JAPAN: Fair To Say Japan's Economic Policy Has Changed - Takaichi

New Japan PM Takaichi was speaking in parliament earlier and stated that it is fair to say that the country's economic policy has changed (via BBG). Takaichi stated that a single year goal of a primary government budget surplus was being abandoned and rather the focus would be on a multiple year horizon (for such an objective). Other points Takaichi noted was that, nominal growth should be stronger than JGB yield levels, while she also planned to bring down the country's debt to GDP ratio (per BBG). Earlier she remarked that Abenomics had not generated strong enough economic growth, with Covid impact impacting momentum.

- The mantra of the Takaichi regime has been expansive but responsible fiscal policy. Focus will be on the first extra budget of the Takaichi regime, which is expected before the end of this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

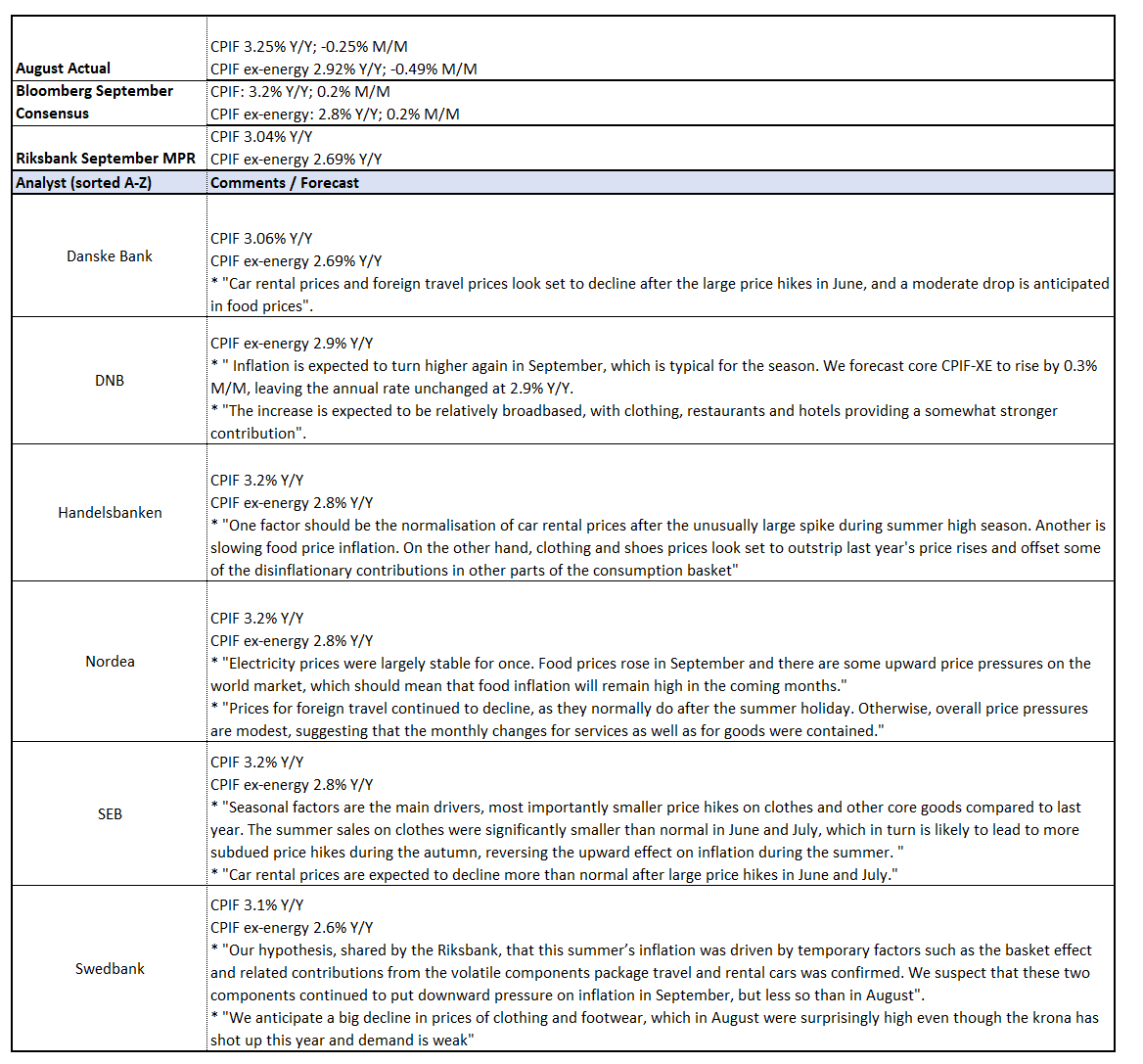

SWEDEN: September Flash Inflation Due At 0700BST/0800CET; No Fireworks Expected

Swedish flash September inflation is due at 0700BST/0800CET, but is not expected to be a major market mover. The Riksbank has signalled that it is likely to remain on hold going forward, after delivering a 25bp cut to 1.75% in September. The Board will require a much larger stock of data than one inflation report to consider deviating from this stance.

- Analysts expect CPIF ex-energy inflation to ease to 2.8% Y/Y (vs 2.9% in August). The Riksbank’s September MPR projects a larger deceleration to 2.7% Y/Y.

- A continued pullback in volatile components such as car rentals and package holidays are expected to contribute to disinflation in September. These components drove the inflation uptick over the summer, but the Riksbank assesses these dynamics to have been temporary.

