GERMAN DATA: Exports To US Rebound To Some Extent In September

The German trade surplus was smaller than expected in September, at 15.3bln (seasonally-adjusted, vs E16.7bln cons) following a downwardly revised August (E16.9bln, revised from E17.2bln). The decrease on a sequential comparison came as an imports jump (3.1% vs 0.5% cons; -1.4% prior, revised from -1.3%) outpaced an exports uptick (1.4% vs 0.5% cons; -0.8% prior, revised from -0.5%). Despite the September uptick, exports remain below Q2 levels in Q3 (on a nominal basis) after Destatis highlighted the series' negative contribution to Q3 GDP in their flash release.

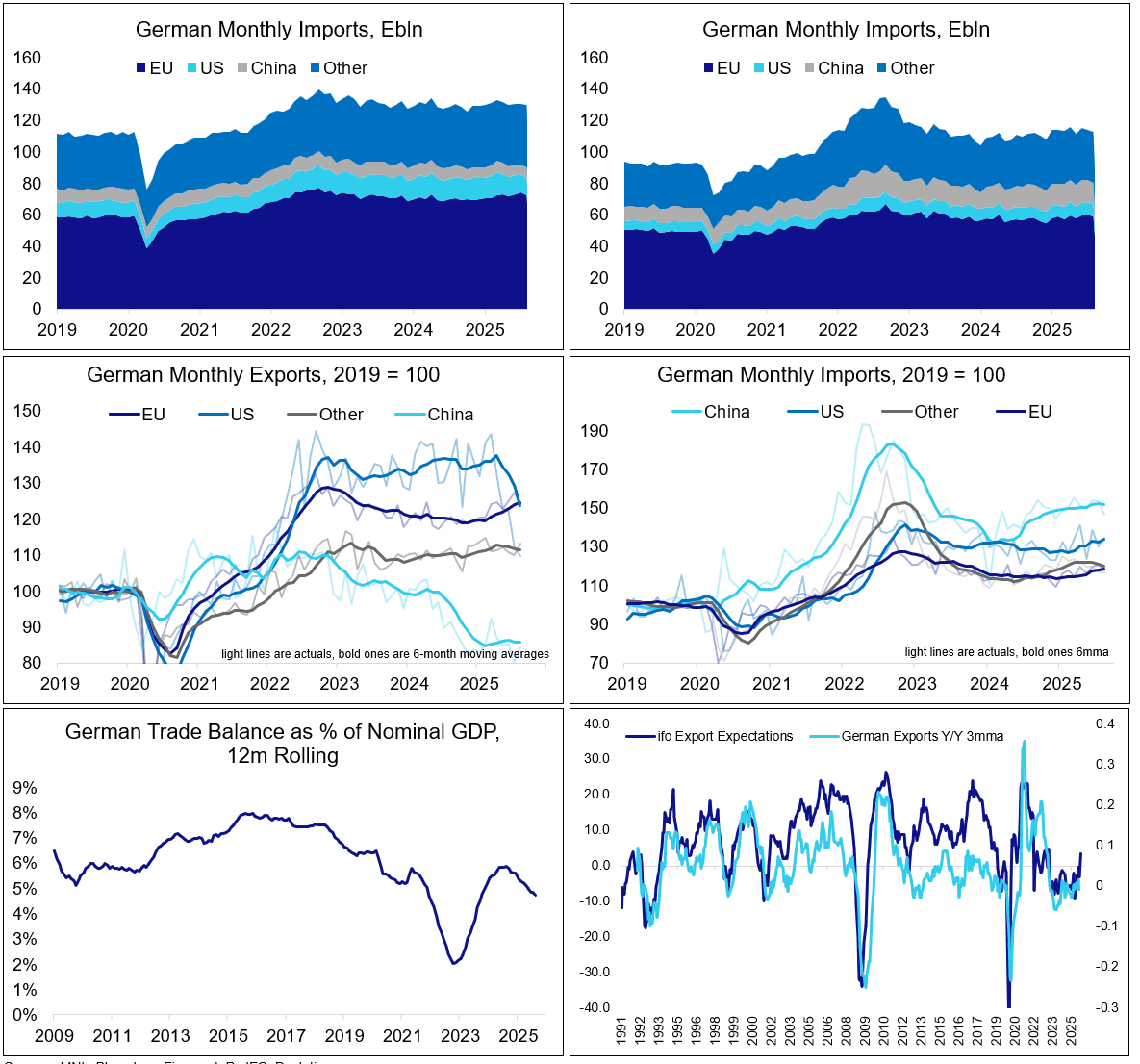

- As a % of nominal GDP on a 12-month rolling basis, the trade surplus extended its current downtrend, at 4.7% as of September, 1.2pp below levels seen around a year ago. That compares with a 2015 high of 8.0% and 2022 low of 2.1% (see bottom left chart).

