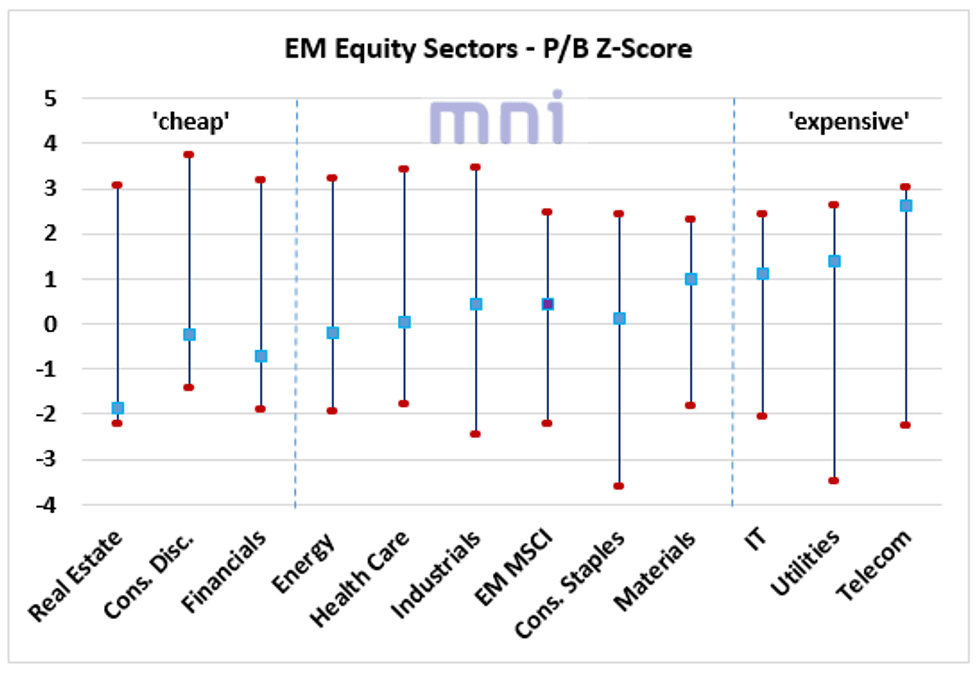

EMERGING MARKETS: Equity Sectors: Financials Remain ‘Cheap’, But Risky

- The surge in risk-aversion in recent weeks has led to a strong demand for ‘safe’ USD leaving EM equities vulnerable, which were trading at their lowest level since November 2020 this week.

- In this chart, we compute the z-score of P/B ratios of the 11 EM equity sectors (+ EM index - MXEF Index) using over 10 years of data (starting January 2010) and then rank them from 'cheapest' to 'most expensive' based on the distance between the minimum value and the current z-score.

- Real Estate and Consumer Discretionary remain the 'cheapest' sectors among the EM world:

- The drop in EM real estate stocks was mainly driven by the collapse of China developer Evergrande last year.

- Consumer Discretionary have been performing poorly in recent months as consumer confidence indicators continue to stand at 'depressed' levels due to Covid uncertainty and surging inflation.

- Financial equities, which had been mainly supported by the aggressive tightening cycle run by EM central banks to counter the inflationary pressures, have remained vulnerable in recent weeks as growth expectations are likely to be reviewed to the downside.

- Financials equities are also ‘cheap’ using our P/B z-score approach.

- On the other hand, Telecom and Utilities are the most 'expensive' sectors (both ‘defensive’ sectors).

Source: Bloomberg/MNI.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Holding Weaker Ahead Of Lowe

Futures consolidate the overnight/early Sydney dip, with YM & XM trading -4.5. The 3- to 12-Year zone of the curve provides the weak area in cash ACGB trade.

- The market remains focused on RBA Governor Lowe’s upcoming address (due in ~40 minutes time). A quick reminder that the RBA’s decision to retain “patient” in the forward guidance issued at the end of yesterday’s monetary policy decision, coupled with a lack of hawkish evolution in the guidance on the whole, provided a dovish surprise. Still, this didn’t meaningfully impact market pricing re: RBA rate hikes (we have fleshed that out previously). Markets price a 15bp cash rate hike come the end of the Bank’s June meeting, while the sell-side consensus is seemingly looking for lift-off in August.

AUD: Lowe's Comments To Grab Attention After Lack Of RBA Policy Pivot

AUD/USD clawed back post-RBA losses on Tuesday, as firmer risk sentiment and an upswing in BBG Commodity Index lent support to Antipodean currencies. The rate attacked resistance from Jan 7 low of $0.7130 into the close.

- The aforementioned resistance level has given way this morning. AUD/USD deals +10 pips at $0.7139, with bulls looking to a move through Jan 20 high of $0.7277. On the flip side, losses past Jan 28, 2021/Jul 16, 2020 lows of $0.6968/63 would provide a boon for bears.

- The Reserve Bank announced the termination of its QE programme Tuesday, but pledged patience on interest rates, while it monitors inflation dynamics. The lack of evolution in forward guidance provided a dovish surprise.

- RBA Gov Lowe will deliver an address to the National Press Club. His comments will be closely watched in the wake of Tuesday's announcement.

- Elsewhere, Australia's building approvals & trade balance are due tomorrow, while the RBA's quarterly Statement on Monetary Policy will hit the wires on Friday.

US TSYS: Tight Start

TYH2 settles into a 0-02 range early on, with thinner market conditions in play owing to the observance of the LNY holiday across several major Asia-Pac financial centres. There has been a lack of macro headline flow thus far, leaving the contract -0-00+ at 127-27+. Cash Tsys run little changed to 1bp cheaper across the curve, with modest bear steepening in play.