EU UTILITIES: Enel: 3Q25 Results

Nov-14 07:48

(ENELIM; Baa1/BBB/BBB+)

Credit neutral.

- Revenue flat YoY.

- Adj. EBITDA flat YoY. LfL +3% YTD. Cost efficiencies now 80% achieved.

- YTD FCF at €2.5bn; net debt up slightly on shareholder returns.

- Reported net leverage unchanged YoY at 2.5x. FFO/ND at 25%.

- FY adj. EBITDA guidance confirmed, with net income increased slightly.

- A new Strategic Plan will be presented in February 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

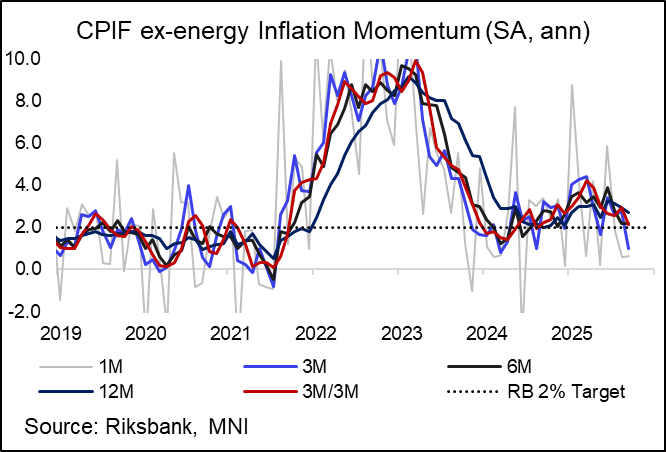

SWEDEN: CPIF ex-energy Confirms Flash; Food and Goods Drive Pullback

Oct-15 07:44

Swedish September inflation confirmed flash estimates, leaving CPIF ex-energy in line with the Riksbank’s September MPR projection at 2.70% Y/Y (vs 2.92% prior). The signal for monetary policy is neutral – we don’t expect a move away from 1.75% for at least the next few months.

- Our estimate of seasonally adjusted CPIF ex-energy inflation for September was 0.05% M/M for the second consecutive month. That pulled 3m/3m annualised inflation momentum down to a 13-month low of 2.12%.

- There was another sharp pullback in food inflation in September, to 2.66% Y/Y (vs 3.94% in August, 4.26% in June and July). This was the lowest annual rate since January.

- Meanwhile, goods inflation pressures appear soft:

- Clothing eased to 2.02% Y/Y (vs 2.95% prior) while footwear pulled back to 0.61% Y/Y (vs 4.66% prior). Monthly price developments were well below September 2024 and the 2010-2019 average for September.

- Furnishings and household equipment inflation was also soft at -2.31% Y/Y (vs -0.41% prior).

- Vehicle inflation was -0.05% Y/Y (vs 0.38% prior).

- These trends were somewhat offset by stronger annual services inflation, but we caveat that familiar volatile categories were at play:

- Car rental and international flight prices saw sequential declines for the second consecutive month (further unwinding summer strength), but Y/Y rates still accelerated relative to August.

- Meanwhile, package holidays reversed a little of August’s -22.5% M/M fall with a 3.1% rise. The annual rate became less negative at -0.49% Y/Y (vs -5.56% in August) as a result.

- Accommodation services rose 5.26% M/M, compared to a -0.62% M/M fall in September 2024. That pushed the annual rate up to 6.13% Y/Y (vs 0.2% prior).

- The proportion of subcomponents with annual inflation rates below 3% rose to 65% in September, up from 60% in August.

EQUITY OPTIONS: EU Bank Call Spread

Oct-15 07:44

SX7E (17th Oct) 232/237cs 1x2, bought for 1.15 in 3k.

GILTS: Rally Extends On Global Cues

Oct-15 07:35

Gilts follow peers higher as the reduction in short-term French political risk and late Tuesday comments from Fed Chair Powell provide support.

- Futures through resistance at 92.06 and 92.14, strengthening the recent bullish theme. Contract trades as high as 92.39.

- Fresh extension higher would target projection resistance (92.72).

- Yields 4-5bp lower across the curve.

- 10s through support at the August 11 low (4.548%). Uptrend support drawn from the Dec ’24 low is very close (4.536%). The next level of note below there is the August low (4.496%).

- 30s have broken through uptrend support drawn off the April low (5.370%) and trade ~3bp above their August low (5.309%).

- The dovish repricing in GBP STIRs extends a little further.

- SONIA futures 0.5-4.5 firmer, BoE-dated OIS showing ~10bp of easing through year-end.

- The DMO will sell GBP1.5bln of the 0.125% Aug-31 I/L line this morning.

- Comments from BoE’s Ramsden & Breeden are due later today, although the settings and topics of the discussions may limit scope for meaningful comments on monetary policy.

- A reminder that BoE Governor Bailey pointed to the trade off in managing inflation and a softening labour market late on Tuesday. He steered clear of any guidance when it comes to future interest rate decisions. Next week’s CPI data is key.