US 10YR FUTURE TECHS: (H6) Bull Cycle Intact For Now

- RES 4: 113-22+ High Nov 25 and a key resistance

- RES 3: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 2: 113-07 High Dec 3

- RES 1: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- PRICE: 112-21 @ 16:10 GMT Dec 19

- SUP 1: 112-06/111-29 Low Dec 16 / 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

The spike higher in Treasuries Thursday highlights a stronger short-term bullish condition and for now signals scope for a continued retracement of the recent Nov 25 - Dec 10 bear leg. A resumption of gains would open 113-00+, a Fibonacci retracement. Price has pulled back from yesterday’s high, a deeper pullback would cancel a bull theme and instead refocus on attention on 111-29, the Dec 10 low and a key short-term support.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SEK: EURSEK Pierces Nov 11 High, But Remains Stuck In Familiar 10.90-11.10 Range

EURSEK has pierced the Nov 11 high of 11.0096, now +0.4% today, with Scandi FX pressured by the latest extension higher for the DXY. This week’s domestic calendar has been light (and is expected to remain as such), leaving SEK susceptible to swings in broader risk sentiment. The fallout from Nvidia’s earnings this evening and tomorrow’s US labour market report will likely prove consequential in the short-term.

- Zooming out, the cross remains comfortably within the 10.90 to 11.10 range that has contained price action since the start of September.

- Progress on Sweden’s expected economic recovery will be key in determining the medium-term trajectory. Recent developments have been positive, though the final Q3 GDP report on Nov 28 will be important to confirm the solid signals from the (often unreliable) flash release.

- Note that the December 2026 RIBA future has risen from just below 1.70% in mid-October to ~1.85% at present, consistent with our view that the risk of a hike is greater than the risk of another cut over a 6-12 month horizon. That hasn’t had much impact on the exchange rate though, as the bar to a Riksbank policy rate move appears very high in the near-term.

- Last week, JP Morgan recommended reinitiating a short EUR/SEK trade (entry 10.9678). They wrote that “With Eurozone data surprises at new YTD highs, and DM PMI data due next week, we think the market is under appreciating the Eurozone cyclical upswing, particularly as European bank stocks broke out to new highs this week. SEK is a high beta cyclical proxy for these macro signals. US equity weakness is a risk for SEK, but we think this can also be its strength if there is a rotation into Europe”.

SECURITY: Thune Indicates Senate Still "Ready To Go" On Russia Sanctions

Senate Majority Leader John Thune (R-SD) told reporters he still wants to pass the Russia sanctions bill, but it needs to start in the House: "We want to get it done. Now I think it's probably, it's a revenue measure most likely originates in the House... As you know, we've been ready to go on that for a long time..." per Frank Thorp at NBC News.

- Andrew Desiderio at Punchbowl notes, "First time I’ve heard Thune say this about the Russia sanctions bill. [House Speaker Mike] Johnson [R-LA] hasn’t made a commitment on it either way, but Thune (and pretty much every Senate Republican) really wants to get it done."

- Thune's comments come amid reports that the Trump administration is 'secretly' negotiating a new 28-point Ukraine peace plan with Russia. The peace initiative has overshadowed the renewed push for sanctions, which Senator Lindsey Graham (R-SC) claimed ealier this week now had the greenlight from President Donald Trump.

- A short time ago, CNN confirmed that a high-ranking US military delegation arrived in Kyiv for talks with Ukrainian President Volodymyr Zelenskyy. According to CNN, a US army spokesperson said the delegation is “on a fact-finding mission to meet with Ukrainian officials and discuss efforts to end the war,” but there is an understanding that the group will present the peace plan to Zelenskyy.

- In a potential signal that Europe could be on board with the peace initiative, Hans von der Burchard at Politico reports that German Chancellor Friedrich Merz said his government is in touch “on a daily basis” with the Trump administration on the new peace initiative for Ukraine, but “at the moment, it is not clear whether this will lead to a result in the short term.”

