OIL: Crude Range Trading Into Thanksgiving Holiday, Bearish Theme Persists

Crude has traded in a $2 range this week falling on news of progress towards a Ukraine peace deal but then tending to rise the following day as the fact sensitive issues, such as territory and security, remain unresolved. After rising on Wednesday, despite news of a US crude stock build, prices are slightly higher on the week.

- WTI is up 1.0% to $58.55/bbl, close to the intraday high at $58.72 which followed a low of $57.66. The benchmark reached a high of $59.06/bbl on Monday and then a low of $57.10 Tuesday and is up 0.9% this week. Initial resistance is at $61.84 with the bear trigger at $55.99.

- Brent rose 0.9% to $63.06 off the day’s peak at $63.20. It fell to $62.11 earlier. It is up 0.7% this week. A bearish theme persists with the bear trigger at $59.97. Initial resistance is at $65.95, 24 October high.

- The EIA reported a crude inventory build of 2.77mn barrels last week bringing the increase in November to 10.96mn. Distillate rose 1.1mn and gasoline 2.51mn but refining utilisation was up 0.3pp to 92.3%, which is almost 2pp above the same time last year.

- Talks on a Ukraine peace are to continue after the Thanksgiving holiday with US envoy Witkoff to go to Russia next week. There were reports that Driscoll would go to Ukraine.

- Goldman Sachs estimates that peace and the subsequent easing of sanctions on Russia would reduce its 2026 Brent forecast of $56/bbl by $5, according to Bloomberg. As Russia has not had trouble finding buyers for its discounted crude, it is unclear the impact fewer sanctions would have on global oil supply.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Macro SinceLast FOMC - Labor: Various Metrics Point To Slow Build In Slack

We may not have received the nonfarm payrolls report for September but the labor market is one of the easier areas of the economy to track in the absence of official data.

- When compiling our own “shadow” employment report, we assessed that alternative private sector indicators of jobs growth paint a mixed picture on the extent of the latest additional softening beyond that seen in latest BLS payrolls data to August.

- The median primary dealer analyst eyed a 60k increase in nonfarm payrolls growth in September although private sector employment growth in the ADP employment was then much weaker than expected at -32k.

- Two indicators that have recently been un-paywalled in response to the government shutdown offer alternative tracking estimates for jobs growth. Revelio Labs estimated jobs growth of 60k,implying no further softening from recent trends in the latest BLS payrolls data published to August (3mth average 29k, 6mth 64k or private sector averages of 29k and 67k) whilst the Carlyle Group’s estimate sat between Revelio and ADP with a projected 17k increase.

