EM LATAM CREDIT: Ecopetrol: Q3 2025 Earnings – Neutral

(ECOPET; Ba1/BBneg/BB+neg)

• Sales declined 13.8% and EBITDA dropped 11.8% YoY. Improved refining margins boosted profitability in the refining business with EBITDA quintupling from COP120bn to COP783bn. That offset weakness in the E&P division which was hurt by a fall in oil prices and flat production.

• Overall, net debt leverage was reported at 2.1x vs 2.2x the previous quarter while gross leverage was reported unchanged sequentially at 2.4x. The company paid less in dividends YoY, sold some investments and paid down debt to preserve its debt metrics given the weaker EBITDA generation.

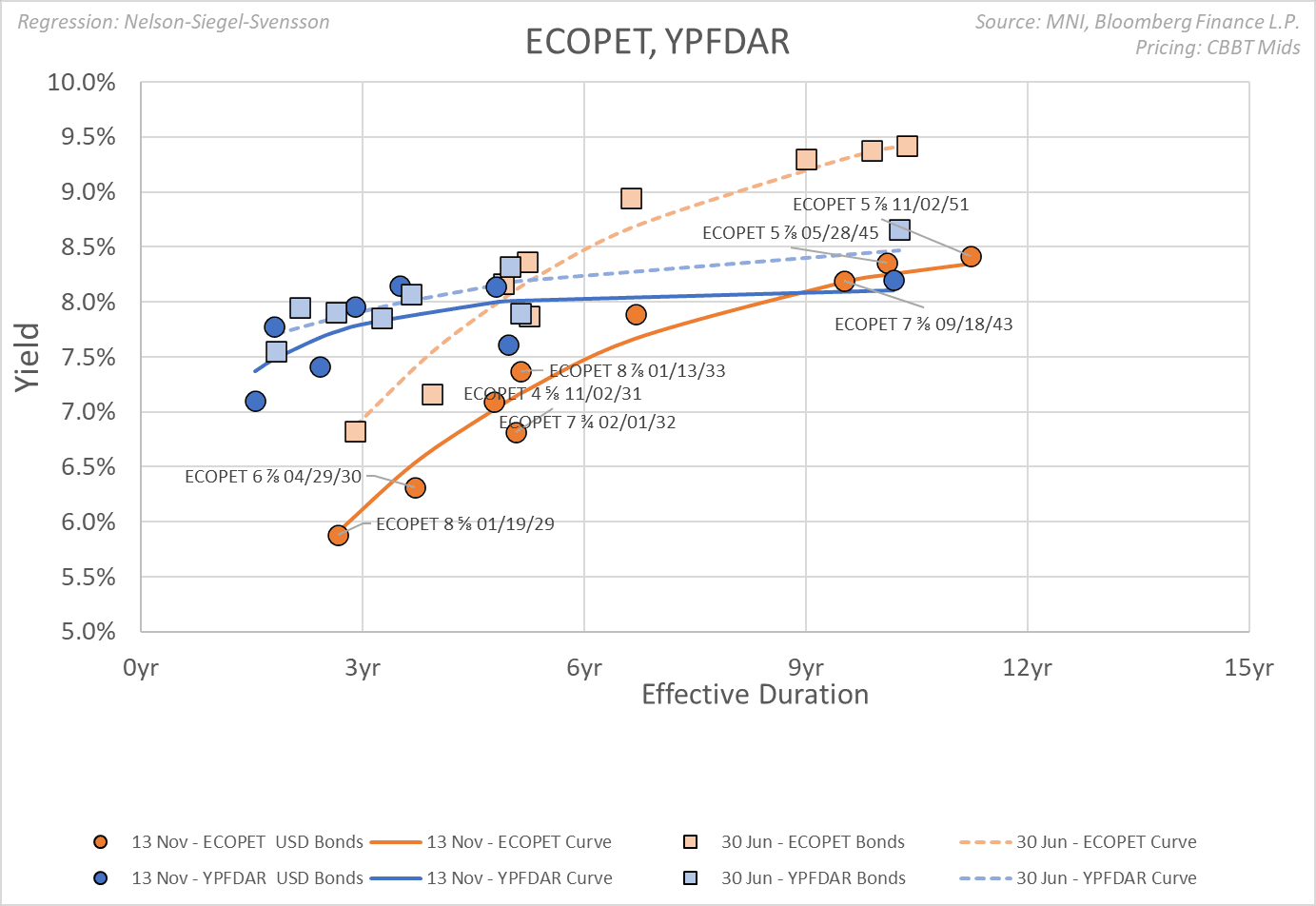

• ECOPET 36s were last quoted T+376bp, 90bp tighter since June 30th and 53bp tighter YTD. Spread to the comparable maturity sovereign was 118bp, 17bp wider since June 30th because of the govt’s buyback of USD sovereign debt these past few months. The steepness of the ECOPET curve relative to the flatter Argentina govt.-controlled YPF (YPFDAR; B2/B-/CCC+) curve is interesting with ECOPET 45s quoted at a higher yield than YPFDAR 47s, though we appreciate the lower dollar price of the YPFDAR 47s may have some influence.

