EQUITIES: Estoxx Put buyer

SX5E (18/08/23) 4350p, bought for 20 in 15k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY DATA: Notable Stickiness In Services And Unprocessed Food (2/2)

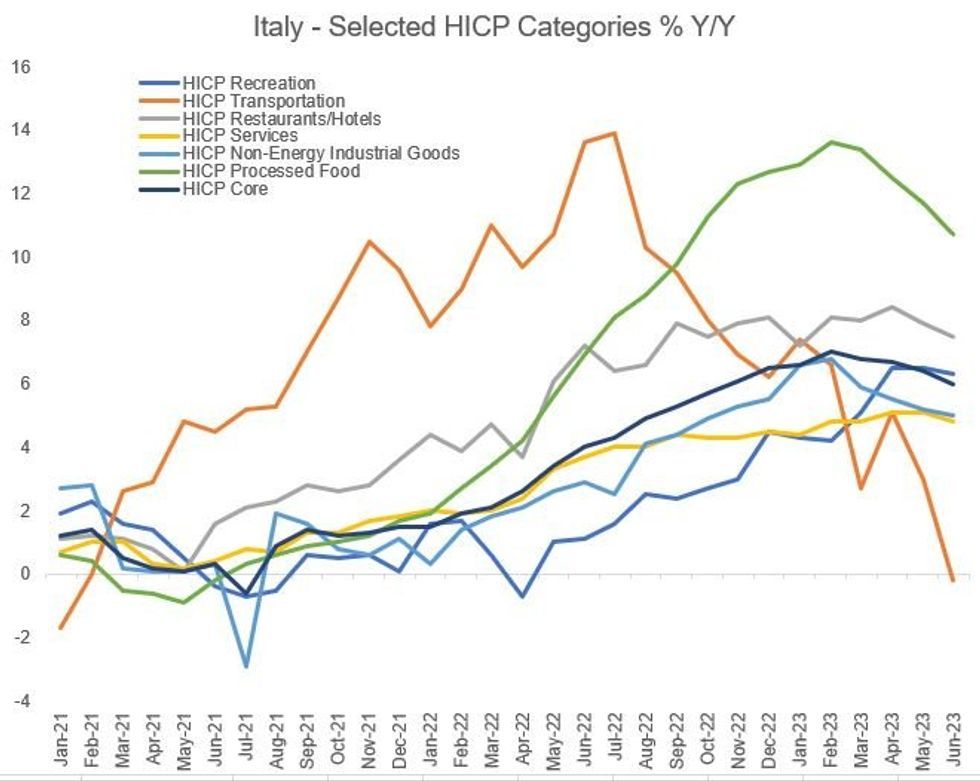

With the exception of communication (+0.5% after 0.4% in May), all of the major core categories were either steady or decelerated on a Y/Y basis.

- Recreation services (+6.3% vs 6.5% in each of the two months prior) and restaurants (+7.5% after 7.9%) also decelerated. They make up 22% of core inflation and that helped overall services HICP (47% of core) edge lower for the 2nd consecutive month at 4.8% vs 5.1% prior.

- Albeit there is still some stickiness here as Y/Y services remain well above 2022 levels which were <4%. And one would have to go back to 2012 to see readings consistently at 2% or above which is where services have printed 17 of the past 18 months.

- Transport, which is 15% of the total HICP basket, fell by 0.2% Y/Y vs 3.0% in May, marking the first negative Y/Y figure since January 2021. On a services basis alone in the CPI series, we saw a deceleration in transport to +3.8% from 5.6% prior.

- Non-energy industrial goods (35% of core) also decelerated but only modestly (to 5.0% from 5.2%).

- And while the broad grocery and unprocessed food category in CPI continued decelerating (10.7% Y/Y vs 11.2% prior), this belies an upward contribution from unprocessed foods (+9.8% in HICP vs 8.8% prior).

- On the latter, we note that some analysts had expected the recent flooding in Italy to impact on unprocessed food prices and that may have indeed been the case in June. Weather issues elsewhere including drought in Spain could come into play in this month's reading. That being said, while unprocessed food affects headline HICP, it is excluded from core.

Source: IStat, MNI

Source: IStat, MNI

ITALY DATA: Energy Leads Prices Lower, Still A Ways To Go On Core (1/2)

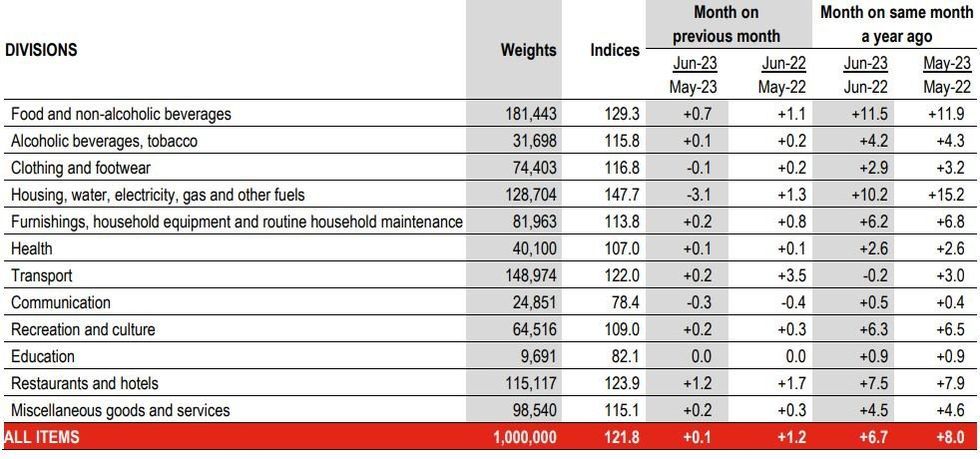

Italy's headline inflation deceleration in June to a 14-month low was faster than expected by the survey median (HICP at 6.7% vs 6.8% consensus, 8.0% prior; CPI 6.4% vs 6.7% expected, 7.6% prior). We would attribute much of the dovish market reaction to relief vs last month's surprisingly strong preliminary print (recall, May flash HICP came in at 8.1% vs 7.5% survey).

- Many analysts had expected an even bigger decline, largely on energy prices (the broad sell-side analyst headline HICP survey range of 6.4-7.2% Y/Y, with CPI from 6.4-6.9%, tells a story in itself of recent Italian inflation volatility).

- And while the report shows progress on core inflation in the 3rd largest eurozone economy (17% of the Eurozone HICP basket), there is a long way to go before it pulls back to comfortable levels.

- Indeed, energy led the way lower for Italian HICP as expected, to a post-Q1 2021 cycle low of 2% Y/Y from 11.5% prior on the back of a sharp fall in non-regulated energy products. More broadly, housing/utility costs slowed sharply (by 5pp to 10.2%).

- With most intrigue on Friday's Eurozone HICP reading surrounding German services prices, at best Italy's report keeps the bloc-wide 5.6% Y/Y headline / 5.5% core flash estimate expectation in play and perhaps nudges consensus lower a couple of tenths of a point.

- That said, June's Italy deceleration was broad-based, and core CPI slowed to 5.6% vs 6.0% in May / core HICP was 6.0% vs 6.4% prior. HICP peaked at 7.0% in February but there hasn't been a print below 2% since prior to the Russian invasion of Ukraine (Jan 2022).

Italy - June Prelim HICP DataSource: Istat

Italy - June Prelim HICP DataSource: Istat

GILT AUCTION PREVIEW: Jul 5 Details

DMO to sell the following at the July 5 auction:

- GBP4.00bln of 3.50% Oct-25 Gilt (Re-open, ISIN: GB00BPCJD880)