OIL: Dangote Crude Throughput Lagging Imports: Kpler

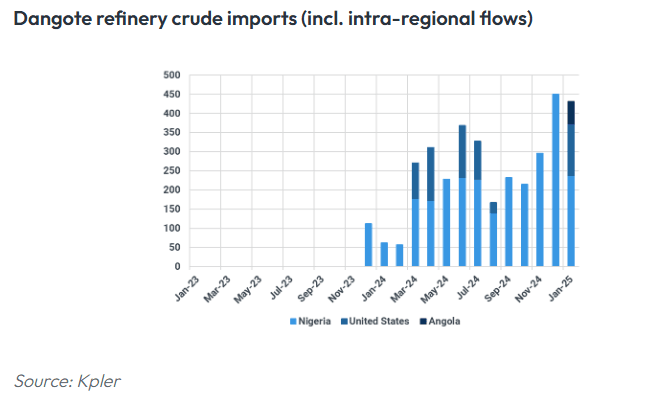

While crude imports into Nigeria’s 650k b/d Dangote refinery surged in Q4 to 450k b/d in Dec, refined product exports in Q4 of just 180k b/d suggest throughput is lagging cargo arrival levels, Kpler said.

- A WTI cargo was discharged at the refinery on Jan. 5, the first US crude delivery in four months, while a Suezmax carrying Angolan Pazflor arrived on Jan. 11, the first-ever Angolan delivery and the first time a medium sweet grade.

- The shift in crude procurement suggests that Dangote’s RFCC and other secondary units are ramping up further.

- Dangote’s gasoline production is likely to increase further ahead, with exports at just 60k b/d in Q4.

- The refinery's gasoline output caters primarily to domestic markets but could become a major supplier cross Western, Central and Southern Africa.

- Europe-Nigeria gasoline flows fell to a four-year low of 70k b/d in December as the Dangote refinery ramped-up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: US 10yr Yield targets the next resistance

- With Tnotes testing another session low, focus turns to the 4.6357% level in Yield, this is around 108.09 vs 108.10 earlier.

- Much Further out would see 4.7351%, the 2024 high, and highest level since November 2023.

- This level would equate to ~107.19 Today.

- There's no Impact in the Yen as of Yet.

(Chart source: MNI/Bloomberg):

STIR: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (+0.01), volume: $2.337T

- Broad General Collateral Rate (BGCR): 4.29% (+0.01), volume: $846B

- Tri-Party General Collateral Rate (TGCR): 4.29% (+0.01), volume: $815B

- (rate, volume levels reflect prior session)

US TSYS: Early SOFR/Treasury Option Roundup

Option desks report modest SOFR & Treasury option volume overnight, better 10Y put interest followed by Jan 10Y call condors more recently. Underlying futures continue to extend lows, 10Y yield revisiting late May levels at 4.6068% this morning. Curves mildly steeper with short end rates outperforming (2s10s now at 25.174 vs. 23.991 low), while projected rate cuts into early 2025 look steady to slightly lower vs. late Monday (*) as follows: Jan'25 steady at -2.1bp, Mar'25 steady at -11.7bp, May'25 -16.7bp (-16.0bp), Jun'25 -23.1bp (-23.4bp).

- SOFR Options:

- 3,100 SFRF5 95.56/95.62/95.68 put flys

- Treasury Options:

- 6,000 TYF5 108.5/108.75/109/109.25 call condors

- Block, 6,000 TYF5 108.5 puts, 13 ref 108-15, 8,200 total, 11 last

- 26,000 TYG5 107.5/108.5 put spds, 24 ref 108-16.5

- 1,700 USF5 112 puts, 2 ref 113-18