RENEWABLES: German Wind Output Forecast Comparison

Jun-04 13:24

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg's EC...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

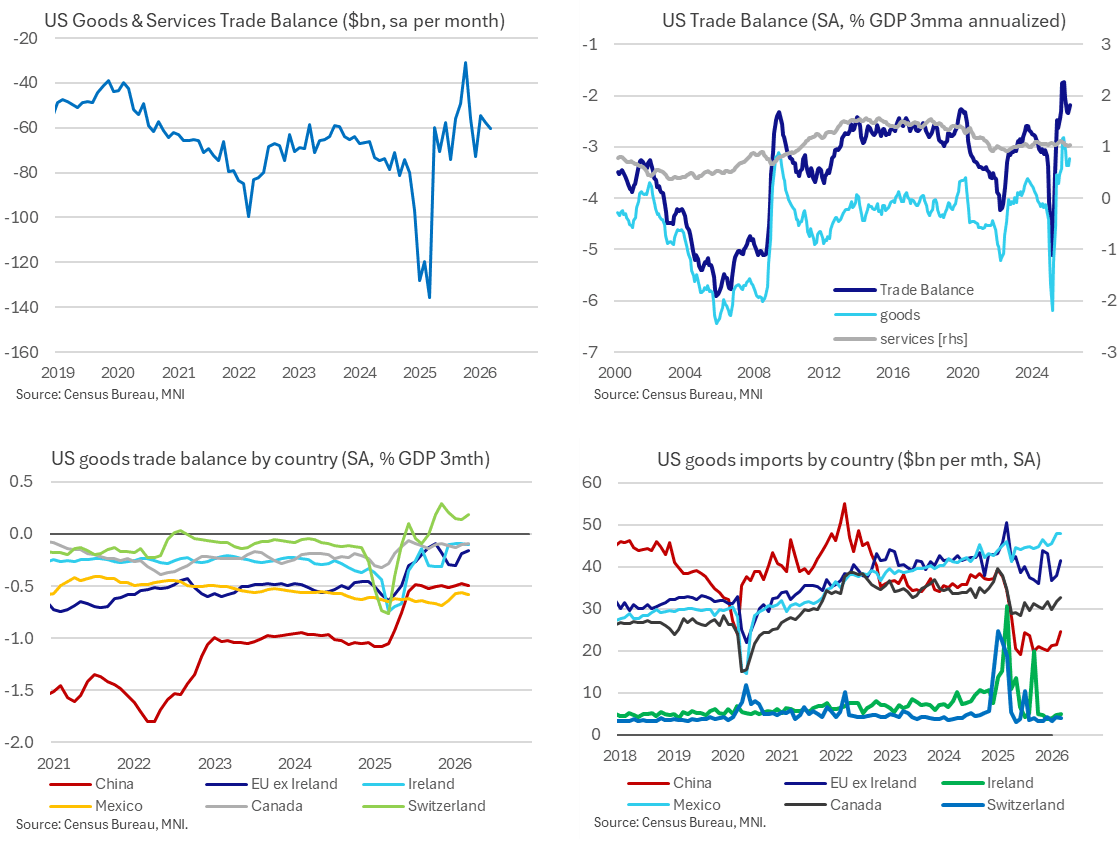

US DATA: Confirmation Of Smallest Trade Deficit Since The 1990s

May-05 13:23

The goods & services trade deficit was worth ~2.2% GDP in Q1. It's a little off last year’s brief three-month lows of 1.7% GDP but on a slower moving basis is the smallest deficit since the 1990s after the tariff-driven goods adjustment.

- The goods & services trade deficit was slightly lower than expected in March at $60.3bn (cons $61bn) after $57.8bn (revised from $57.3bn) in February.

- We’re back to separate releases with a goods-only advance (unusually close to consensus last week) before today’s full goods & services version, having shifted to only a final release when catching up after the government shutdown.

- It leaves what have been three relatively steady months in Q1 after last year’s huge swings on US trade policies.

- Latest 3-mth rolling balances: goods & services deficit of 2.2% GDP, goods deficit at 3.2% GDP and services surplus at 1.0% GDP.

- For a smoother trend, the 12-month goods deficit of 3.3% GDP confirms what was the smallest deficit since the late 1990s per the advance release whilst the services surplus remains at a fairly typical 1.1% GDP compared to post-pandemic years.

- Today’s new country-level data keep to recent trends: China and the EU have seen the largest adjustment in trade balances with the US under the second Trump administration although that mostly came in early- to mid-2025. Both have seen balances narrow by 0.5pp of US GDP, with the deficit with China trimmed from 1.0% GDP end-2024 to 0.5% GDP on a three-month rolling basis and the deficit with the EU from 0.8% to 0.3% GDP.

- Switzerland is another country with a large adjustment (from -0.3% to 0.2% GDP) although that’s amplified by base effects from gold shipments in late 2024 between the presidential election in Oct and Trump then taking office in Jan 2025.

- In signs of USMCA still having an impact despite various challenges, Canada and Mexico have seen relatively very little adjustment in trade, at least at a balance level. The deficit with Canada has been trimmed from 0.2% GDP to 0.1% GDP whilst the deficit with Mexico is unchanged at 0.6% GDP.

NORGES BANK: MNI Norges Bank Preview: May 2026 - Patience May Not Prevail

May-05 13:21

FOR THE FULL PUBLICATION PLEASE CLICK HERE

EXECUTIVE SUMMARY:

- Norges Bank laid the foundations for rate hikes at the March decision, and we expect the first to be delivered in May, bringing the deposit rate to 4.25%. Such a move would go against analyst consensus for a hold at 4.00%, though rates markets lean slightly in favour of a hike.

- Norges Bank are primarily concerned about high domestic inflation, with the Iran war providing a separate hawkish impulse to the outlook given Norway’s status as an energy exporter. As such, we don’t see much value in the Board waiting till June to hike rates – elevated inflation has been flagged as a concern for some time now, and the March guidance was quite clear that the Committee is ready and willing to act

- Of the 14 analyst previews we have seen, 6 expect a rate hike in May and 8 expect a hold. Notably, of the 6 Scandinavian bank previews we have seen, 4 expect a hike and 2 expect a hold.

GBP: FX Exchange traded Option

May-05 13:18

GBPUSD (5th June) 134.00p, bought for 0.56 in 1k.

Related bullets

Related by topic

Renewables

Energy Data

Germany

Emissions

G3

North America

TTF ICE

Asia LNG

Asia

Gas Positioning