UK: GBP Remains Buoyant as Labour Manifesto Details Emerging

Jun-13 10:47

- Most recent CFTC data indicated that GBP net length is the largest across G10 at 16.1% of open interest, supported throughout the year by expectations for a first cut from the BOE continuing to be pushed back this year, now seen in November. Labour market and GDP data has done little to move the dial this week ahead of the June 20 BOE decision.

- Despite potential risks surrounding the July 04 election and the impacts on the UK economy from a Labour majority, the currency continues to trade in a buoyant manner, only outperformed by the Norwegian Krone against the greenback in the last six months.

- Having closed below the 0.8500 mark for the first time since August 2022 last Friday, EURGBP has spent the week consolidating below support at 0.8484, the May 29 low and bear trigger. Initial downside pressure saw the cross narrow the gap with initial support at 0.8408, however, price has since settled around 0.8450. A bearish dynamic remains firmly in play and a more significant target is found at 0.8340. Resistance moves down to 0.8499, the 20-day EMA.

- Bullish conditions remain firmly in place for GBPJPY. After closing back above the psychological 200 mark earlier this week, the pair has been consistently edging higher and eating into the steep declines seen back in 2008.

- It is also worth highlighting that alongside the BOE decision on June 20, the Swiss National Bank will also decide on rates, having become the first major central bank to cut rates earlier this year. Recent hawkish remarks from SNB’s Jordan have tempered expectations for another cut from the SNB and GBPCHF has dipped in sympathy.

- Medium-term trend conditions in GBPCHF remain bullish - moving average studies are in a bull-mode set-up highlighting a dominant uptrend and the recent pullback appears to be a correction. However, the latest consolidation appears to be a bear flag - a continuation pattern - and if correct, suggests scope for a deeper short-term retracement.

- A break below 1.1362, the Jun 5 low would open 1.1320, the May 9 low. Clearance of this level would strengthen a bearish theme and expose 1.1171, the Apr 19 low and a key support. Key resistance has been defined at 1.1678, the May 27 high. A break of this level would resume the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Italy 2037 BTP Green: Final Terms

May-14 10:46

- EU9b Green Fixed (Oct. 30, 2037) at BTPS+9

- Guidance BTPS+11 area

- Books above EU84b (including JLM interest): Leads

- Coupon: Semi-annual, act/act

- Benchmark Security: BTPS 0.95% 3/2037

- Issuer: Italy Buoni Poliennali Del Tesoro (BTPS)

- Ratings: Baa3/BBB/BBB

- Format: Reg S, dematerialized, registered, senior unsecured, 144a eligible, CAC,, green bond

- UOP: In accordance with Italy’s Framework for the Issuance of Sovereign Green Bonds

- Settlement: May 21, 2024

- Denoms: 1k x 1k

- ISIN: IT0005596470

- Bookrunners: BNPP, CA-CIB, DB (B&D), NatWest Markets, UniCredit

- Full first coupon on 30 October 2024 accruing from 30 April 2024

- Target Market: Eligible counterparties, professional clients and retail clients (all distribution channels)

Details as per Bloomberg

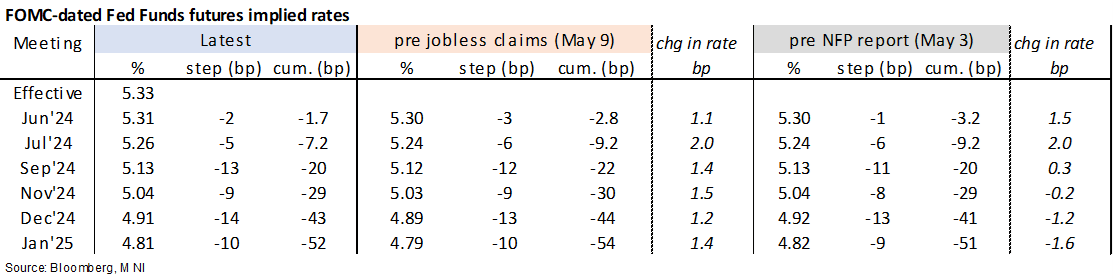

STIR: Fed Rate Path Softens Slightly With PPI and Powell Ahead

May-14 10:39

- Fed Funds implied rates have tilted slightly lower, initially aided by some dovish BoE commentary but with front end Treasuries since outperforming.

- It leaves a rate path broadly similar to levels seen prior to the payrolls report, slightly higher for near-term meetings and lower for end-2024.

- Cumulative cuts from 5.33% effective: 1.5bp Jun, 7bp Jul, 20bp Seo, 29bp Nov and 43bp Dec.

- Today’s focus is first on PPI inflation at 0830ET before Fed Chair Powell in a special event with ECB’s Knot at 1000ET (no text).

- It’ll be Powell’s first appearance since the May 1 FOMC press conference (highlights of which can be found in the MNI Fed Review here). Since then, the payrolls report surprised dovishly across the board but some inflation metrics have surprised higher including ISM services prices paid and surveyed inflation expectations.

- There will no doubt be questions on whether Powell has seen tomorrow’s CPI data. Guidance that he gave when speaking to Rubenstein in Feb 2023 suggests his appearance will come a little early as he said he receives some key data the “night” before.

SONIA: Call fly buyer

May-14 10:38

SFIU4 95.10/95.25/95.40c fly, bought for 2 in 5k.