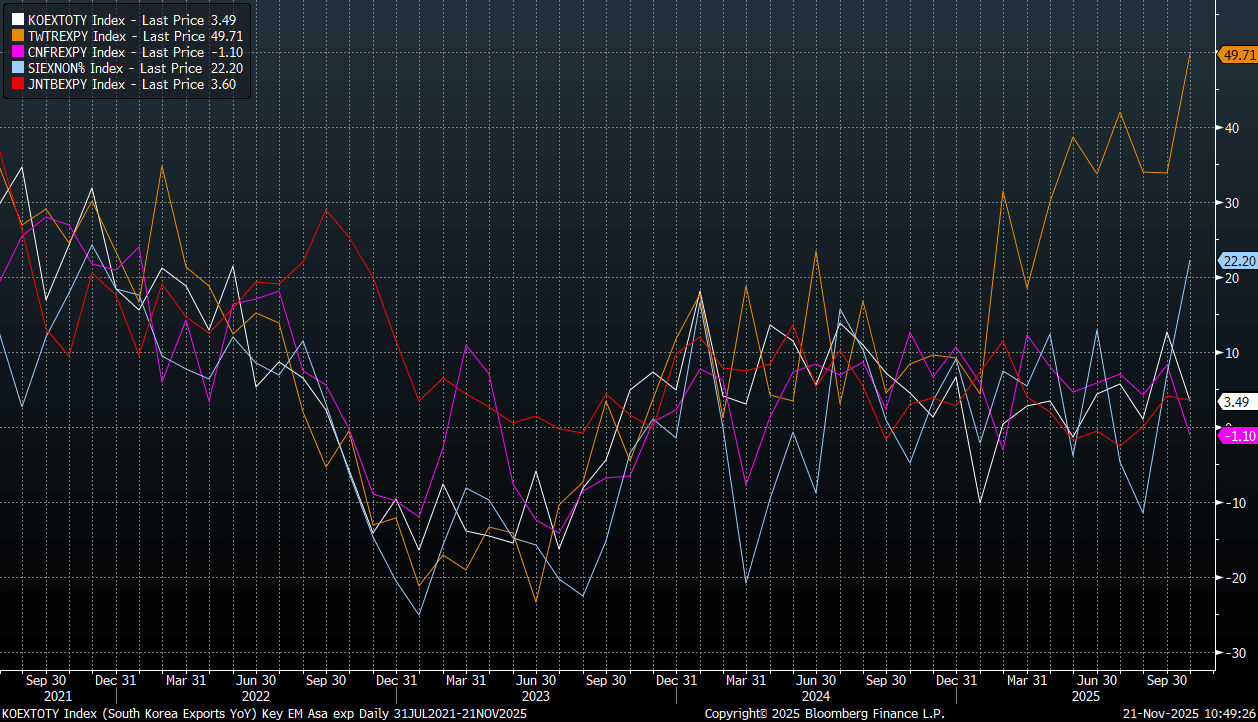

JAPAN DATA: Exports Better Than Forecast, Y/Y Momentum To US Less Negative

Japan Oct exports were better than forecast up 3.6%y/y, versus 1.1% forecast and 4.2% prior. Imports were also stronger than forecast up 0.7%y/y (-1.0% was forecast and 3.0% was the Sep outcome). For exports this broadly matches other trends seen in export orientated economies, see the chart below (Japan y/y exports is the red line). Most economies, outside of China, are up from recent lows in terms of y/y momentum, although Taiwan remains the clear outperformer. This resilient backdrop for Japan will be welcomed by the authorities, although growth rates are below 2024/2025 highs.

- The trade balance was -¥231.8bn, close to forecasts and the Sep outcome. In seasonally adjusted terms we were close to flat though, better than forecast and prior.

- Exports to the US were -3.1%y/y, to the EU 9.2% y/y and China 2.1%y/y. For the US, exports were down 13.3% in Sep, so this is an improvement. Automobile exports to the U.S. fell 7.5% y/y, pressured by trade policy, following a 24.2% decline in September. Focus will be on whether we can further sequential improvement in these trends. In volume terms, exports to the US were flat (after a 13.5%y/y decline in Sep).

