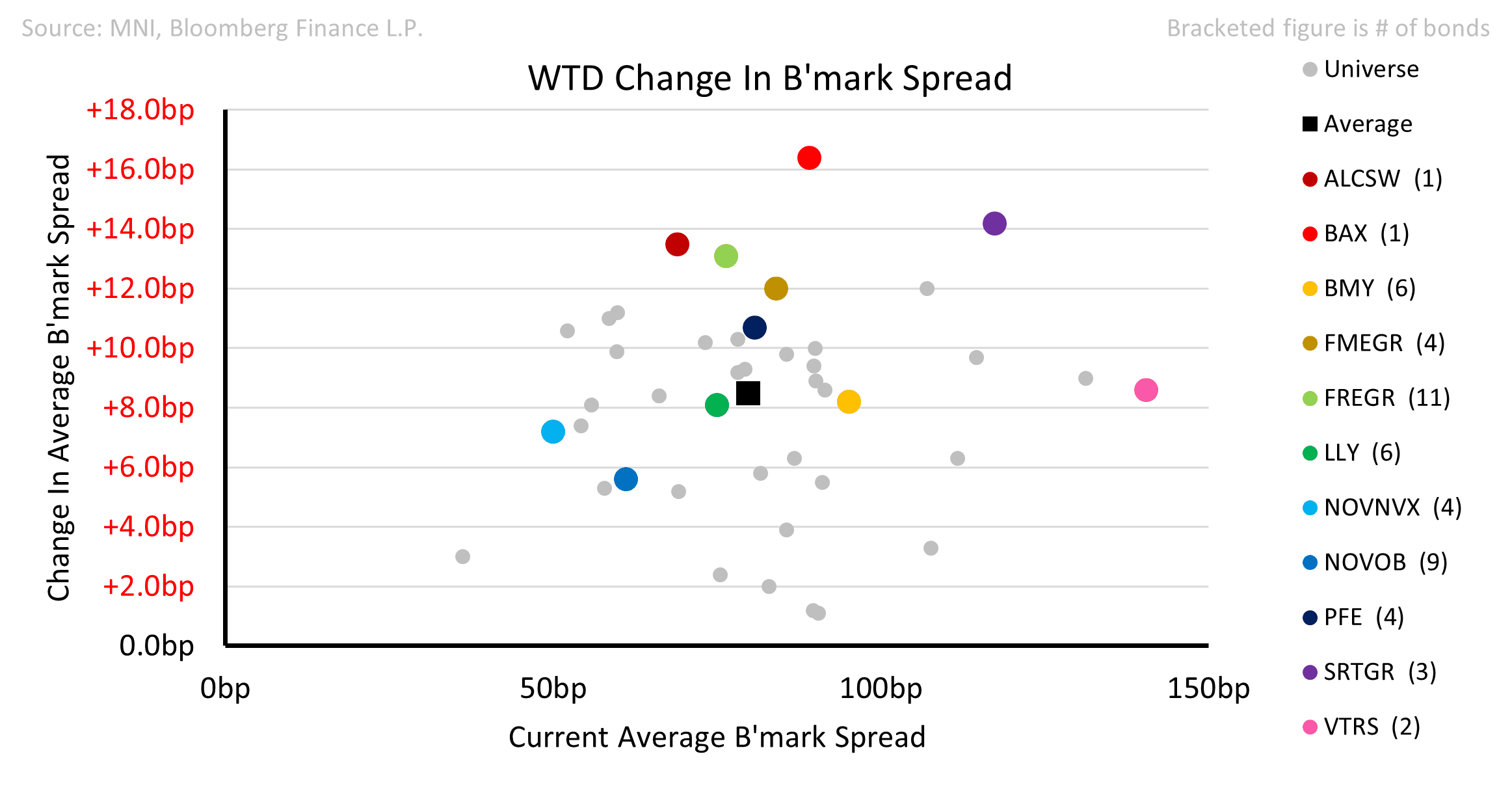

EU HEALTHCARE: Healthcare: Week in Review

Nov-07 11:39

An unusually tough week for Healthcare with spreads on average 8bps wider. Results were generally supportive, but we did see two multi-tranche borrowings across € and $.

- Bristol Myers: €5bn issuance to fund $7bn Tender. BMY 35s +8 wider wtd; +14 ytd.

- Novartis raised $6bn in the USD market to pay for the Avidity takeover.

- Viatris EBITDA was -10% on the ongoing closure of Indore. Fitch may reduce to BBB- depending on how much longer Indore is closed but the company has said that most of the remediation is complete. Only Viatris and BMY are significantly wider on the year.

- Baxter was placed on Review for Downgrade. Its 29s were +16 wider.

- Novo Nordisk and Pfizer are locked in a battle to takeover Metsera. The final bid will likely top $10bn.

- Eli Lilly and Novo Nordisk agreed to sell GLP-1 drugs on TrumpRx. Both will receive tariff reprieve and may see the pill form of GLP-1 expedited.