- There is some uncertainty amongst analysts around the contribution from the clothing and footwear component in September (see image for more).

- CPIF ex-energy is expected to fall significantly below target next year due to the Government’s temporary food VAT tax cut. The Riksbank will look through associated swings in annual inflation rates. Indicators of price pressures (e.g. Economic Tendency Indicator expected prices) point to subdued underlying inflationary pressures ahead.

- As always, the flash release does not contain any details. The final report is due on October 15.

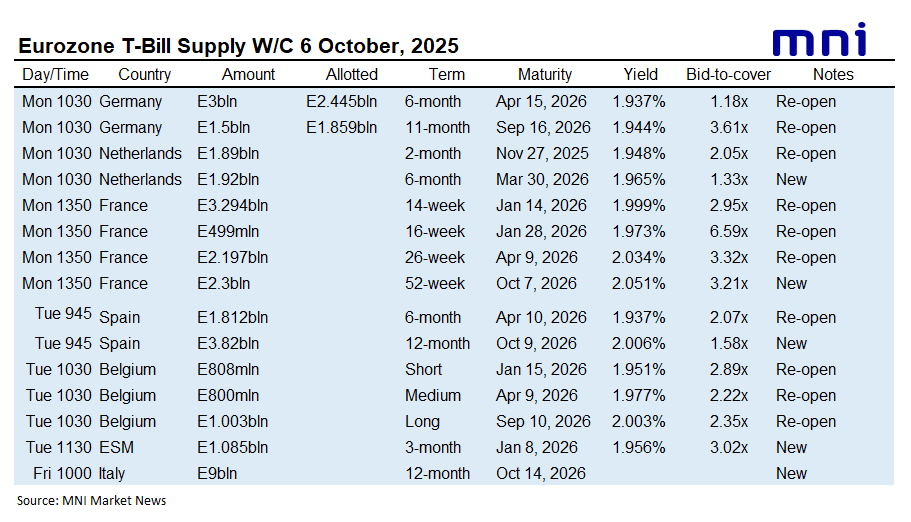

EUROZONE T-BILL ISSUANCE: W/C 6 October

Italy is still due to sell bills this week, while Germany, the Netherlands, France, Spain, Belgium, and the ESM have already come to the market. We expect issuance to be E34.9bln in first round operations, up from E11.1bln last week.

- To conclude issuance for the week on Friday, Italy will look to sell E9bln of the new 12-month Oct 14, 2026 BOT

EURGBP TECHS: Support At The 50-day EMA Remains Exposed

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8769 High Jul 28 and the bull trigger

- RES 1: 0.8751 High Sep 25

- PRICE: 0.8677 @ 06:33 BST Oct 8

- SUP 1: 0.8673/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8633 Low Sep 15

- SUP 3: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 4: 0.8540 Low Jun 30

The latest pullback in EURGBP appears corrective and the trend condition is bullish. Attention is on initial firm support at 0.8673, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement. Note that the key trend support lies at 0.8597, the Aug 14 low. A breach of this level would highlight a stronger reversal. For bulls, key resistance and the bull trigger is 0.8769, the Jul 28 high.