EM LATAM CREDIT: Geopark: Frontera Acquisition – Negative

(GEOPAR; NR/B+/B+) * Colombia oil and gas E&P Geopar is buying Frontera's upstream Colombia busines...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Effective Fed Funds Rate

FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $169B

Repo Reference Rates from earlier:

- Secured Overnight Financing Rate (SOFR): 3.71% (-0.06), volume: $3.321T

- Broad General Collateral Rate (BGCR): 3.69% (-0.06), volume: $1.296T

- Tri-Party General Collateral Rate (TCR): 3.69% (-0.06), volume: $1.268T

- (rate, volume levels reflect prior session)

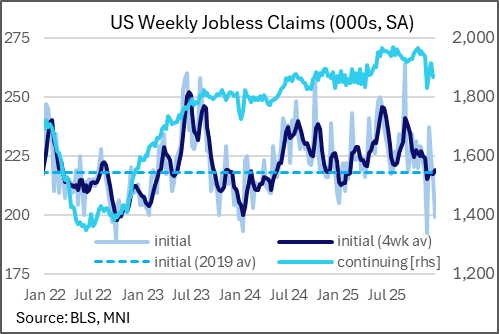

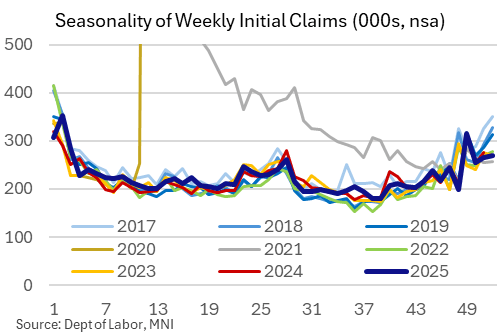

US DATA: Low Jobless Claims In Volatile Holiday Period, Weather May Be A Factor

Initial jobless claims for the Dec 27 week were much lower than expected at 199k, vs the 218k consensus (215k prior rev from 214k). This marked the lowest level of seasonally-adjusted initial claims since the Nov 29 week, though it is for that reason that we suggest caution: both are holiday weeks (the other is Thanksgiving) which typically translates into volatility in claims.

- Indeed NSA claims rose 5k to 270k so the seasonal adjustment factor is doing a lot of the heavy lifting here, as in previous years the NSA increases have lacked a discernable pattern for this week (2022 +9k, 2023 -5k, 2024 +8k)

- Claims looked low vs previous years across several major states; at a guess we would say this may be due to unusually warm weather this year across much of the country, in addition of course to the usual seasonal volatility.

- And while this was a large dropoff on an SA basis, the rise in the first week of December means the 4-week moving average in SA claims rose 2k to 219k for the highest since mid-November, so the general "low-fire" trend remains intact.

- Meanwhile continuing claims for the Dec 20 week came in at 1,866k (1,902k consensus, 1,913k prior rev from 1,923k), marking a 3-week low but still in the recent ranges. NSA claims dropped 103k to 1,881k, and like initial, we would expect a large pickup the following week.

- Note that neither claims data point represented the Employment Report's reference week.

US TSYS: Early SOFR/Treasury Option Roundup

SOFR & Treasury options revolved around downside puts overnight through this morning's lower than expected weekly claims data. Underlying futures weaker post data while projected rate cut pricing retreats vs. late Tuesday levels (*): Jan'26 at -3.5bp, Mar'26 at -12.5bp (-14bp), Apr'26 at -18.5bp (-20.9bp), Jun'26 at -32.7bp (-35.1bp).

- SOFR Options:

- +4,000 SFRG6 96.37/96.43/96.50 put flys, 1.0 vs. 96.47/0.10%

- +2,000 SFRZ6 99.00 calls, 2.0

- +2,000 SFRG6 96.56/96.75 1x2 call spds .75

- +5,000 SFRU6 96.12/96.31 put spds, 1.0 ref 96.84

- 3,500 2QH6 96.37 puts ref 96.685

- 3,000 SFRZ6 96.37/96.81 put spds ref 96.895

- 2,400 SFRH6 96.31/96.50 put spds ref 96.49

- 1,500 SFRZ6 96.18/96.31 2x3 put spds

- 2,000 SFRF6 96.37/96.43 2x1 put spds ref 96.50

- 5,000 SFRF6 96.37 puts ref 96.50

- Block, 5,676 SFRF6 96.62/96.68/96.75/96.87 call condors, 0.5 net ref 96.495

- Treasury Options:

- 1,100 USH6 113/114 put spds ref 115-22

- 1,000 USH6 108/112 put spds ref 115-27

- 4,000 TUG6 104.12/104.37 put spds ref 104-14.12

- 1,000 USG6/USH6 116 put spds, 34 net / Mar over

- +1,600 FVG6 109.5 calls, 20 vs. 109-16.25/0.49%

- +1,200 TYH6 114.5 calls, 14

- +3,000 TYG6 110 puts, 1

- +6,500 TYG6 112/113.5 call over risk reversals, 0.0 vs. 112-23/0.51%