GOLD: Hawkish Fed Pressures Gold As Correction Continues, Stabilising Today

Hawkish comments from Fed Chair Powell following the expected 25bp rate cut brought gold back below $4000 and it continued to unwind October’s gains. Powell raised doubts over the December meeting commenting that FOMC members feel a pause could be prudent especially given that the lack of data means “you can’t see as far ahead”. This drove the US dollar (BBDXY +0.3%) and yields higher weighing on non-yield bearing gold.

- Bullion has stabilised around $3941.0/oz at the start of Thursday’s APAC trading after falling 0.6% to $3930.07 to be up 1.8% in October. Corrections continue to hold above support at $3900, a Fibonacci retracement. It reached $4030.11 yesterday below resistance at $4161.4.

- Powell said that “a further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it” and that “there's a growing chorus now of feeling like maybe this is where we should at least wait a cycle [meeting], something like that”.

- There are now only ~16bp of cuts priced for December with 22.5bp before the meeting. If this remains the case, then gold may struggle to rally again without drivers of safe-haven flows.

- Silver diverged rising 1.1% to $47.555 to be up 2% this month but still well off the 17 October high at $54.48. The metal reached $48.456, below initial resistance at $49.456, before trending lower. The 50-day EMA is at $45.652. Silver is currently around $47.82

- The S&P e-mini and Euro stoxx were flat but the S&P e-mini has started Thursday down 0.2%. Oil prices were higher with Brent +0.8% to $64.90/bbl. Copper rose 0.6%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

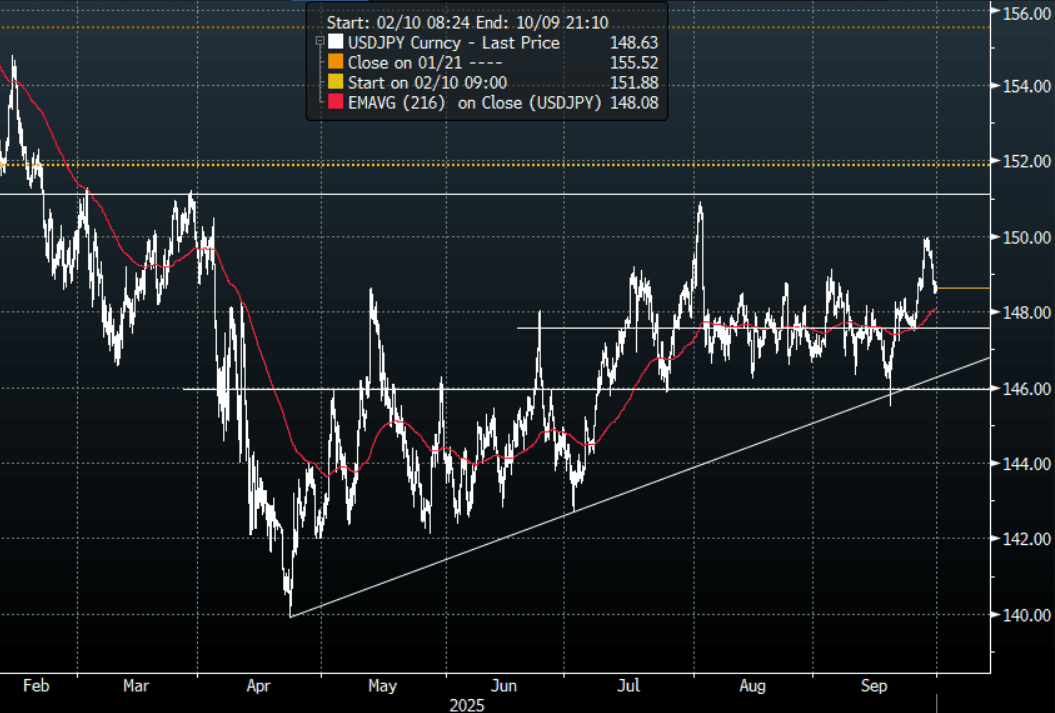

JPY: USD/JPY - Rejects 150.00 As USD Comes Back Under Pressure

The overnight range was 148.58 - 148.85, Asia is currently trading around 148.60. The USD has no friends as the sellers are quick to return on a potential US shutdown. Hawkish comments from the BOJ’s Noguchi gave USD/JPY an extra nudge lower, putting in a sharp rejection of the 150.00 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print could take on larger significance. Some demand returned around 148.50 stalling the momentum lower, next support is back towards the 147.50/148.00 area.

- MNI: Japan Govt Keeps Economic View; Ups Spending, Capex. Japan’s government slightly tweaked its economic assessment in September, upgrading views on private consumption and capital investment for the first time in over a year, though leaving its overall judgment largely unchanged, the Cabinet Office said Monday.

- (Bloomberg) - “Japan Polls Split on Whether Koizumi or Takaichi Leads LDP Race. With less than a week until Japan’s ruling party is set to elect a new leader, opinion polls are split over whether political scion Shinjiro Koizumi or right-leaning Sanae Takaichi has the most backing among the party’s supporters.”

- MNI INTERVIEW: BOJ Decisions Inconsistent - Ex-BOJ's Yamamoto. Markets are watching Bank of Japan communications more closely than economic data for signals on policy moves, with board decisions seen as inconsistent and driven by convenience rather than fundamentals, former BOJ Executive Director Kenzo Yamamoto told MNI.

