POWER: EU End of Day Power Summary: France Falls, CWE Rises on Gas

The French front-month power contract has removed initial gains to trade lower amid the early return...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

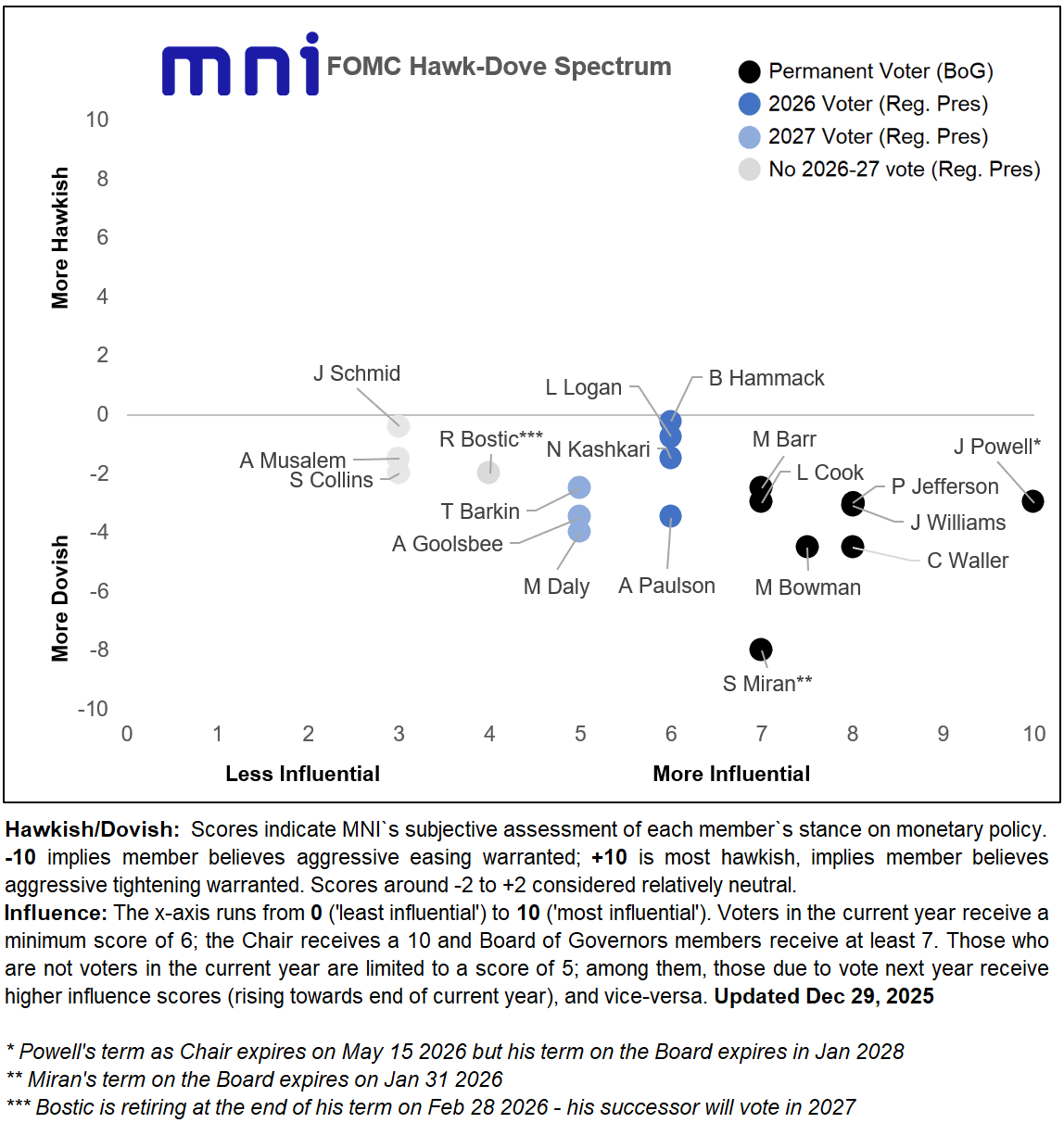

FED: Permanent FOMC Voters Lean More Dovish (2/2)

As for the 8 permanent voting members of the FOMC, we haven't heard from many of them since the December meeting (just 3) but we continue to believe they are the driving force behind signaling further cuts.

- Gov Waller, currently one of the most dovish FOMC members, said on Dec 17 that his 2026 rate dot submission was below the FOMC median (of 3.4%) at "about three", saying "maybe we're 50 to 100 basis points off of neutral. We still got some room" to ease. But "We're not seeing a dramatic decline of labor market going off a cliff...I don't think we have to do anything dramatic. If you have to do something dramatic, it's too late."

- After dissenting in favor of 50bp cuts at each of the last 3 meetings, Gov Miran said on Dec 22 he hasn't decided on whether to push for a 25bp or 50bp cut at the January meeting - he "could see voting for" 25 given that with rates having come down 75bp at the last 3 meetings "the need for me to dissent for 50 becomes less", but "I do think it's important we continue steadily reducing the policy rate". Of course, that could be Miran's last meeting if he is replaced after his term ends at the end of January.

- NY Fed Pres Williams - who recall reignited December rate cut pricing in a speech he gave in November signalling unusually clearly that he saw room for a further cut in the "near term" - said on Dec 19 that “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

- The latest major data reports have been downplayed as factors driving monetary policy thinking, with Williams noting that the latest soft CPI print as well as the tickup in the unemployment rate in November were distorted by technical factors.

