US: FED Reverse Repo Operation

Feb-22 18:49

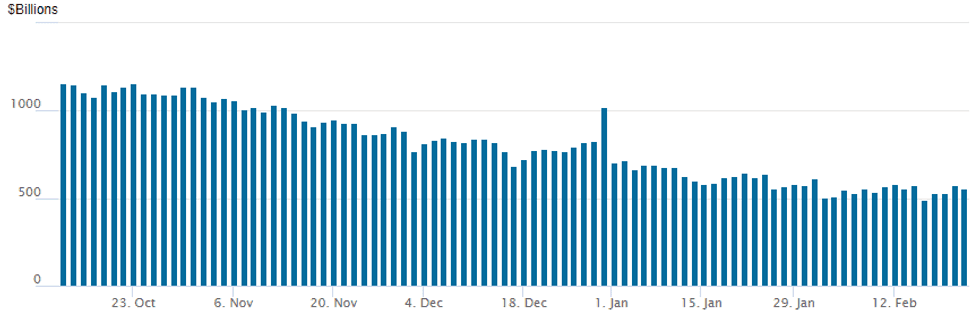

- RRP usage recedes to $553.245B vs. 574.882B Wednesday; compares to $493.065B on Thursday, Feb 15 -- the lowest since early June 2021 .

- Meanwhile, the latest number of counterparties falls back to 86 from 96 yesterday (compares to 65 on January 16, the lowest since July 7, 2021).

NY Federal Reserve/MNI

NY Federal Reserve/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: WTI Reversal Does Little To Dent Bear Steepening

Jan-23 18:40

- WTI has continued to reverse having topped out close to recent highs at around 1120ET, moving back to circa $74/bbl for down almost 1% on the day.

- Our commodities team note the return of Libyan production from the Sharara field and a gradual return from North Dakota is offsetting Middle East tensions and loading disruptions in Russia from Ukrainian attacks.

- The intraday pullback has done little to dent the day’s bear steepening in Tsys, sitting 0.5-6bp cheaper on the day.

GBPUSD TECHS: Support Remains Intact For Now

Jan-23 18:30

- RES 4: 1.2996 High Jul 27

- RES 3: 1.2881 76.4% retracement of the Jul 14 - Oct 4 bear leg

- RES 2: 1.2827 High Dec 28 and the bull trigger

- RES 1: 1.2737 High Jan 16

- PRICE: 1.2666 @ 15:54 GMT Jan 23

- SUP 1: 1.2597 Low Jan 17 and key short-term support

- SUP 2: 1.2525 38.2% retracement of the Oct 4 - Dec 28 bull phase

- SUP 3: 1.2500 Low Dec 13

- SUP 4: 1.2432 50.0% retracement of the Oct 4 - Dec 28 bull phase

GBPUSD remains above 1.2597, the Jan 17 low. The pair has pierced a key short-term support at 1.2611, the Jan 2 low and traded below the 50-day EMA, at 1.2628. The latest recovery is a bullish development, however, a clear breach of 1.2628/11 support would highlight a S/T top and signal scope for a deeper retracement, opening 1.2500, the Dec 13 low. Key resistance is 1.2827, the Dec 28 high. A break would resume the uptrend.

US TSYS/SUPPLY: 2Y Auction: On The Screws With Mixed Internals

Jan-23 18:08

2Y Tsys unchanged on the auction results, having rallied marginally ahead of them - yields +0.9bp on the day. Mixed internals for the auction, with a low bid-to-cover but strong indirects take.

- The $60B 2Y auction sees a high yield of 4.365% vs WI 4.365%. Coming in on the screws, it’s in line with the five-auction average of 0.0bps and after stopping through by 0.6bps in Dec.

- The bid-to-cover is on the low side at 2.57x, compares to 2.68x from Dec and a five-auction average of 2.70x. Lowest since Nov and before that March.

- However, dealer take also on the low side: 14.83% (lowest since Sep) vs 18.6% Dec and five-auction av 16.8%.

- Indirects take: 65.30% (highest since July) vs 61.85% Dec and five-auction av 62.3%

- Directs take: 19.87% vs 19.5% Dec and five-auction av 20.9%

- The $60B sale is the largest since Oct’21. Ahead of next week’s quarterly refunding announcement, consensus is aligned on a further $3B monthly upsizing for the upcoming quarter.