- Results: Coloplast, Philips, Amgen, Pfizer, Novo Nordisk, Smith & Nephew, Bexton Dickinson, Viatris, AstraZeneca, Fresenius Medical, and Fresenius SE.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

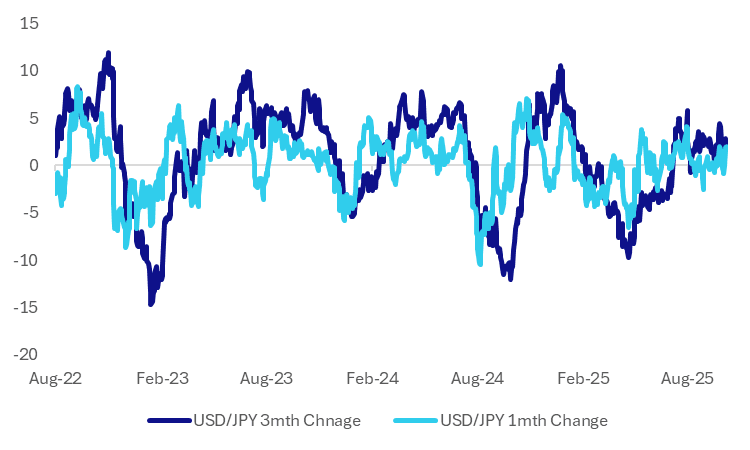

JPY: Official Language, FX Price Action Yet to Mirror Pre-Intervention Patterns

Oct-08 11:28

- The scale and pace of the JPY move this week will be triggering speculation of official intervention in FX markets which, if confirmed, would be the first formal intervention since July last year. Nonetheless, price action and official behaviour so far has not met the pattern of historical formal intervention.

- We are yet to see the usual, more aggressive verbal jawboning that has historically preceded intervention (language including "deeply concerned about FX moves", "will take appropriate response if excessive FX moves"). FinMin Kato's language yesterday appeared more restrained: "refraining from commenting on market moves", "will closely watch any excessive moves".

- We also note USD/JPY's 1 month and 3 month rate of change is comfortably below levels that prevailed during previous intervention episodes. Both metrics are around +2% firmer, which is elevated but well within historical norms.

- That said, a number of xxx/JPY crosses are entering technically overbought territory on the recent rally - triggered by Takaichi's LDP victory and the subsequent backtracking of BoJ rate hike expectations.

- With EURJPY, CHFJPY extending to new alltime highs and short-term momentum measures all accelerating (USDJPY dmas should form a golden cross (50-dma > 200-dma) in the next few days), markets are clearly looking through Takaichi advisor Honda's comments on Monday that USDJPY beyond 150.00 is "a bit too much".

Fig 1: USD/JPY 1mth & 3mth Rate Of Change - Within Historical Norms

Source: Bloomberg Finance L.P./MNI

EURIBOR OPTIONS: Call Spread, Spread

Oct-08 11:18

ERF6 98.1875/98.3125cs vs ERM6 98.37/98.50cs, bought the June for half in 5k.

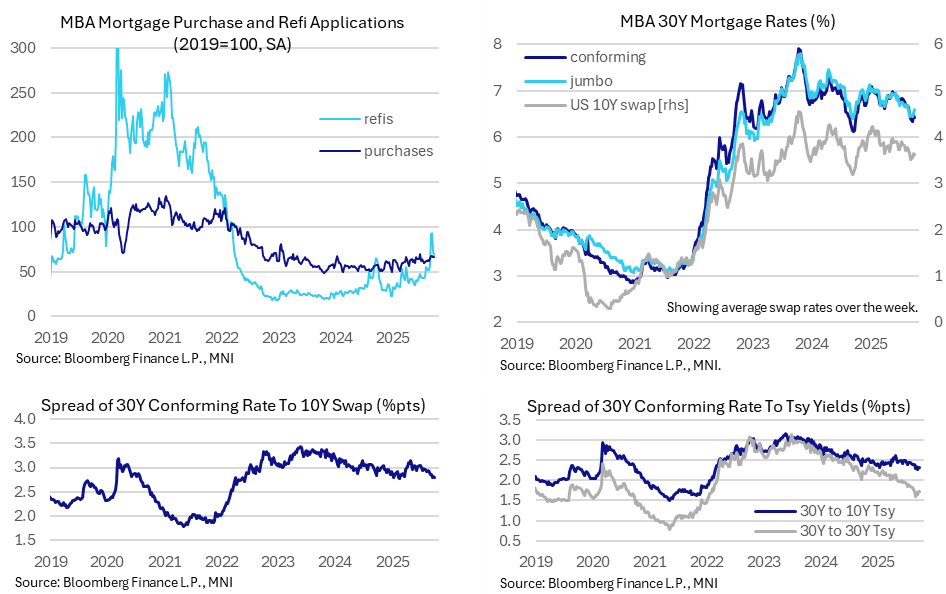

US DATA: Mortgage Applications Continue To Unwind Refi Jump

Oct-08 11:15

- MBA composite mortgage applications fell -4.7% (sa) last week as they continued to chip away at the refi-driven jump in the first half of September.

- Composite applications were -4.7% after -12.7% the week prior, following a 30% increase in the week to Sep 12 and 9% before that in the week to Sep 5.

- Refis were -7.7% after -20.6% and with respective earlier gains of 58% and 12%, whilst new purchase applications were -1.2% after -1.0% and gains of 2.9% and 6.6%.

- Levels relative to 2019 averages: composite at 68% vs a recent three plus year peak of 82% in September, refis at 68% and new purchases at 66%.

- A small decline in 30Y mortgage rates didn’t offer much support on the week, easing to 6.43% (-3bp) after a 12bp increase the previous week. The 6.34% seen in the week to Sep 19 was the lowest since Sep 2024 after a 35bp decline in four weeks starting late August.

- Interestingly, the 30Y mortgage to 10Y Tsy yield spread continues to hover marginally above 230bp having eased modestly since US Tsy Sec Bessent in August talked on wanting to keep the spread between mortgage rates and treasuries flat or even bring it down. These are some of the lowest spreads since Mar 2022.

- The spread to 10Y swap rates meanwhile has averaged 280bp for three weeks now, a tightening from the 300 +/-5bp range seen for some time since reciprocal tariff announcements in April. It’s a little below the 285bp averaged in Q1.

Trending Top

Mar-27 20:13