BOJ: Fixed Rate Purchase Offer

The BoJ offers to buy an unlimited amount of 5- to 10-Year JGBs at a fixed rate of 0.50%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

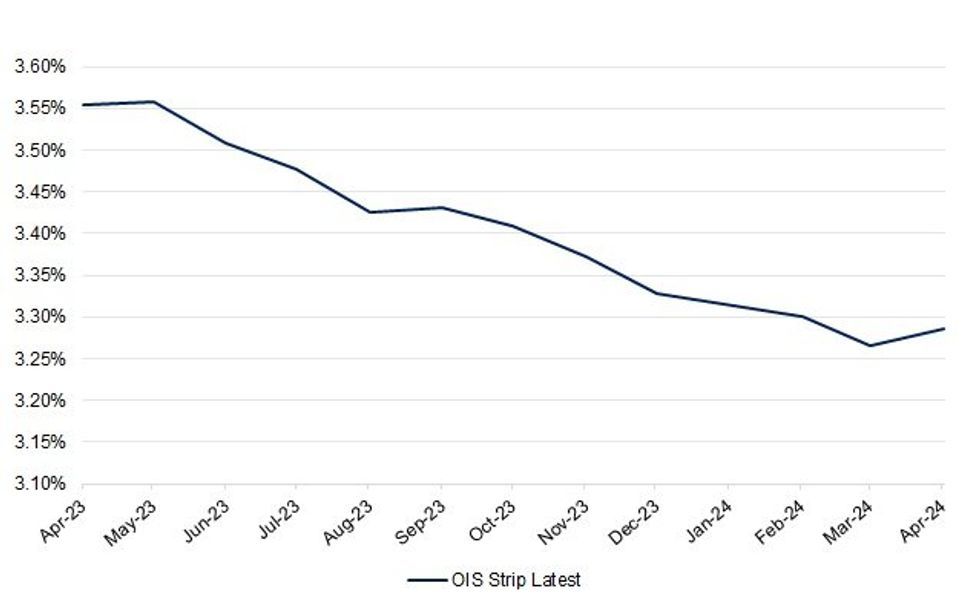

STIR: RBA-Dated OIS Strip Calls Time On RBA Hiking Cycle (For Now)

Fallout from the SVB collapse leaves the RBA-dated OIS strip calling time on the RBA’s rate hiking cycle, with 1-2bp of easing now priced for next month’s central bank gathering, while a 25bp cut is now essentially fully priced for the Bank’s December meeting (RBA-dated OIS covering meetings from August currently all price more than a 50% chance of such a step).

- A softer NAB business confidence reading (moving into negative territory) will do nothing to push back against this pricing, given that the RBA included it on the list of must-watch data re: monetary policy assessment. The survey collator noted that “while we expect inflation likely peaked in Q4, price growth remains elevated and the survey suggests that while global goods-side pressures have abated somewhat, there has been less evidence of easing in services-side pressures. NAB continues to expect a more material slowdown in demand, but this will likely come later in 2023 when the full effect of rate rises has passed through.”

- U.S. CPI data (due Tuesday, NY Time) will be key for the short-term outlook of market pricing re: global monetary policy settings.

Fig. 1: RBA-Dated OIS Strip

| OIS Strip Latest | |

| Apr-23 | 3.56% |

| May-23 | 3.56% |

| Jun-23 | 3.51% |

| Jul-23 | 3.48% |

| Aug-23 | 3.43% |

| Sep-23 | 3.43% |

| Oct-23 | 3.41% |

| Nov-23 | 3.37% |

| Dec-23 | 3.33% |

| Feb-24 | 3.30% |

| Mar-24 | 3.27% |

| Apr-24 | 3.29% |

Source: MNI - Market News/Bloomberg

STIR: SFRJ3 Covered 95.250/94.875 Put Spread Lifted

SFRJ3 95.250/94.875 put spread covered 95.62 15% delta, paper paid 11 on 12750, taken bid over.

JGBS: 10-Year JGB Yields Tumble Further Away From YCC Cap

Tokyo reacts to the precipitous falls in core global FI yields in early trade, with 10-Year yields now showing below 0.20%, the first such instance observed since August. The major cash JGB benchmarks are running 1-15bp richer as 10s lead the rally. Swap spreads are mixed, tightening between 2- to 5- and in the 30+-Year zone, while running wider in between. JGB futures tested their overnight high before backing off. Questions will begin to swirl re: the longevity of this move, given expectations for a further BoJ YCC tweak (we are now comfortably below the YCC cap that the BoJ defended until Dec), although if the SVB failure proves to be the straw that breaks the camel’s back when it comes to the global hiking cycle then market pressure on the BoJ could remain somewhat subdued, at least in comparable terms vs. what we have seen in recent months. If we see repricing re: global central banks reversing then expect fresh shorts to be set after what seems to be a bit of a position clear out in the latest rally.