Fig 1: Key Asian Economy Export Trends - Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

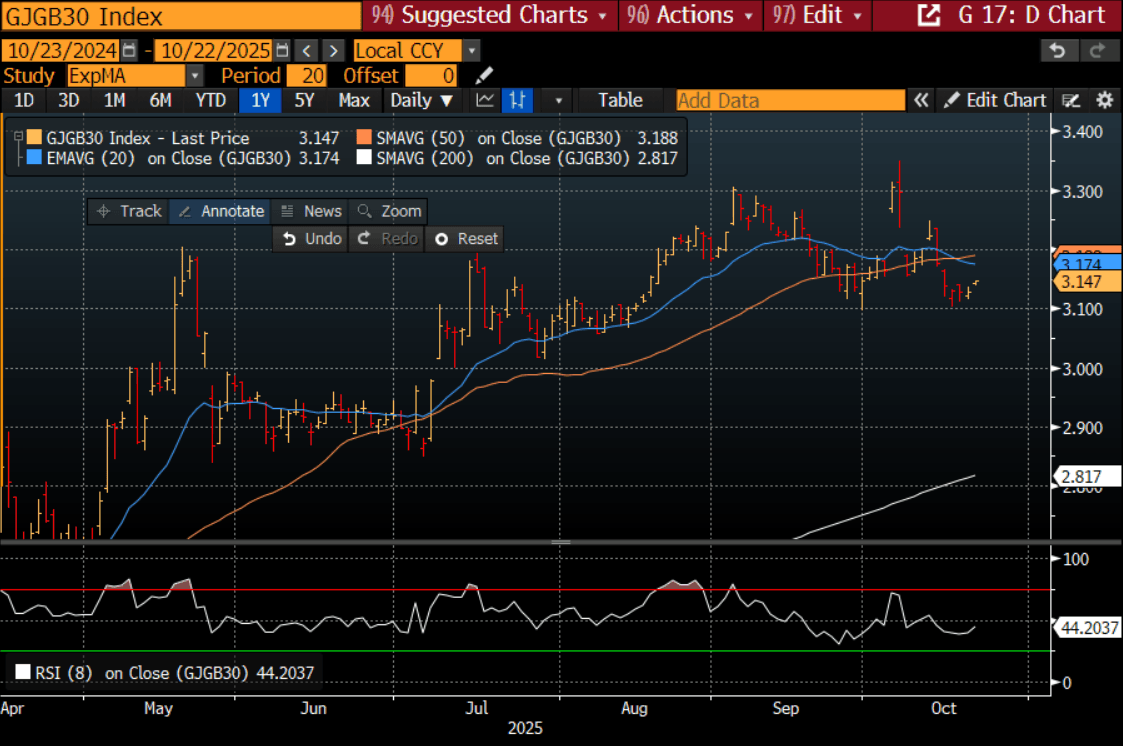

JGBS: Little Changed Out To 20Y, 30Y Cheaper But Still Well Below Highs

In Tokyo morning trade, JGB futures are weaker, -6 compared to settlement levels.

- Japan’s exports rose 4.2% in September from a year earlier, with imports +3.3% y/y. Adjusted trade deficit 314.3b yen; est. deficit 112.4b yen

- Japan's Sanae Takaichi has become the country's first female prime minister, vowing to strengthen the nation's economy and defense capabilities and enhance relations with the US. - BBG

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest bull-flattener.

- Cash JGBs are little changed across benchmarks out to the 20-year. The benchmark 30-year yield is 1.7bps higher at 3.146% but still sits way below the cycle high of 3.351%, hit shortly after Takaichi was announced as the LDP leader. (see chart)

- Swap rates are little changed.