• The pattern of declining domestic oil and gas production offset by U.S. Permian Basin growth persisted with quarterly domestic falling 1.3% YoY and 2% YTD while Q3 Permian grew 2.3% YoY and for nine months YTD rose 10.8%. The company denied reports that it was considering selling its interest in the Permian despite pressure from the environmentally focused Petro administration.

• Ecopetrol has a contingent liability for VAT taxes owed on the import of gasoline for about COP11.2Tn (USD3bn) in total which it has appealed and not provisioned for as the probability of a successful appeal was deemed by external advisors to be greater than 50%. We are not as sanguine but the added liability would be manageable. Gross debt leverage would rise to 2.65x from 2.4x and would have to be financed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Climbing Off Session Lows

- Treasuries are climbing off recent session lows following comments by Fed Gov Miran (voter) at a at Nomura Research Forum stated that US-China trade tensions tied to rare-earth curbs "pose significant downside risks". Ironically, this comes after after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports" helped risk sentiment earlier.

- Currently, Tsy Dec'25 10Y contract trades 113-09.5 (-3.5) vs. 113-07 low, yld tapped 4.0417% high; curves flatter/off lows: 2s10s -1.874 at 53.061, 5s30s -1.692 at 10.603.

- Initial technical support at 112-26 (20-day EMA) followed by the 50-day EMA at 112-16. A clear break of the average would expose 111-13+, the Aug 18 low and a key support.

- Cross asset: Bbg US$ index off lows, -2.77 at 1211.67, stocks claw extending lows: DJIA down 196.59 points (-0.42%) at 46030.72, S&P E-Minis down 27.25 points (-0.41%) at 6653.25, Nasdaq down 69.1 points (-0.3%) at 22429.75.

CHINA: Reflationary Process Expected to Remain Slow

- The marginally softer-than-expected headline CPI inflation data for September primarily reflected a drag from the food component, as well as a dip in transportation prices. Excluding food and energy, core consumer prices rose 0.1% on the month, with the annual rate rising to a fresh 19-month high (+1.0% y/y). Producer prices were flat on the month, with the pace of deflation narrowing as deflationary pressures in the metals and energy goods sectors lessened.

- Goldman Sachs writes that food deflation could be stronger than they previously expected for this year and next. Along with the further declines in crude oil prices that they anticipate ahead, they have revised down their full-year 2026 headline CPI forecast to 0.8% y/y (from 1.0% y/y previously). Reflecting the stronger-than-expected PPI prints, meanwhile, they slightly raise their full-year 2025/26 forecasts for headline PPI inflation to -2.6%/-0.7% y/y (from -2.8%/-1.0% y/y previously).

- Meanwhile, JP Morgan expects the reflationary process to be slow, with a likely scale-back of the government’s anti-involution (anti-excess capacity) policies, weak consumer demand, and renewed external demand pressures amid US-China tension re-escalation. Overall, they expect CPI inflation to gradually turn positive by year-end and PPI deflation to narrow further, with headline CPI averaging -0.1% y/y and PPI at -2.6% for the full year.

EURUSD TECHS: Remains Below The 50-Day EMA

- RES 4: 1.1919 High Sep 17 and a bull trigger

- RES 3: 1.1820 High Sep 23

- RES 2: 1.1779 High Oct 1 and a key short-term resistance

- RES 1: 1.1672 50-day EMA

- PRICE: 1.1621 @ 15:42 BST Oct 15

- SUP 1: 1.1542 Low Oct 9

- SUP 2: 1.1516 76.4% retracement of the Aug 1 - Sep 17 bull leg

- SUP 3: 1.1392 Low Aug 1 and bear trigger

- SUP 4: 1.1313 Low May 30

EURUSD is in consolidation mode. A bear theme remains in place following the recent breach of the 50-day EMA and a support at 1.1646, the Sep 25 low. This signals scope for a test of 1.1516, a Fibonacci retracement. Note that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend and suggests the move down is likely a correction - for now. Initial firm resistance is 1.1672, the 50-day EMA.