US DATA: CPI Imputation Shares At Least Improved In November

Dec-18 17:29

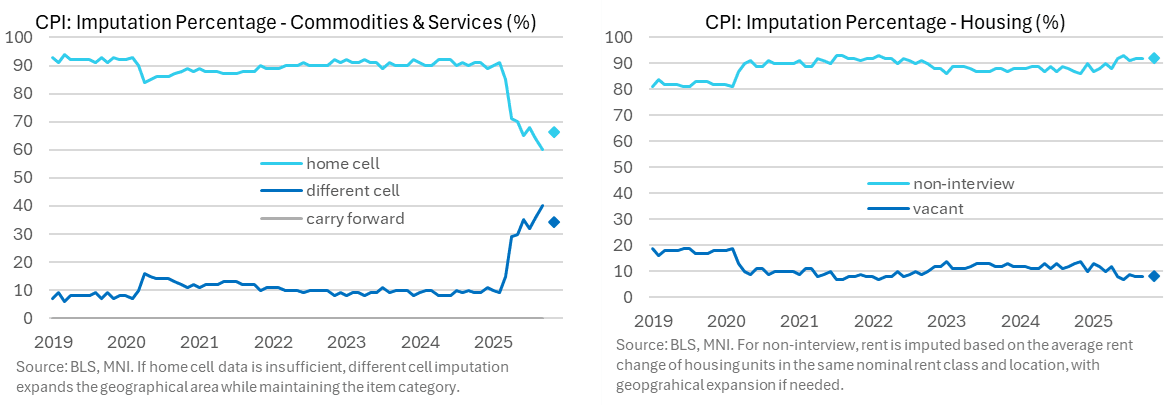

- It doesn’t help shine any light on the wide range of questions around October data collection but the imputation percentages for the commodities & services survey at least improved in November after a latest deterioration in September.

- Specifically, the different cell imputation share fell to 34% in Nov after a latest record high of 40% in September (data back to Jan 2019), 36% in Aug and 32% in Jul.

- For context, this share started the year at 10% before climbing following budget and staff cuts. It also peaked at 15% in the pandemic when in-person surveys weren’t possible.

- Different cell imputation is used when the BLS needs to expand the geographical area for a specific category.

- With 66% using home cell imputation, 0% used carry forward as opposed to what was presumably a huge spike in October.

- The housing survey imputation shares were similar to prior months however, with a non-interview share of 92% in both Nov and Sep.

- For these non-interview cases: “rent is imputed by the average change in rent observed for housing units within the same nominal rent class (low, medium, or high rent) within the same location. If this source pool is insufficient, the pool is expanded across geography similar to the method used in the C&S survey.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Dhingra Slides Maintain Clearly Dovish Stance

Nov-18 17:20

There don’t look to be any surprises in BoE Dhingra's presentation, being the most dovish MPC member. Some highlights from her slides:

- Consumption growth has been consistently weaker than forecast

- The expected falling back in the saving ratio has failed to materialise

- Microdata points to disposable incomes being just as weak as consumption

- Spending microdata suggests household costs are less optimistic regarding a real wage recovery

- Only interest income has grown consistently during the “consumption puzzle period”

- The financial counterpart of savings shows a paying down of debts rather than an accumulation of liquid assets for future consumption

- And deposits have been stable except for the top quintile of households

OPTIONS: Larger FX Option Pipeline

Nov-18 17:20

- EUR/USD: Nov20 $1.1500(E2.0bln), $1.1630(E1.2bln), $1.1675-80(E1.5bln); Nov21 $1.1500(E1.4bln), $1.1675-80(E1.2bln)

- USD/JPY: Nov20 Y150.00($1.3bln), Y155.00($1.4bln)

- AUD/USD: Nov20 $0.6550(A$2.3bln)

- USD/CAD: Nov21 C$1.3950-70($1.3bln)

- USD/CNY: Nov20 Cny7.1080-89($2.0bln)

FED: US TSY TO SELL $95.000 BLN 8W BILL NOV 20, SETTLE NOV 25

Nov-18 17:05

- US TSY TO SELL $95.000 BLN 8W BILL NOV 20, SETTLE NOV 25