US DATA: December PCE: Core Inflation Looks In Line, But Consumption Upgrade Due

Jan-31 13:09

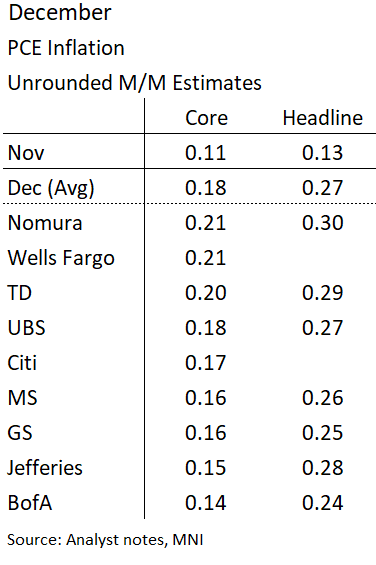

The median analyst expectation for monthly core PCE (Friday 0830ET) following the CPI/PPI/Import Price releases was 0.18% M/M (central range of 0.14-0.21%) - see table below.

- Thursday's Q4 GDP release suggests that those expectations were well-founded: at 2.502% Q/Q annualized, the implied core PCE rate for December is 0.172% M/M (the analyst median is basically split between 0.17% and 0.18%). Headline is seen at 0.27% (0.13% prior). Of course that doesn't account for possible revisions to the prior months, but as it stands there were no major revelations from the quarterly data.

- The GDP readings put the Q4 Y/Y figure at 2.8%, exactly in line with the FOMC's December projections, so this should not affect policymakers' perceptions of price pressures at end-year.

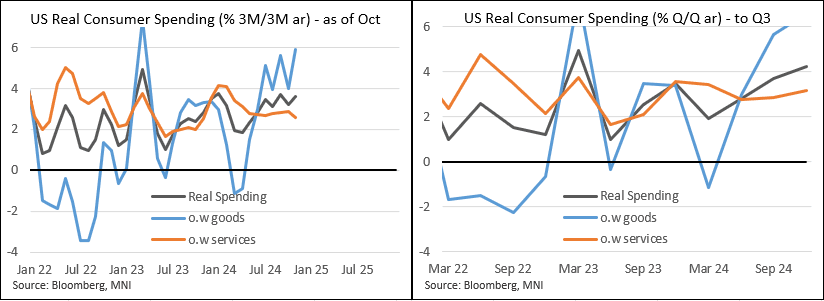

- As for monthly consumption, surveys coming into this week saw December real personal spending at 0.3% M/M (same as December).

- But that figure (which was consistent with the 3.2% Q/Q quarterly consensus for consumption) looks to be higher in reality, given the 4.2% Q/Q quarterly print that we now have in hand.

- It also suggests there will be upside revisions to the softer real consumption figures we saw in Oct (0.1% M/M) and Nov (0.3%). The 3-month annualized figure in November was a "mere" 3.6%, so absent revisions to Oct/Nov, the consumer looks to have ended Q4 with roaring activity, perhaps on the order of 0.6%.

- We'll also look for the breakdown, given that the momentum for services (two-thirds of PCE consumption) appeared to be fading in the monthly prints, but the GDP report showed a different story. In November, services consumption printed a 15-month low growth of 0.07% - suggesting some of the weakest momentum in a year. But the GDP figures showed a 3-quarter high for real services consumption growth (3.1% Q/Q ann., 2.8% prior), pointing to a strong December and/or upward revisions to prior.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Tsy Curves Look To Finish 2024 at June'22 Highs

Dec-31 19:18

- Treasuries look to finish the last trading session of 2024 lower after reversing Tuesday morning support. Markets closed Wednesday for New Years day, resume full trade Thursday.

- The Mar'25 10Y contract trades 108-25.5 (-5.5) late in the day, 10Y yield near session high of 4.5871%. Curves bounced off flatter levels, 2s10s climbing to 34.344 -- the highest level since June 2022.

- Short end support, in turn, helped projected rate cuts into early 2025 gain momentum vs. late Monday levels (*) as follows: Jan'25 steady at -2.8bp, Mar'25 -14.6bp (-13.6bp), May'25 -20.6bp (-19.5bp), Jun'25 -29.8bp (-28.8bp).

- No substantive reaction to this morning's housing and regional Dallas Fed services activity data. Looking ahead to Thursday data (prior, est): Initial Jobless (219k, 221k) and Continuing Claims (1.910M, 1.890M) at 0830ET; S&P Global US Manufacturing PMI (48.3, 48.3) at 0945ET; Construction Spending MoM (0.4%, 0.3%) at 1000ET.

- Treasury supply: $85B 4- & $80B 8W bill auctions at 1130ET, $64B 17W bill auction at 1300ET.

COMMODITIES: WTI Futures, Gold Holding Higher

Dec-31 18:47

WTI futures are trading higher today as the contract extends recent gains. A stronger reversal to the upside would refocus attention on key short-term resistance at $76.41, the Oct 8 high. Initial firm resistance is unchanged at $71.97. A bear threat in Gold remains present. The yellow metal traded sharply lower on Dec 18 and the move undermines a recent bull theme. A resumption of weakness would open key support at $2536.9, the Nov 14 low.

- WTI Crude up $0.9 or +1.27% at $71.88

- Natural Gas down $0.32 or -8.13% at $3.618

- Gold spot up $19.24 or +0.74% at $2625.86

- Copper down $6.95 or -1.7% at $402.3

- Silver down $0.1 or -0.34% at $28.8383

- Platinum up $3.96 or +0.44% at $908.02

US STOCKS: Late Equity Roundup: Tech & Interactive Media Sectors Underperforming

Dec-31 18:36

- Stocks are trading near session lows after reversing early session gains. Though off this year's record highs (SPX Eminis 6178.75, DJIA 45,073.63, Nasdaq 20,204.58) major averages will finish the year with double digit gains: SPX Eminis +19.5%, DJIA +13.1%, while the Nasdaq gained 29.9%!

- Currently, the DJIA trades down 92.19 points (-0.22%) at 42474.46, S&P E-Minis down 28 points (-0.47%) at 5929.75, Nasdaq down 147 points (-0.8%) at 19337.13.

- Information Technology and Communication Services shares underperformed continued to underperform late Tuesday, shares of software and semiconductor makers weighing on the tech sector: Nvidia -1.61%, Advanced Micro Devices -1.36%, Crowdstrike Holdings -1.28%.

- Interactive media and entertainment shares weighed on the Communication Services sector: Alphabet -0.9%, Live Nation -0.76%, Netflix -0.60%, Meta -0.41%.

- On the positive side, Energy and Materials sectors outperformed in the second half, oil & gas stocks buoyed the Energy sector as crude prices continued to rise (WTI +1.0 at 71.99): APA Corp +3.59%, Marathon Petroleum +2.46%, Occidental Petroleum +2.15%.

- Meanwhile, shares of chemical & fertilizer makers supported the Materials sector: Mosaic +2.44%, Celanese +1.42%, Dow +1.37%.

- Looking ahead, the next round of quarterly earnings kicks off mid-January with Blackrock, Bank of NY Melon, Wells Fargo, JP Morgan, Goldman Sachs, Citigroup, US Bancorp, M&T Bank and PNC all reporting between January 13-16.

Trending Top

May-01 21:26