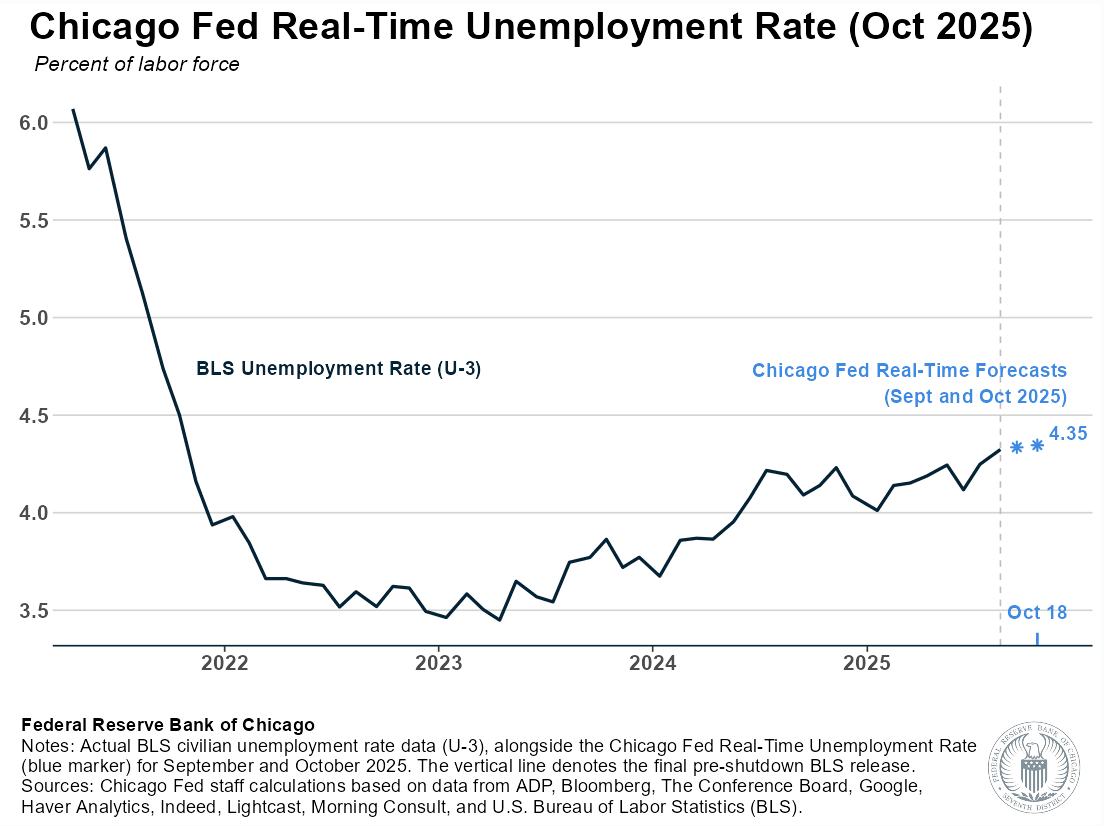

- With ratios keenly watched by FOMC members against a backdrop of large changes in labor supply, various unemployment rate metrics point to further increases. That includes to (marginally) new recent highs in the Chicago Fed’s unemployment rate nowcast at 4.35% in October after an estimated 4.34% in September and 4.32% in official August data.

- Recall that the September SEP showed the median FOMC participant expecting further increases in the months ahead to 4.5% in Q4, before slowly easing to 4.4% in 4Q26 and 4.3% in 4Q27.

- State-level jobless claims data look contained though, with the labor market still best characterized as in a low fire, low hire state.

- For a comprehensive summary of these labor metrics, see our full report found here, noting that weekly jobless claims data and the Chicago Fed nowcast have been updated since then but haven’t materially altered the picture.

