BONDS: EGBs-GILTS CASH CLOSE: Bunds Soar As ECB Takes Back Seat To US Bank Woes

May-04 16:22

The German curve bull steepened sharply on ECB day, with the UK following suit but underperforming.

- The ECB decision received a mixed reception. Bunds jumped with the 25bp hike vs some lingering expectations of 50bp, and a lack of firm commitment to further tightening in the statement.

- More hawkish was Lagarde's "we are not pausing" and emphasis on requiring multiple future "decisions" to get to sufficiently restrictive territory; the announced end of APP reinvestments starting in July; and a lack of TLTRO bridging loans announced. Periphery spreads closed the day wider.

- Ultimately though US banking concerns and related equity volatility had a much bigger impact, with Treasuries pulling Bunds and Gilts to session highs in a strong risk-off move.

- Hike expectations faded, with ECB terminal dropping by 12bp and BoE 11bp - helping to drive short-end cash curve outperformance.

- Focus early Friday will be on ECB speakers (Simkus and Elderson scheduled), with the US jobs report taking centre stage later.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 16.2bps at 2.479%, 5-Yr is down 12.3bps at 2.122%, 10-Yr is down 5.7bps at 2.19%, and 30-Yr is down 0.5bps at 2.366%.

- UK: The 2-Yr yield is down 9bps at 3.678%, 5-Yr is down 8.7bps at 3.482%, 10-Yr is down 4.3bps at 3.653%, and 30-Yr is down 2.6bps at 4.069%.

- Italian BTP spread up 6.1bps at 193.2bps / Spanish up 3bps at 109.8bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: $3.84B Citrix Note Expected Today

Apr-04 16:21

- Date $MM Issuer (Priced *, Launch #)

- 04/04 $5B *World Bank (IBRD) 5Y SOFR+37 (book > $85B)

- 04/04 $3.84B Citrix 6.5Y NC 2.5Y appr 9%

- 04/04 $3B #KFW 2026 SOFR+20 (book > $10.5B at the close)

- 04/04 $2.25B *IADB 10Y SOFR +53 (book > $3B)

- 04/04 $1.25B0 #Kingdom of Jordan +5Y 7.875%

- 04/04 $600M #CNH Industrial 5Y +140

- 04/04 $Benchmark ZF North America 5Y, 7Y

- Expected to launch Wednesday:

- 04/05 $Benchmark Quebec 5Y SOFR+58a

EUROPE: Bund Futures Back To Flat As ECB Pricing Retrenches Further

Apr-04 16:17

ECB terminal hike pricing really pulling back here, now down 11bp on the day, with an October depo rate peak of just under 3.50%. That's off 14bp since pre-US JOLTS.

- Meanwhile, Bund futures have erased the session's losses and are trading flat on the day at 136.58.

- Tying this together, note that cash Bunds - which are now closed for the day - saw twist steepening, with the short-end rallying strongly as global central bank hike expectations dissipated.

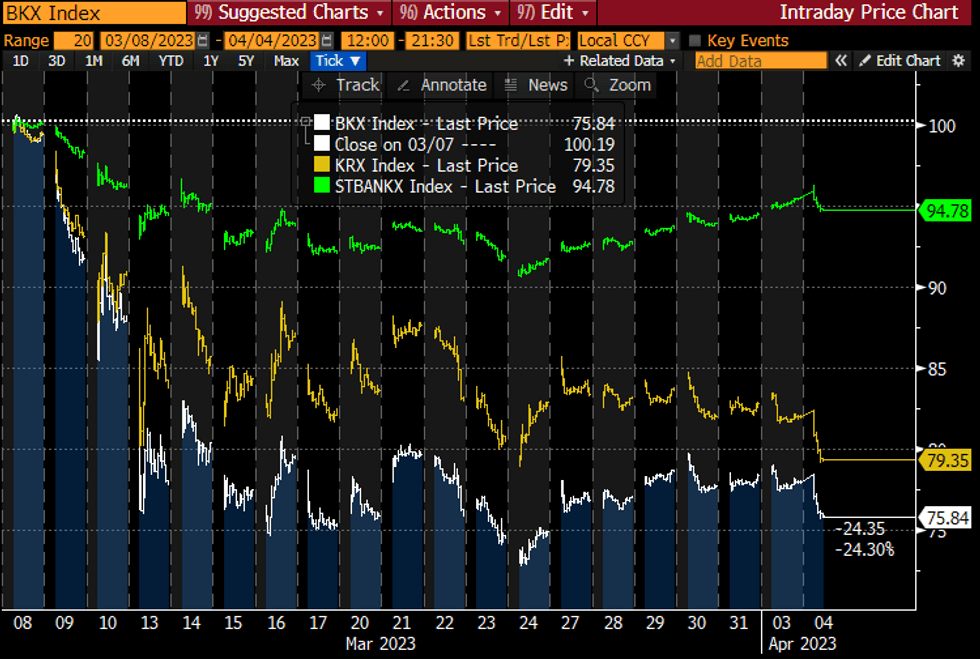

CANADA: Canadian Banks Maintaining Relative Resilience

Apr-04 15:57

- US banks being under pressure today (BKX -2.8%, regional KRX -3.3%) once again haven’t fully translated into Canadian banks (STBANKX -0.7%).

- It continues notable resilience for Canadian banks, with the price index circa 5% lower than Mar 8 levels vs roughly 20-25% declines for US bank indexes – see normalized chart.

TSX Banks (green) vs KBW Bank (white) and Regional Bank (yellow) indexes Source: Bloomberg

TSX Banks (green) vs KBW Bank (white) and Regional Bank (yellow) indexes Source: Bloomberg

Trending Top

Mar-27 20:13