- We haven't heard since the December meeting from Chair Powell, Gov Barr, Gov Bowman, Gov Cook, or Gov Jefferson. Four of those five (Barr being the exception) are more dovish leaning than the Committee as a whole.

- We use the term "permanent" to describe these 8 voters only in terms of their positions: three may not be voting too much longer including Powell (term as Chair ends in May, after which he may resign from the Board), Cook (Supreme Court hearing on Jan 21 over the White House's attempt to fire her), and Gov Miran.

FED: MNI Hawk-Dove Spectrum Update: 2026 Voters Tilt Slightly More Hawkish (1/2)

MNI's FOMC Hawk-Dove Spectrum has been adjusted to reflect the change in the voting composition between 2025 and 2026. As is usually the case following the December meeting going into the minutes, there has been only limited FOMC participant commentary due to the holiday period, but what we have heard has largely reinforced where we thought participants were on the Hawk-Dove Spectrum going into the meeting.

- We'd characterize the 2026 Fed presidential voting slate as slightly more hawkish than the outgoing 2025 rotation, contrasting with a relatively dovish Board. First looking at the regional members:

- Philadelphia's Paulson is the most dovish of the 2026 regional Fed voters, saying on Dec 12 that "I am still a little more concerned about labor market weakness than about upside risks to inflation...I continue to see monetary policy as somewhat restrictive". Paulson didn’t reveal what action she supported at the December meeting but heavily implied she would have backed the cut and that she currently envisages more easing in 2026.

- Arguably the biggest dove among 2025 Fed presidents was Chicago's Goolsbee whose stance depends on the time horizon: he is wary of further near-term easing and was one of two hawkish dissenters in favor of a hold in December, but his base case is that rates come down substantially over the coming year. (For comparison, we characterize San Francisco Fed's Daly, a 2027 voter, as more dovish than him largely because she has had more appetite for immediate cuts.) Goolsbee on Dec 12: "if you look at the dot plot, I'm one of the most optimistic folks about how rates can go down in the coming year, I'm just uncomfortable with front loading the rate cuts assuming all of the inflation that we've seen be transitory."

- Also becoming voters in 2026 are Cleveland's Hammack and Dallas's Logan who are among the biggest 3 hawks on the Committee; they are comparable to KC's Schmid who dissented against the last two rate cuts. Hammack said on Dec 12 that "we've got policy that's in that range of neutral...I would prefer to be on a slightly more restrictive stance".

- The 4th regional voter is Minneapolis's Kashkari who hasn't made monetary policy commentary since the December meeting but we assume he has maintained his relatively cautious stance after saying in November that he wouldn't have supported the October rate cut. He's probably a little more hawkish than St Louis's Musalem and Boston's Collins, who in spite of some reservations especially in October and December voted in favor of the last 3 cuts.

- Atlanta's Bostic said on Dec 16 that he would have preferred to hold rates in December and didn't pencil in any cuts in 2026, but he is retiring at the end of February meaning that his last FOMC meeting is in January.

- We haven't heard from Richmond's Barkin, Logan, Kashkari, Daly, or Musalem since the December meeting.

FED: Dec FOMC Minutes Eyed For Policy Disagreement, Balance Sheet Management

The December FOMC meeting minutes (out 2pm ET today) will be watched for confirmation that there is a high bar in the upcoming releases to a follow-up cut in January (only 4bp easing is priced).

- Our review of the December FOMC meeting is here: recall that the FOMC delivered what was widely anticipated to be a “hawkish cut”, lowering the Funds rate range by 25bp to 3.50%-3.75% while portraying a cautious stance on further adjustments in the Statement and Dot Plot.

- The main theme here is likely to be disagreement over the path forward. At the press conference Chair Powell summed up a more patient stance going forward: "We're going to get a great deal of data between now and the January meeting, and I'm sure we'll talk more about that, and that will the data that we get are going to factor into our thinking.... We're well positioned to wait and see how the economy evolves from here….We will have to see. We will get quite a bit of data."

- There were of course already several members who preferred not to ease at the December meeting, including dissenters Schmid and Goolsbee; the 2025 end-year Dot Plot saw 6 members pencil in no cut at the meeting. For 2026, while the median member saw a 3.4% end-year rate implying 1 more 25bp cut, 7 of 19 participants saw rates concluding the year at either 3.6% or 3.9% - in other words, no lower than the current level.

- The latest major data releases don’t seem to have swayed opinions one way or another, with the limited commentary we have received so far (see below) suggesting that FOMC participants are discounting the seemingly-soft CPI and unemployment readings as distorted by technical factors. That puts more importance on the upcoming December nonfarm payrolls (Jan 9) and CPI (Jan 13) releases, but even so the bar appears to be set high for a cut at the January meeting. A side note: it will be interesting to see in the Minutes if the Committee discussed their estimates of how much nonfarm payrolls are “overstated” (Powell said in the presser that monthly job gains were overstated by around 60k).

- With the biggest surprise at the meeting being the Fed’s decision to launch reserve management purchases immediately, we will be watching for the discussion that led to this move, as well whether they considered shifting administered rates (eg IORB) or implementing temporary open market operations in order to keep a lid on effective policy rates.

- MNI's full preview is here (PDF).

A few analyst expectations:

- Deutsche: “we will be looking for any information that helps to define the contours of the policy disagreements amongst the Committee”

- JPMorgan: “expected to reveal that participants continue to hold strongly differing views on the near-term policy outlook”

- TD: “will likely shed more light on the division within the Committee while signaling a majority of participants believed it would be reasonable to slow down the pace of easing”