ASIA: Coming Up In Asia Pac Markets On Tuesday

| 2145BST | 0545HKT | 0845AEDT | New Zealand Sep Filled Jobs |

| 2300BST | 0700HKT | 1000AEDT | South Korea Q3 GDP |

| 0000BST | 0800HKT | 1100AEDT | Australia 2037 Bond Sale |

Source: Bloomberg Finance L.P./MNI

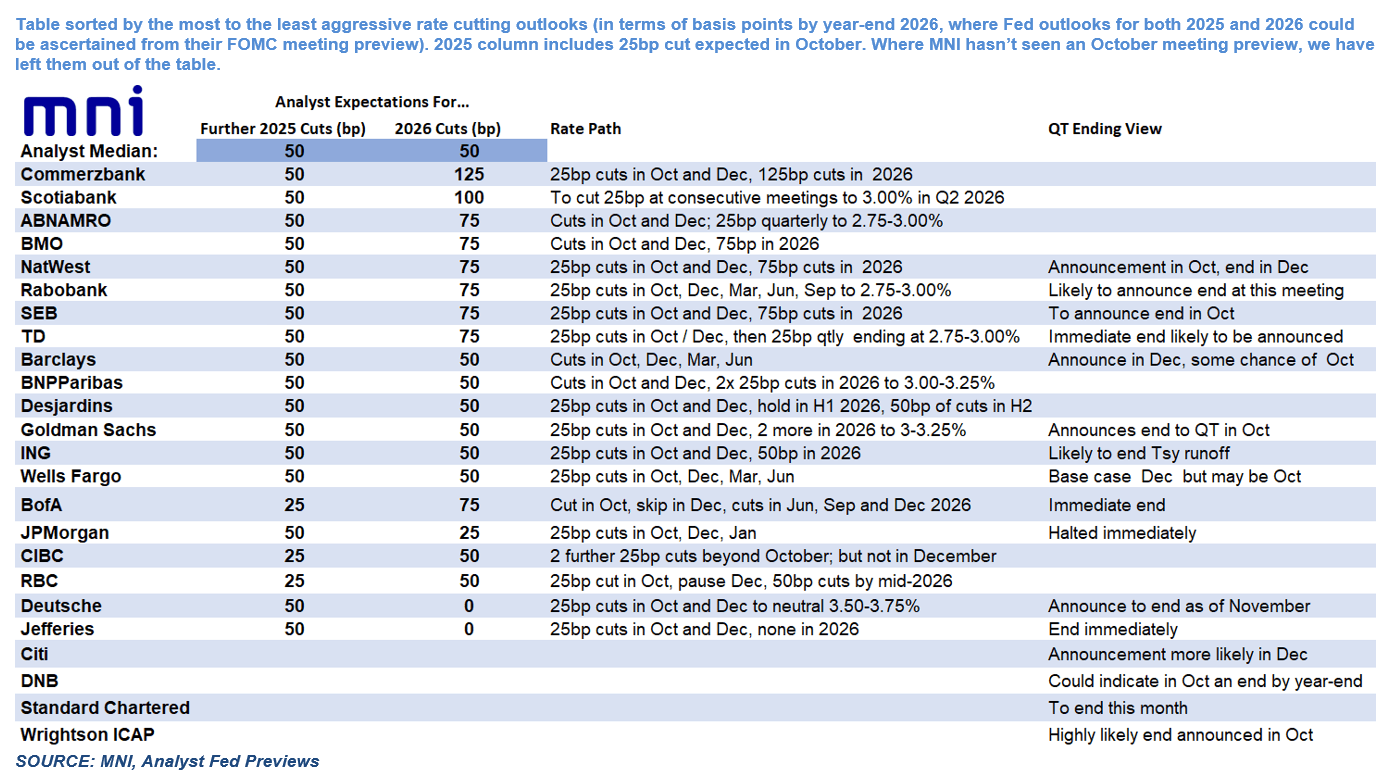

FED: MNI Fed Preview-October 2025: Analyst Outlook

This update of our October 24 Fed preview includes analyst expectations - starting page 32 - Download Full Report Here

The FOMC is unanimously expected to cut the Fed funds rate by 25bp at the October meeting, per 31 previews seen by MNI.

- Future action: Almost all analysts expect a follow-up cut in December, though some expect a “skip” at the meeting before resuming easing in 2026 (BofA, CIBC, RBC).

- Analysts’ views of total cuts from now through end-2026 range from 50bp to 175bp, with two analysts seeing no 2026 cuts (Deutsche, Jefferies). The median expectation is for 50bp of further cuts in 2025 and 50bp in 2026.

- Statement: There aren’t many expectations for meaningful changes to the October statement vs September’s, with the characterization of growth seen upgraded somewhat, but few to no changes to the description of inflation / labor market developments. The Statement may add language to acknowledge the limited flow of “official” data, but suggest that trends evident going into the prior meeting remain intact.

- No analyst expects the characterization of the balance of risks to be changed. Likewise, there are no core views that forward rate guidance will be changed - though JPMorgan cites risks the Statement could mention "in considering the extent and timing of additional adjustments" to hint an imminent end of the mini-easing cycle.

- QT: An immediate end to balance sheet runoff is now the consensus expectation for the October meeting. Some analysts expect a December announcement, but acknowledge risks it could happen this week.

- Dissents: Gov Miran is almost universally expected to dissent again in favor of a 50bp cut. Many analysts see potential for a hawkish dissent in favor of a hold, with KC Fed’s Schmid the most likely candidate.