Bloomberg Finance LP

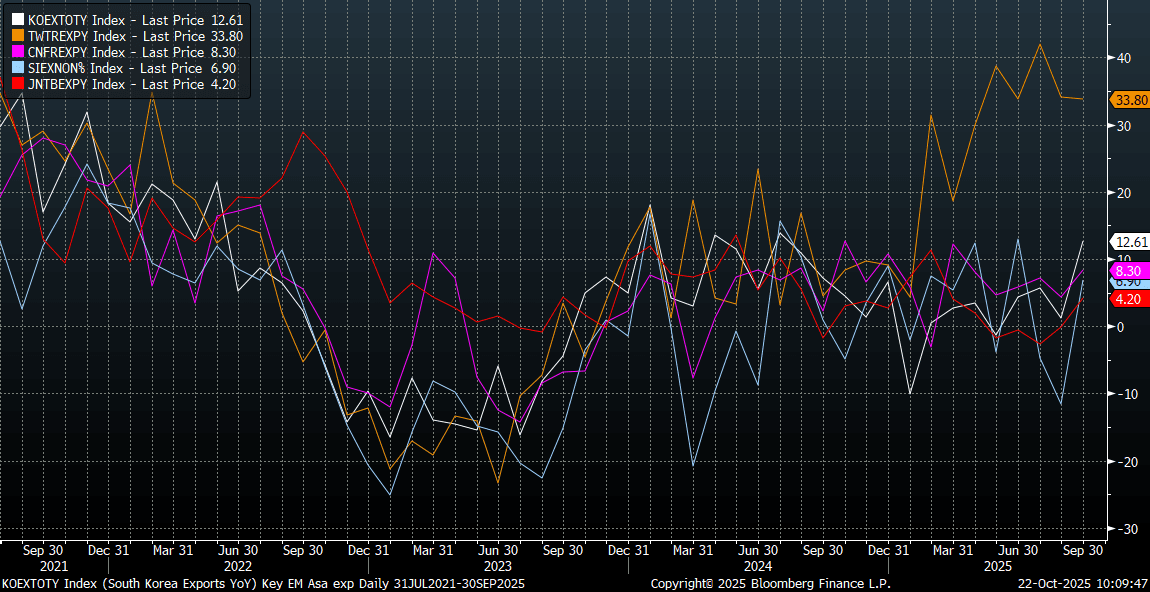

JAPAN DATA: Exports Up, Aided By Tech Shipments, Unlikely To Shift BoJ Outlook

Japan headline exports were close to market forecasts, rising 4.2%y/y (+4.4% was forecast and -0.1% was the Aug outcome). Imports were stronger than expected, +3.3%y/y (+0.6% was forecast and -5.2% was prior), which left the trade deficit positions weaker than the consensus estimates. For export growth it was the first y/y rise since April of this year, which will be welcomed by the authorities. The BoJ is watching fallout from higher US tariff levels (albeit that were lowered in Sep) on export growth. Today's outcome is unlikely to shift near term thinking around rate hike timing.

- The chart below plots export growth for key externally focused Asian economies (Japan is the red line on the chart). Japan's rebound in Sep brings is consistent with the trends for most other parts of the region, although Taiwan, the orange line, remains the standout.

- Tech/semiconductor exports were a source of strength, up 12.6%. Car exports fell 0.6%, with exports to the US fell by 13.3% (car exports to the US were off 24.2%y/y, after a 28.4% decline in Aug). Exports to China and the EU were both above 5%y/y, with tech related demand in Asia prominent.

- The trade deficit position persisted, but were around recent levels.

Fig 1: Export Growth For Key Asian Economies

Source: Bloomberg Finance L.P./MNI

GOLD: Gold & Silver Correction Continuing In APAC Session, Breached 20-d EMA

Profit taking in gold and silver begun on Tuesday has continued in Wednesday’s APAC trading with prices down 1.8% to $4052.3 and 1.0% to $48.21 respectively. The USD BBDXY is little changed but the slight decline appears to have provided a floor to the metals. Traders have been long, with the extent unclear due to the lack of CFTC positioning data due to the US government shutdown, and appear to be normalising those positions as both metals are in overbought territory.

- Gold prices fell to a low of $4004.26 as Asian markets opened, below support at $4021.6, 20-day EMA. It is currently trading above this level but another breach would open $3819.6, 2 October low. The correction is unwinding the overbought position.

- Silver reached a trough earlier at $47.550 below support at the 20-day EMA of $49.089. It continues to trade below this level opening up the 50-day EMA at $44.996. The market is smaller than gold which can exacerbate moves.