JGBS: Futures Higher Overnight Amidst Conflicting News On US/Iran Talks

In post-Tokyo trade, JGB futures closed stronger, +10 compared to settlement levels, after US tsys m...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

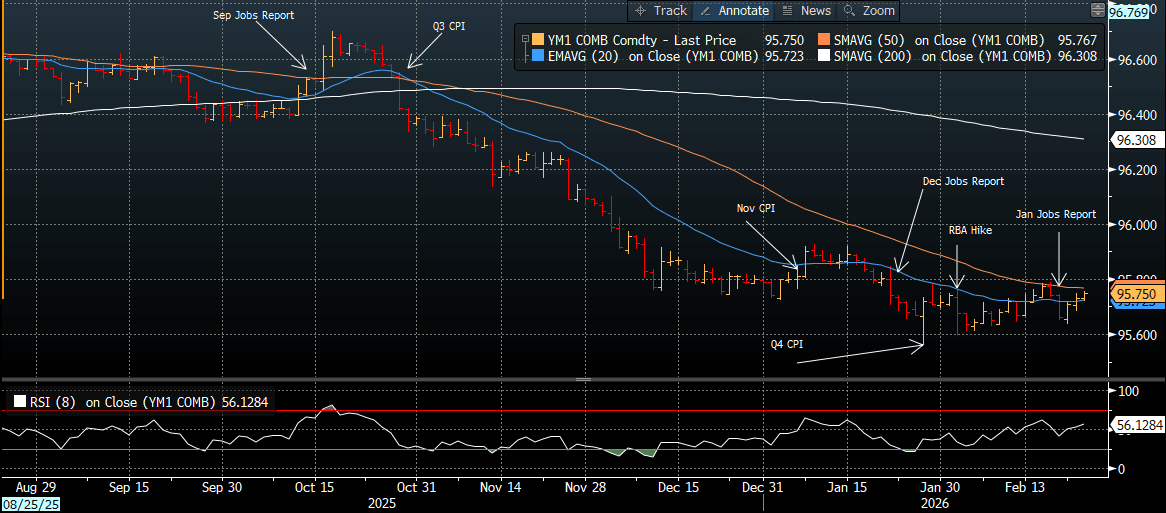

AUSSIE BONDS: Richer With US Tsys As Risk-Off Buoys, CPI Tomorrow

ACGBs (YM 2.5 & XM +3.0) are stronger after US tsys finished 2-6bps richer, with the 5-10-year zone leading, buoyed by risk-off sentiment.

- The head of the RBA's Economic Analysis area, Michael Plumb, has given a speech this morning. It looks to be very in line with post RBA guidance after the recent rate rise earlier in Feb. "In short, we assess that much of the pick-up in inflation was due to some sector-specific price pressures that we expect to dissipate in coming quarters. But overall growth in demand also looks to have been stronger than expected in the second half of last year, adding to existing economy-wide capacity pressures and therefore inflation."

- Cash ACGBs are 2-3bps richer with the AU-US 10-year yield differential at +66bps.

- The bills strip is slightly mixed across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 17% for March to 96% by June and 144% by December 2026.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond today and A$800mn of the 2.75% 21 November 2028 bond on Friday.

Bloomberg Finance LP

CNH: Onshore Markets Return, USD/CNH Holding Under 6.8900, LPRs Seen Steady

China onshore markets return from the LNY break today. Spot USD/CNH is holding under 6.8900 at this stage, but above recent lows of 6.8810. All key EMAs remain in downtrends, with the 20-day around 6.9160 in terms of potential upside resistance. Downside focus is likely to rest at 6.8500, levels last seen in the first half of 2023. Spot USD/CNY ended at 6.9048 before the LNY break, and early focus will be on if the pair can test under 6.9000 and sustain the move. The last USD/CNY fixing level was at 6.9398 (back on Feb 13).

- Since China markets went on holiday the USD BBDXY index is higher (from around 1813.35 to above 1189 in late NY Monday dealings). Still, the recent tariff news from late last week/over the weekend has driven fresh uncertainty around the USD outlook and whether it drives a fresh wave of negative dollar sentiment (like we saw through parts of the first half of 2025).

- The yuan should be a natural beneficiary to any such trends and yesterday Hong Kong related equities rose strongly (HSI up +2.53%). Still, in Monday US trade the Golden Dragon equity index fell by 0.95%.

- The yuan may also receive some benefit from lower tariff rates post the SCOTUS ruling, although the US position could shift. Any shifts may not come in the near term though given US President Trump is scheduled to visit China for a leaders summit with China President Xi at the end of March.

- Today on the data front, we have the 1yr and 5yr LPR outcomes. No change is projected but risks are seen towards lower rates in coming months.

BONDS: NZGBS: Little Changed Despite Risk-Off Induced Rally For US Tsys

NZGBs are unchanged despite US tsys finishing 2-6bps richer, with the 5-10-year zone leading.

- US tsys were buoyed by risk-off sentiment although they nudged a couple of bps higher on Axios reporting Kushner and Witkoff are urging Trump to give diplomacy a chance in US-Iran negotiations.

- Fresh catalysts for the latest push lower in yields have been limited although it looks to be an extension of moves following President Trump's latest tariffs comments, starting with threats of much higher tariffs and worse for any country that wants to “play games” before the lack of needing congressional approval.

- WTI futures have also pulled back after sizeable gains earlier, with US-Iran tensions firmly in focus ahead of Thursday’s indirect talks in Geneva.

- Today in the US sees multiple data releases (likely highlighted by weekly ADP and the Conference Board Consumer survey), Fed Governor Cook speaking on AI and 2Y supply.

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for April, while December 2026 assigns 27bps.

- The local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.25% May-34 bond.

Bloomberg Finance LP