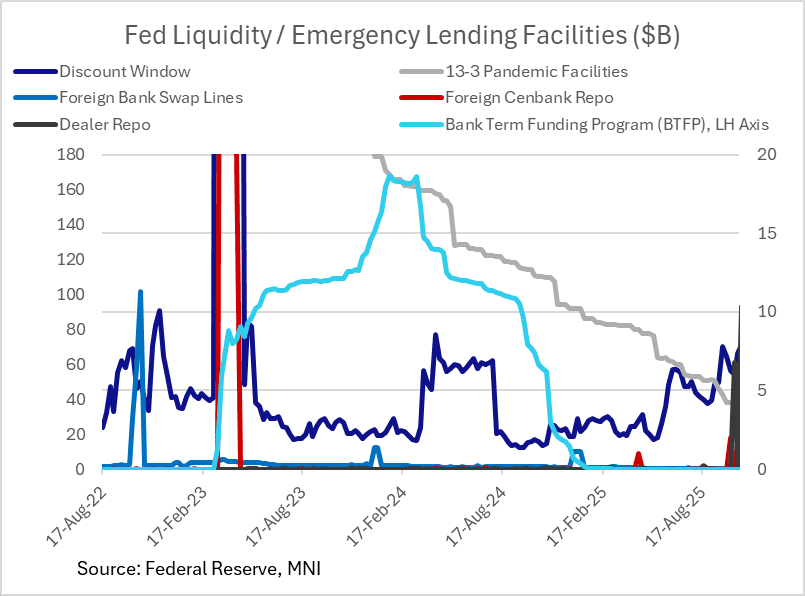

FED: Fed Assets Pull Back, But Reserve Management Buys Eyed In 2026 (2/2)

Indeed NY's Williams has already begun pointing to potential for balance sheet re-expansion to begin again, with "reserve management" purchases intended to keep Fed liabilities rising in line with market demand:

- "Looking forward, the next step in our balance sheet strategy will be to assess when the level of reserves has reached ample. It will then be time to begin the process of gradual purchases of assets that will maintain an ample level of reserves as the Fed’s other liabilities grow and underlying demand for reserves increases over time. Such reserve management purchases will represent the natural next stage of the implementation of the FOMC’s ample reserves strategy and in no way represent a change in the underlying stance of monetary policy."

- The prevailing consensus is that such reserve management purchases will begin by the end of Q1 2026 if not earlier, with t-bills bought and in amounts of up to $20B a month.

- Meanwhile in the final countdown to the end of QT on December 1, net SOMA runoff was around $4B in the last week, with a pace of around $20B overall over the last month.

- Takeup of the Fed's lending facilities pulled back in the week to Wednesday Nov 5, halving to just over $11B as month-end pressures abated. This was due almost entirely to a $10.2B drop in dealer repo operation takeup, the spike in which last week marked the highest since 2020.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH Maintaining Uptrend As Onshore Markets Return

Onshore China markets return today after the National Day break (after being out since last Wednesday). Spot USD/CNH tracks near 7.1490 in early Thursday dealings, maintaining a modest uptrend that has been in place since mid Sep. We are just above 50-day EMA resistance, while the 100-day point is close to 7.1670. The 20-day EMA support point is close to 7.1360/65, while late Sep lows, near 7.1190, might need to be tested to challenge near term thinking around dips being supported in the pair.

- The USD BBDXY index is up around 0.90% since China markets went off. Spot USD/CNY finished up at 7.1224 last Tuesday. Focus will be on the USD/CNY fixing in light of the dollar rebound. This bias is likely to be for the yuan to exhibit a low beta with respect to these USD gains. USD/CNH is only up around 0.30% over this period.

- CNH/JPY made fresh highs of 21.39 on Wednesday, but sits back at 21.3480 in latest dealings, consolidating its recent break above 21.00. Yen remains on the backfoot amid onshore political uncertainty, as well as better risk on tones.

- Anecdotes around China spending during the recent holiday period were mixed, via BBG from late yesterday: "Sales at key retailers and restaurants grew just 3.3% during the first four days of the holiday, according to the Commerce Ministry, nearly half the growth pace seen during the Labor Day break in May."

- The local data calendar has Sep new loans/aggregate finance due from the 9th to 15th of Oct. Next week we get trade figures on Monday, followed by inflation data on Wednesday (both for Sep).