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.00($876m). Upcoming Close Strikes : 146.00($1.14b Oct 3), 146.50($1.09b Oct 1) - BBG.

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

- Data/Event : Industrial Production, Retail Sales, Housing Starts

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Drops Sharply On Supply Outlook

Oil prices fell sharply with the October 5 OPEC meeting in focus following the resumption of flows from Iraqi Kurdistan to Turkey on the weekend. There was also likely some profit taking after prices rose on concerns regarding the impact on Russian supply from its war with Ukraine. The IEA is forecasting a record market surplus in 2026 and any further rollback of previous OPEC output cuts will add to that. Currently it is expected to increase November production by at least 137kbd in line with October.

- WTI fell almost 4% to $63.18/bbl to be down slightly in September. It reached a high of $65.40 early in European trading and then fell to a low of $62.98, holding above the bear trigger at $60.85. It is currently around $63.10.

- Brent was down 3.5% to $67.95/bbl and is now little changed on the month. It rose to $69.91 before declining to $67.52, above key support at $64.50, 30 June low.

- It is difficult to know at this stage if further increases in OPEC’s production target will materialize with most members, except Saudi Arabia, having little spare capacity.

- US special envoy Witkoff said that Israel has agreed to the US Gaza peace proposal but Hamas is yet to respond.

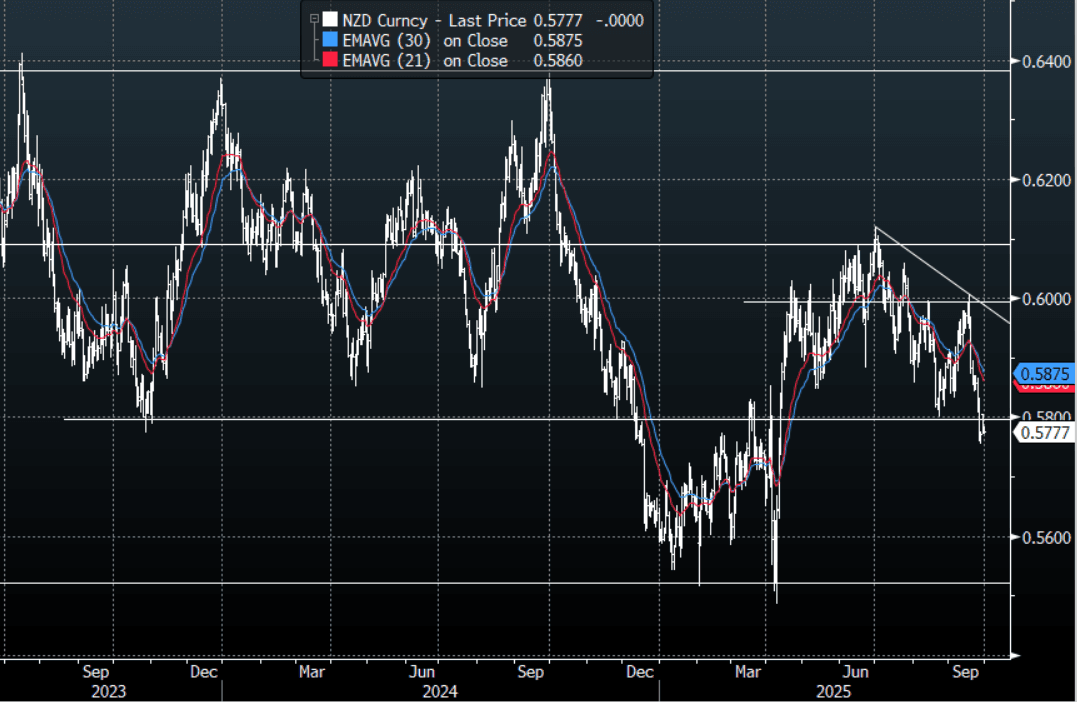

NZD: NZD/USD - Trades Heavy Below 0.5800

The NZD/USD had a range overnight of 0.5776 - 0.5796, Asia is trading around 0.5775. US stocks moved back close to the highs before the market thought a shutdown might not be that great for risk, the USD can’t find any friends and a potential shutdown brought out all the bears again. The NZD broke through its pivotal 0.5800 support last week and has kept the pair under pressure trading heavy even with the USD falling. The first sell zone would be between the 0.5850/0.5900 area. US Futures have opened slightly lower this morning, E-minis -0.10%, NQU5 -0.10%.

- Bloomberg - “RBNZ Proposes Expanding Use of Word ‘Bank’ to More Lenders. RBNZ issues a consultation paper that proposes expanding the use of the word ‘bank’ to all deposit takers that become licensed under the Deposit Takers Act, central bank says in statement.”

- MNI AU - The ANZ business survey for September is released on Tuesday. The activity assessment compared to a year ago is an important signal for GDP in the quarter. Business confidence and the activity outlook are off the May lows, following the announcement of US tariffs, but remain below the Q4 2024 peak. The price/cost components are also important to monitor.

- MNI Brief - China will provide an additional CNY500 billion to support investment as the economy faces challenges, National Development and Reform Commission spokesperson Li Chao told a briefing on Monday.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5785(NZD1b), 0.5860(NZD332m), 0.5875(NZD372m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

- Data/Event: ANZ Business Confidence

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P