FREIGHT: Diverging Supply Environment Drives Clean, Dirty Tanker Rates

Nov-07 11:15

In Q4, oil markets are expected to feel the impact of increased global production reaching the water, according to International Seaways executives, cited by Platts.

- The combination of OPEC’s reversal of voluntary cuts and additional output from the Americas will support stronger tanker demand amid record oil consumption growth of around 1%, they said.

- Spot rates for VLCCs remain robust, with Suezmax and Aframax vessels benefiting from tighter availability.

- While crude, or dirty tankers are buoyed by record cargo volumes, the company is monitoring the forward curve, which remains flat and limits floating storage incentives.

- In the clean tanker market, the absence of Russian diesel has lengthened voyage routes, with the US and Latam stepping in to fill supply gaps.

- Sanctioned Russian and Iranian barrels continue to underpin elevated freight levels.

- Despite firm markets, Suezmax and LR1 earnings softened quarter on quarter, while medium-range tankers proved more resilient.

- Limited fleet growth—just 2%—and a low orderbook suggest a tightening supply outlook, reinforcing bullish conditions for tanker rates through 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

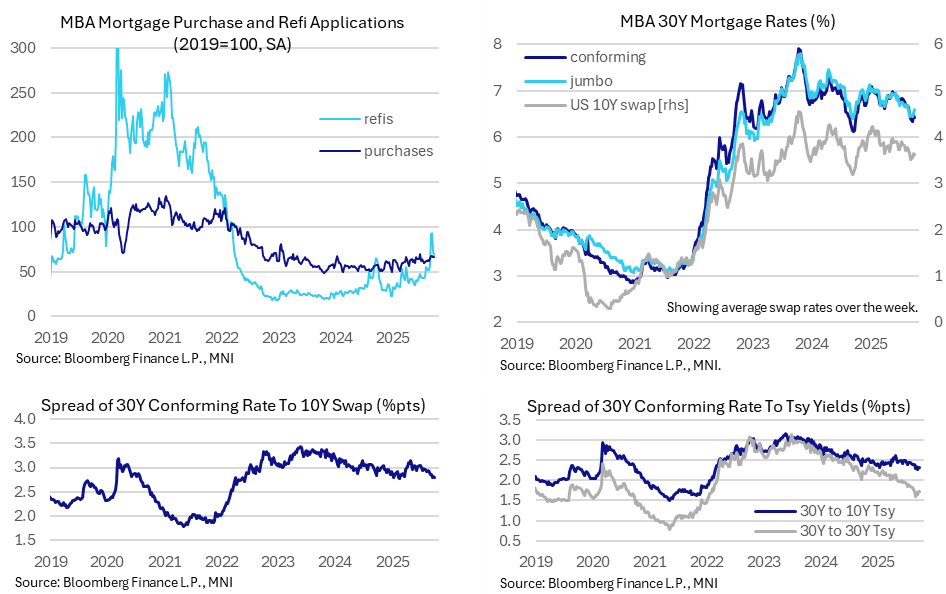

US DATA: Mortgage Applications Continue To Unwind Refi Jump

Oct-08 11:15

- MBA composite mortgage applications fell -4.7% (sa) last week as they continued to chip away at the refi-driven jump in the first half of September.

- Composite applications were -4.7% after -12.7% the week prior, following a 30% increase in the week to Sep 12 and 9% before that in the week to Sep 5.

- Refis were -7.7% after -20.6% and with respective earlier gains of 58% and 12%, whilst new purchase applications were -1.2% after -1.0% and gains of 2.9% and 6.6%.

- Levels relative to 2019 averages: composite at 68% vs a recent three plus year peak of 82% in September, refis at 68% and new purchases at 66%.

- A small decline in 30Y mortgage rates didn’t offer much support on the week, easing to 6.43% (-3bp) after a 12bp increase the previous week. The 6.34% seen in the week to Sep 19 was the lowest since Sep 2024 after a 35bp decline in four weeks starting late August.

- Interestingly, the 30Y mortgage to 10Y Tsy yield spread continues to hover marginally above 230bp having eased modestly since US Tsy Sec Bessent in August talked on wanting to keep the spread between mortgage rates and treasuries flat or even bring it down. These are some of the lowest spreads since Mar 2022.

- The spread to 10Y swap rates meanwhile has averaged 280bp for three weeks now, a tightening from the 300 +/-5bp range seen for some time since reciprocal tariff announcements in April. It’s a little below the 285bp averaged in Q1.

EQUITY OPTIONS: EU Bank more Rolling Put

Oct-08 11:10

- SX7E (17th Oct vs 19th Dec) 220p, bought the Dec for 5.8 in 4k.

Earlier saw a Nov vs Dec 220p.

EURJPY TECHS: Impulsive Bull Wave Extends

Oct-08 11:09

- RES 4: 180.00 Psychological round number

- RES 3: 179.50 Top of a bull channel drawn from the Feb 28 low

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 178.00 Round number resistance

- PRICE: 177.85 @ 11:51 BST Oct 8

- SUP 1: 175.13 Hgh Sep 29

- SUP 2: 174.03 20-day EMA

- SUP 3: 173.24 High Oct 3 and a gap low on the daily chart

- SUP 4: 172.27 Low Oct 2 and a key medium-term support

The trend set-up in EURJPY remains bullish and fresh cycle highs this week strengthens the bull condition. The cross has cleared resistance at 175.13, the Sep 29 high, to confirm a resumption of the primary uptrend and hit all-time highs in the process. The move higher this week also marks an acceleration of the uptrend. Sights are on the 178.00 handle next. Key short-term support has been defined at 172.27, the Oct 2 low.

{kind=link}

Trending Top

Mar-27 20:13