SWEDEN: Govt Confirms SEK17.3bln Extra Amending Budget To Respond To Iran War

May-27 09:23

"*SWEDEN GOVT CONFIRMS SEK17.3B SPENDING TO EASE IRAN WAR EFFECT" Bloomberg "*SWEDISH GOVT PRESENTS ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

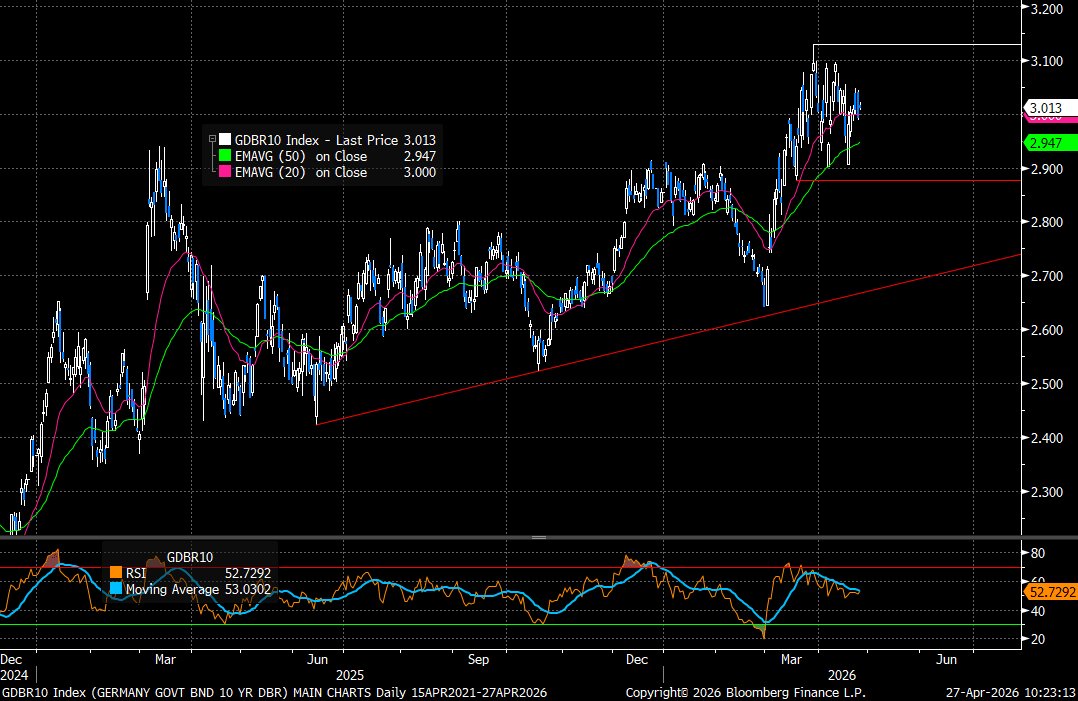

EGBS: 10-year Bund Yields Need Material Iran News To Break Out Of 20bp Range

Apr-27 09:23

10-year Bund yields continue to pivot around the 3.00% level, in a rough 2.90-3.10% range for six weeks now. A clear break in either direction will require some material developments in the Iran war, with markets currently having to battle heavy, mixed headline flow on ceasefire prospects.

- The curve has lightly bear steepened this morning, with Schatz yields little changed at 2.55% and 30-year yields up 2bps to 3.54%.

- A medium-term downtrend in Bund futures remains intact. A triangle has developed on the daily chart - this is a continuation pattern and reinforces the bearish theme. Futures are -3 ticks today at 125.60, with initial support the 125.00 figure.

- The lack of increase in wage and long-term inflation expectations in the Q1 SAFE survey will be reassuring to ECB Governing Council members. All else equal, it supports arguments suggesting the risks of second round effects are lower than in 2022, reducing the need for an aggressive, front-loaded, hiking cycle

- The EU will sell bonds at 1030BST today. Demand metrics will be in focus after the EU finally approved its E90bln loan to Ukraine in recent weeks.

- Belgium will also look to hold a conventional auction today for a combined E2.6-3.0bln. Belgium was downgraded by S&P on Friday, but this should already be in the price for OLOs.

- Finally, the EFSF has sent an RfP with regards to an upcoming transaction, suggesting a syndication is likely today or tomorrow.

- A reminder that this week’s Eurozone calendar is very heavy, with surveys, flash inflation data, flash GDP data and the ECB decision all due.

Figure 1: 10-year Bund Yields Since 2025 (Source: Bloomberg Finance L.P)

EURIBOR OPTIONS: Mid Curve Call Condor Spread

Apr-27 09:19

0RM6 97.00/97.25/97.75/98.00c condor vs 2RM6 96.87/97.12/97.62/97.87 iron c condor, bought the 1yr for 2.5 in 7.5k.

FOREX: USD Index Reverses Opening Gap Higher in Short Order

Apr-27 09:07

- Oil prices rose and the USD rallied at the resumption of trade on the back of cancelled US-Iran talks over the weekend and only saw temporary downward pressure from a report that Iran had presented another proposal to the US to open the Strait of Hormuz. Despite that, risk optimism prevailed, leading the USD Index to more than retrace its opening gap higher, to a 0.2% session loss but with a material range Monday morning of more than 1%.

- Dollar weakness throughout the European morning holds, with AUD and NOK standing out to the upside. AUDUSD is starting to make another attempt at the 0.7200 handle, with the bull trigger at 0.7222, the April high, clearance of which would mean the highest levels since June 2022.

- NOK strength comes as terms of trade tailwinds continue helping the krone outperform the G10 basket. We've previously noted that the current backdrop appears favourable for NOK, drawing on the strong recovery in risk assets, still-elevated oil prices and hawkish domestic impulses for Norges Bank to consider. USDNOK (-0.8% at 9.2500) is through last Wednesday's low, narrowing the gap to next support around 9.2000 / 9.2076 (May 2022 low).

- Ahead of the Tuesday's BoJ meeting, USDJPY extends session lows below 159.20 in European trade. The pair remains in consolidation mode, with the primary trend still bullish but price action failing to meaningfully push above the 160.00 mark over the course of the Iran war. Support around the 50-day EMA remains intact - currently at 158.35. A clear break of the average is required to signal a short-term reversal. Attention is on key resistance and the bull trigger at 160.46, the Mar 30 high.

- Most analysts see the BoJ retaining a “hawkish hold” stance, with tightening still part of the forward path. Governor Ueda is expected to emphasise data dependence and “difficult policy trade-offs,” while still signalling that “more tightening will be needed over time” alongside possible downgrades to growth forecasts and upgrades to inflation.

- Dallas Fed Manufacturing Activity is on today's light data calendar while the Fed and ECB remain in their respective quiet periods ahead of their decisions this week.

Trending Top

May-29 06:00