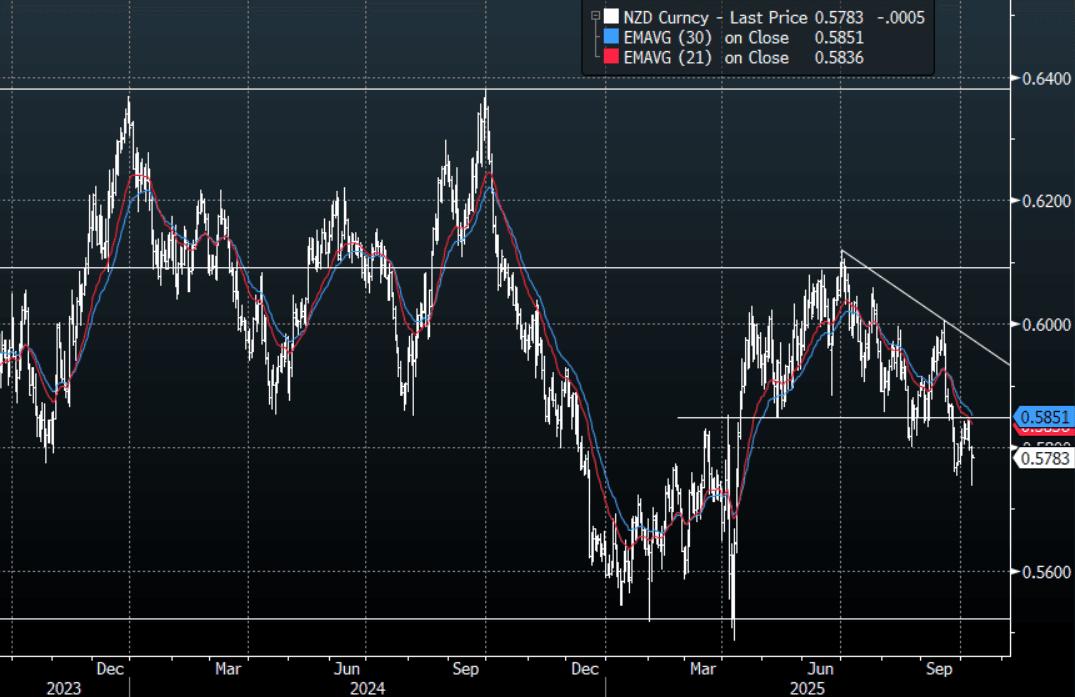

NZD: NZD/USD - Finds Demand Below 0.6750, Look For Sellers Above 0.5800 Again

The NZD/USD had a range overnight of 0.5737 - 0.5788, Asia is trading around 0.5785. US equities cannot be kept down and surged to new highs again regaining momentum after they looked to have stalled. The USD did really react to this, consolidating its recent gains. After falling over 1% on the surprise RBNZ cut, the NZD found strong demand just below the 0.5750 area and has bounced overnight as risk looks to regain its momentum higher. That does look like an ugly shadow on the Daily chart but I suspect rallies will continue to be faded while we remain below 0.5850. The NZD remains one of the stand out vehicles to express a short, again you just have to decide what against.

- MNI RBNZ WATCH: MPC Strengthens Easing Bias With 50bp Cut. The RBNZ will closely watch the Q3 CPI, due Oct 20, which it expects at 3.0%, and the Q3 labour market report on Nov 5, which the August statement forecast to show a 5.3% unemployment rate, ahead of its next and last meeting for 2025.

- Bloomberg reports banks are lowering their expected cash rates in response to yesterday: “Some Economists Expect RBNZ Will Cut Cash Rate to 2% or Lower. Citi economists expect the OCR will fall as low as 1.75% in early 2026. JPMorgan economists expect the OCR will drop to 2% in February.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Gold Rallies As US Shutdown Continues, Holding Above $4000

Given its usual relationship with the US dollar and Treasury yields, gold should have been subdued on Wednesday. The USD BBDXY rose 0.1% and the 2-year yield was slightly higher. Instead gold decisively breached $4000 reaching a high of $4059.31/oz and rose 1.4% on the day to $4042.03. The next level to watch is $4074.5, a Fibonacci projection. Political uncertainty in the US, France and Japan are driving safe-haven flows into precious metals.

- The US has been the major contributor to gold’s rally with the Fed resuming rate cuts and the September minutes signalling that most FOMC members expect more easing before year end.

- President Trump’s interference in the central bank with his attacks on Chair Powell and attempt to remove Governor Cook has also rattled markets. The ongoing government shutdown is the latest driver of bullion with no imminent end apparent and the subsequent delay in economic data clouding the economic picture.

- France’s President Macron is due to name a new PM by the end of the week but that is unlikely to solve the parliamentary impasse, especially on the budget.

- There has also received long-term support with increased central bank purchases of gold, especially from PBoC, which are expected to continue.

- Silver is up 2.2% to $48.887 after a high of $49.551, above round number support at $49.00, and is up 4.8% this month similar to gold’s +4.7%. Silver remains in an uptrend with the bull cycle extended this week and the next level to watch is the April 2011 record high at $49.804.