- Across countries and back on a nominal basis, German exports to the US rebounded to some extent, at +11.9% M/M following five consecutive sequential declines which amounted to a 23.6% drop. While it is not clear if the series will make up fully for its previous losses, the September data points towards some stabilization at least. The 6 month moving average of the series continues to decline, however (mid-left chart).

- Exports to China were weak in September, at -2.2% M/M after an unusually strong August (+5.5%). The series has been on a longer-term decline since 2022 with little pointing towards an imminent, substantial reversal here. A recent postponement of German foreign minister Wadephul's China visit has raised concerns of a deterioration of DE - CH relations; expectations are for the visit to go ahead ultimately though, with Chancellor Merz to follow at some stage.

- Exports to Eurozone countries rose by 2.5% M/M, making up for their August decline of similar size. On a 6-month moving average trend basis, German exports to the EU continue to be on an uptrend (but remain below 2022 highs).

- Imports meanwhile saw broad-based increases in September, rising 9.0% from the US, 6.1% from China and 1.2% from the EU (vs 1.8%, -3.8% and -1.8% in August, respectively).

- IFO export expectations fell by 0.6 points to 2.8 in October. While the index is off its cycle lows, IFO continues to remain on the pessimistic side regarding German export prospects, commenting "there is no real recovery in sight."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Correction Off Recent Lows for WTI Futures Considered Corrective

WTI futures have recovered from the most recent low print - a correction. A bearish theme remains intact. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains in play and this week’s breach of $40000.0 reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum remains in overbought territory and moves sideways - a bullish signal. Sights are on $4074.54, a Fibonacci projection. Support to watch is $3775.3, 20-day EMA.

- WTI Crude up $0.58 or +0.94% at $62.31

- Natural Gas up $0.03 or +0.8% at $3.526

- Gold spot up $53.38 or +1.34% at $4037.47

- Copper up $2.2 or +0.43% at $511.85

- Silver up $0.95 or +1.99% at $48.7596

- Platinum up $18.75 or +1.15% at $1645.77

EQUITIES: E-Mini Trend Condition Unchanged, Direction Remains Upward

Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high. The trend condition in S&P E-Minis is unchanged and the direction remains up. Recent fresh cycle highs confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6700.59. It has recently been pierced, a clear break of it would signal scope for a deeper pullback.

- Japan's NIKKEI closed lower by 215.89 pts or -0.45% at 47734.99 and the TOPIX ended 7.75 pts higher or +0.24% at 3235.66.

- Across Europe, Germany's DAX trades higher by 66.25 pts or +0.27% at 24450.78, FTSE 100 higher by 31.2 pts or +0.33% at 9514.7, CAC 40 up 47.93 pts or +0.6% at 8021.8 and Euro Stoxx 50 up 16.29 pts or +0.29% at 5629.91.

- Dow Jones mini up 70 pts or +0.15% at 46922, S&P 500 mini up 12.25 pts or +0.18% at 6773.75, NASDAQ mini up 66.75 pts or +0.27% at 25106.75.

OAT: UniCredit Point To Asymmetric Risk Profile Tilted Towards Further Widening

UniCredit deem the risks to the OAT/Bund spread as “asymmetric”, suggesting that “tightening potential appears limited, while we see several outcomes that could lead to significant widening”.

- They believe that “the appointment of a new PM would alleviate pressure on OATs, although a new government would likely lack the support to pursue a more virtuous fiscal policy”. Therefore, they “expect the OAT/Bund spread to tighten only moderately, towards 75bp or slightly tighter” on this outcome, as “a weak government, coupled with weakening fiscal fundamentals, would continue to represent a headwind for investors”.

- UniCredit suggest that a snap parliamentary election would put further pressure on OATs, “with the OAT/Bund spread likely widening to 90bp” on such an outcome. They warn that “should the election result in a divided parliament, with no party or coalition gaining a healthy majority, the spread could widen further, beyond the 90bp area”.

- They note that Macron resigning “would be the worst possible scenario for OATs, as it would represent a game changer for French political institutions and might have implications on a broader level. Such a scenario would probably trigger a flight to quality, with the OAT/Bund spread probably moving towards 110bp or beyond”.