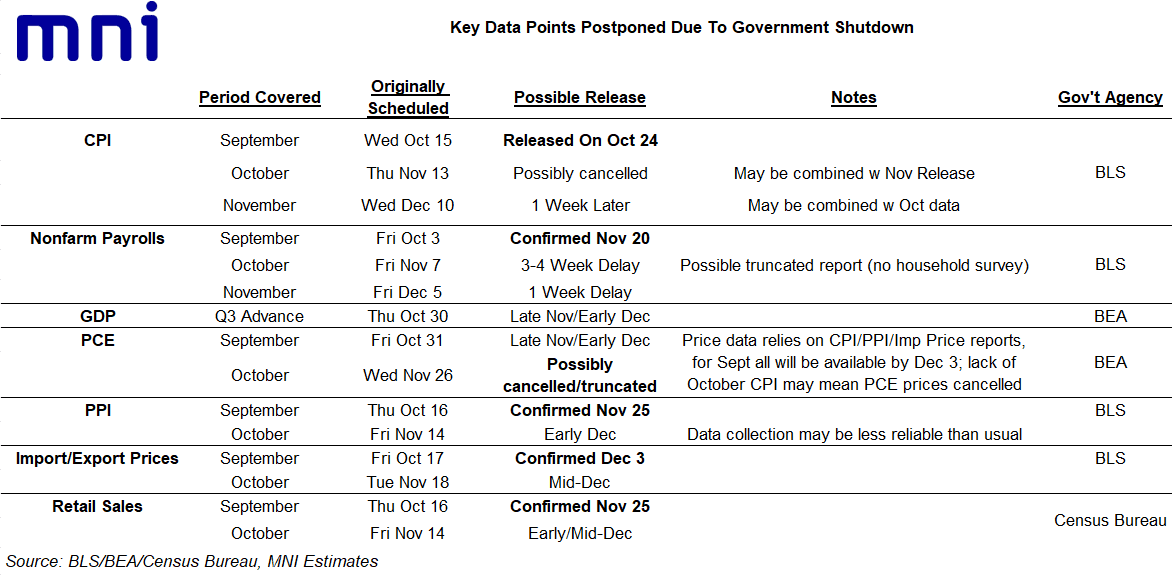

US DATA: Fed Still Unlikely To Have November CPI, Payrolls By Dec Decision Time

In our latest MNI FedSpeak podcast we discussed the outlook for economic data releases as the Federal Reserve's December decision looms - we also opined on what the meeting decision and messaging might be. To hear the full episode (recorded Tuesday), click here.

- Despite the latest scheduling updates indicating an increasing likelihood of getting Q3 GDP and September PCE in the coming couple of weeks, MNI remains doubtful that the Fed will have nonfarm payrolls data for November (originally scheduled for Dec 5) by its December 9-10 meeting - particularly since the BLS backlog appears to be clearing only slowly, and the Thanksgiving holiday (Nov 27) approaches. We acknowledge that opinions are mixed on the November payrolls release, with some analysts still having a Dec 5 release as their base case.

- When and if it does come out, October's dataset would include only the Establishment survey but not Household survey results (so headline payrolls but not unemployment rate etc), so there is a chance a short report will be produced by early Dec.

- Overall we think there's a good case to combine the October and November reports due to the data collection deficiencies in October. Merely getting a headline payrolls number from October may not be enough to sway Fed decision-making - in the event of a weak figure, hawks may shrug off the noisiness and uncertainty surrounding the collection of data in the month, while most are looking more closely at the unemployment rate anyway as a gauge of labor market looseness.

- And while there has been no official word from BLS, October CPI's reading will almost certainly be cancelled, which should preclude the publication of an October PCE prices report altogether. The November CPI data was scheduled to be released on the morning of the FOMC decision but that looks extremely unlikely.

- We update our key data points schedule below. Our FAQ on rescheduled data (Nov 11) remains largely intact, though releases are coming out a little more slowly than we had anticipated, by a few days to about a week - here

- Also see MNI's Data Methodology Cheat Sheet (Nov 13 - including methodologies underlying data releases) - here