JGBS: Futures Weaker Overnight, Mixed US-Iran Signals

May-27 23:27

In post-Tokyo trade, JGB futures closed weaker, -7compared to settlement levels, after US tsys finis...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Slightly Weaker Overnight Ahead Of BOJ Decision

Apr-27 23:25

In post-Tokyo trade, JGB futures closed weaker, -6 compared to settlement levels, after cash US tsys US tsys finished 2-3bps cheaper across benchmarks amid Middle East headlines.

- Headlines have crossed from a FoxNews interview with US Secretary Of State Rubio. Rubio states that the Iran offer the US received was better than expected. This follows earlier headlines from the WSJ that the US was considering making a counter offer in coming days, as Trump reportedly remain skeptical the ability of Iran to meet the key objective around its nuclear program.

- Global central banks are the focus this week with the BOJ today, FOMC on Wednesday, and the BOE and ECB on Thursday.

- Most banks see the BOJ pausing at the 27-28 April meeting while retaining a "hawkish hold" stance, with tightening still part of the forward path.

- Governor Ueda is expected to emphasise data dependence and "difficult policy trade-offs," while still signalling that "more tightening will be needed over time," alongside possible downgrades to growth forecasts and upgrades to inflation.

- Market pricing and bank forecasts cluster around a June move (with July a fallback). (See MNI BOJ Preview here)

Source: Bloomberg Finance LP / MNI

AUSSIE BONDS: Modestly Cheaper, Light Local Calendar Ahead Of CPI Tomorrow

Apr-27 23:19

ACGBs (YM -1.5 & XM -3.0) are weaker after cash US tsys US tsys finished 2-3bps cheaper across benchmarks amid Middle East headlines.

- Cash ACGBs have bear-steepened, with yields 1-4bps higher and the AU-US 10-year yield differential at +68bps. Cash bonds were closed yesterday.

- The bills strip pricing is -1 to -2 across contracts.

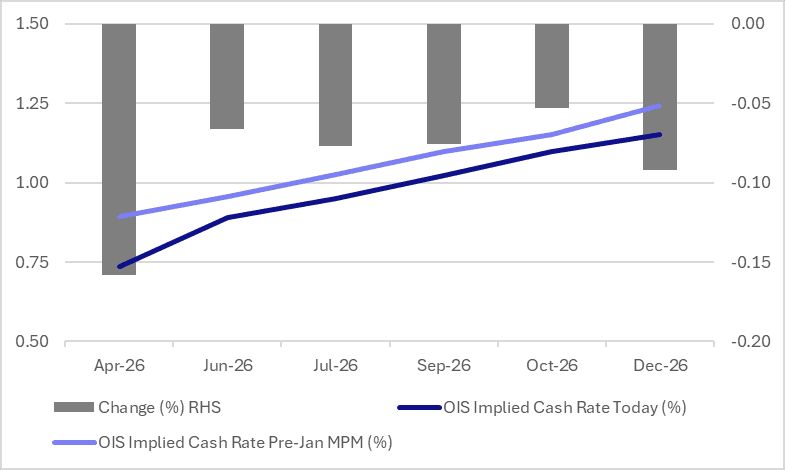

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 81% for May to 179% by August and 256% by December 2026.

- Today, the local calendar will be empty.

- Q1 and March CPI data will be released tomorrow and will be monitored very closely to set final expectations for the 5 May RBA decision. It will also be scrutinised for any early impact from the Middle East conflict beyond fuel prices in the monthly March data. There is a high correlation with NZ and its Q1 inflation data signal that inflation in Australia may have also stabilised. The 40% and 70% rises in petrol and diesel prices could add at least around 1pp to March headline inflation.

- The AOFM plans to sell A$1000mn of the 4.25% 21 December 2035 bond today and A$1000mn of the 4.50% 21 April 2033 bond on Friday.

BONDS: NZGBS: Modestly Cheaper After Long Weekend

Apr-27 23:02

NZGBs are 2bps cheaper, following the long weekend, after US tsys finished 2-3bps cheaper across benchmarks amid Middle East headlines.

- Headlines have crossed from a FoxNews interview with US Secretary Of State Rubio. Rubio states that the Iran offer the US received was better than expected. This follows earlier headlines from the WSJ that the US was considering making a counter offer in coming days, as Trump reportedly remain skeptical the ability of Iran to meet the key objective around its nuclear program.

- Global events picks up tomorrow with ADP weekly employment and Conference Board Consumer Confidence. Otherwise, focus is on Central Banks this week with the BOJ today, FOMC on Wednesday, and the BOE and ECB on Thursday.

- NZ’s filled jobs rose 0.3% m/m in March versus revised +0.2% in February.

- Bloomberg - "India and New Zealand signed a free-trade deal cutting tariffs on most goods and expanding market access."

- "Fertilizer woes. Up to 60% of Mideast urea output may have been lost since the start of the conflict, CRU Group said, threatening global food inflation. " – BBG

- Swap rates are unchanged.

- RBNZ-dated OIS pricing is little changed across meetings. 14bps of tightening is priced for May, while February 2027 assigns 109bps.