BONDS: EGBs-GILTS CASH CLOSE: Gains Fade, But UK Short-End Rally Stands Out

Jul-25 16:41

Gilts and core EGBs strengthened Thursday, with periphery spreads mostly wider.

- The session began with a risk-off tone in a resumption of the previous day's price action. Gilts and Bunds both gained, helped by an unexpected PBOC rate cut overnight, soft German IFO data, and weak corporate earnings reports - each of which underlined global growth concerns.

- Price action shifted negative in the afternoon following stronger-than-expected US GDP data, though Bund and Gilt futures partially recovered and closed higher on the day.

- The German curve bull flattened, with the UK's bull steepening.

- UK short-end outperformance was notable, with 2Y yields seeing their lowest close since May 2023 as BoE rate cut probabilities crept higher.

- Having widened in early trade, periphery EGB spreads regained ground over the course of the session as equities found their footing. BTPs underperformed, closing wider to Bunds, with PGBs outperforming.

- Looking ahead, Friday's docket includes more Eurozone consumer confidence surveys, and ECB inflation expectations.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.1bps at 2.634%, 5-Yr is down 2.2bps at 2.348%, 10-Yr is down 2.7bps at 2.417%, and 30-Yr is down 3.2bps at 2.629%.

- UK: The 2-Yr yield is down 4.1bps at 3.948%, 5-Yr is down 2.5bps at 3.917%, 10-Yr is down 2.6bps at 4.13%, and 30-Yr is down 0.3bps at 4.67%.

- Italian BTP spread up 1.1bps at 136.1bps / Portuguese down 1.2bps at 64.1bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Jun-25 16:36

- EUR/USD: Jun27 $1.0650(E2.1bln), $1.0700(E3.4bln), $1.0740-50(E2.0bln); Jun28 $1.0650(E1.3bln), $1.0670(E1.2bln), $1.0690-95(E1.3bln), $1.0715-25(E1.9bln), $1.0765-75(E1.3bln); Jul01 $1.0700(E1.5bln)

- USD/JPY: Jun28 Y158.00($1.9bln), Y160.00($2.0bln)

- GBP/USD: Jun28 $1.2645-50(Gbp1.1bln)

- USD/CAD: Jun27 C$1.3675-85($1.5bln), C$1.3700-05($1.4bln)

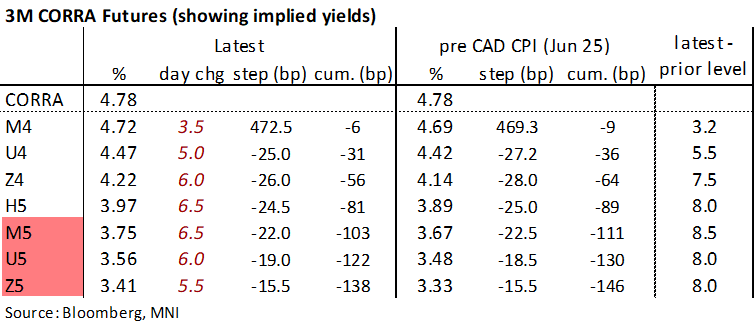

CANADA: CAD FI Pares Post-CPI Reaction, But US Differentials Still At Highs Since June BoC Cut

Jun-25 16:24

- With the stronger than expected Canadian CPI report now more fully digested, 2Y GoC yields have limited post-data increases to a still sizeable 8.9bps (for +7.4bps on the day).

- The Can-US 2Y yield differential has also trimmed some of its earlier large gains, now at -77bps having touched -73bps, but still increase from -82.5bps pre-data and would mark the highest close since the BoC cut 25bps on Jun 5.

- BoC-dated OIS meanwhile hovers around 9-10bps priced for the Jul 24 meeting (from 15bp) with still another labour and CPI round to come plus the BoC’s business and consumer surveys.

- Further out, CORRA futures have a cumulative 56bp of cuts to end-2024 and 138bp to end-2025, vs 64bp and 146bp pre-CPI.

- Perhaps complicating proceedings on the day at the margin was yesterday’s shock win for the centre-right main opposition CPC in the Toronto-St Paul by-election, having been held by the LPC since the 1993 general election.

FED: Cook – Payrolls Strength May Continue To Be Overstated

Jun-25 16:10

Fed Governor Cook (permanent voter) says it will be appropriate to cut rates “at some point” in long-awaited monetary policy relevant comments having last earnestly talked on the subject back in March. Full remarks here.

- “I believe that our current policy is well positioned to respond as needed to any changes in the economic outlook. With significant progress on inflation and the labor market cooling gradually, at some point it will be appropriate to reduce the level of policy restriction to maintain a healthy balance in the economy.”

- Bumpy disinflationary path: “My forecast is that three- and six-month inflation rates will continue to move lower on a bumpy path, as consumers' resistance to price increases is reflected in the inflation data. I expect 12-month inflation will roughly move sideways for the rest of this year, with monthly data likely similar to the favorable readings during the second half of last year.”

- Higher payrolls breakeven and overstated data: “With more workers entering the economy, the monthly job gains needed to keep the unemployment rate steady likely has risen from just under 100,000 to nearly 200,000. Although these estimates are uncertain, such a breakeven pace may be a bit higher than the true pace of recent job gains, when taking into account data from the [QCEW]. These data suggest that payroll job gains were overstated last year and may continue to be so this year. Thus, even the robust payroll numbers are consistent with a tight, but not overheating, labor market.”

- The below Bloomberg headline gets some attention but it’s the same rhetoric as her brief comments from early last month "*COOK: RISING CONSUMER DELINQUENCY RATES `BEAR WATCHING'" - bbg

Trending Top

Mar-27 20:13