US TSYS: Could a Stronger GDP See Yields Higher Again?

- US treasury futures trended sideways today, after last night's dramatic shift and will look ahead to tonight's trading session to see if there is further follow on. The 10-Yr bond future was around 112-18+ by late afternoon in the trading day in Asia, up marginally from the US close of 112-25

Bonds rallied back with yields down 1-2bps in what appears to be profit taking. In what was a relatively outsized move overnight in yields, it was unsurprising to see a modest bounce back today.

- The US 2-Yr is -1.8bps lower at 3.582%

- The US 5-Yr is down -1.9bps at 3.694%

- The US 10-Yr has recovered a little, down -1.9bps at 4.06%

- The US 30-Yr is at 4.614% down -1.2bps on the day.

It remains to be seen whether the bond market will continue to sell of in US time overnight. The auction schedule is predominantly bills and unlikely to drive the direction for bonds.

Most likely catalyst for tonight is data with initial jobless claims and GDP QoQ, which is expected to moderate to 3.0% from 3.8%. The likelihood is that positioning in treasuries is more balanced after last night's move. Should however GDP not moderate as much as forecasts, it could push on the market further sending yields higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

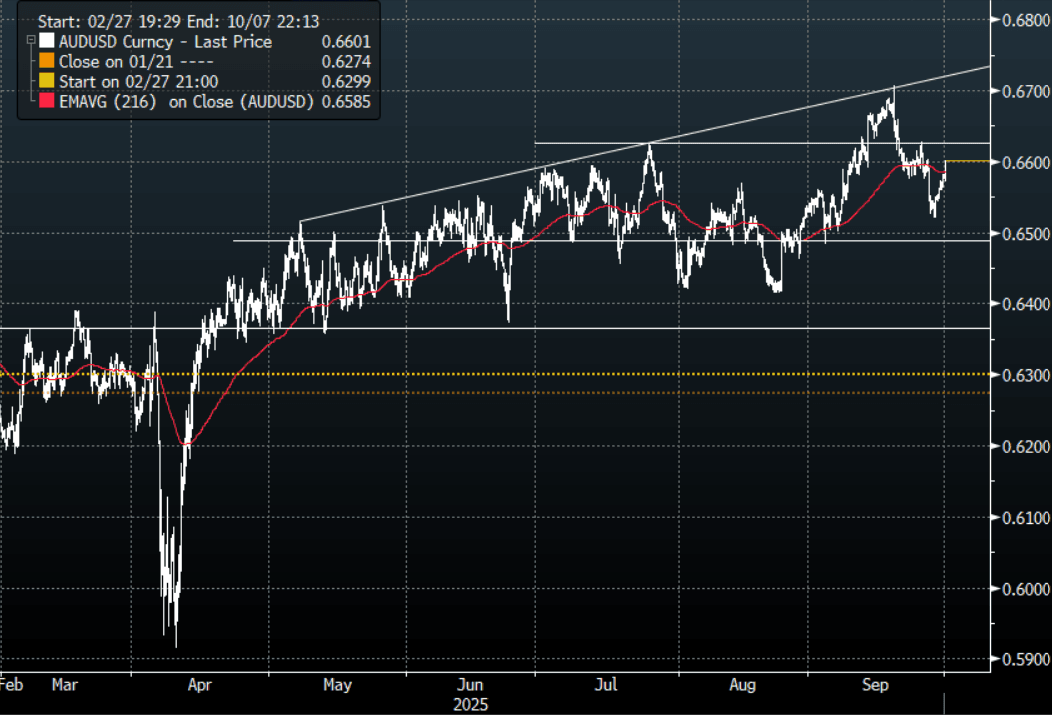

AUD: Asia Wrap - AUD/USD Drifts Higher Then Pops To Test 0.6600 On RBA

The AUD/USD has had a range of 0.6571 - 0.6603 in the Asia- Pac session, it is currently trading around 0.6600, +0.35%. The USD can’t find any friends and a potential shutdown has brought out all the bears again. The AUD drifted higher in sympathy, the RBA left rates unchanged and gave the pair an extra bump up to test 0.6600. I suspect some resistance back towards the 0.6600/0.6625 area initially. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print could take on larger significance.

- "RBA SAYS HOUSING MARKET STRENGTHENING, BOARD JUDGED APPROPRIATE TO REMAIN CAUTIOUS. SAYS LABOR MARKET CONDITIONS REMAIN A LITTLE TIGHT. RECENT DATA SUGGEST 3Q INFLATION MAY BE HIGHER THAN SEEN, SAYS DECLINE IN UNDERLYING INFLATION HAS SLOWED." - BBG

- "AUSTRALIA AUG. PRIVATE CREDIT RISES 7.2% Y/Y, AUSTRALIA AUG. PRIVATE CREDIT RISES 0.6% M/M; EST. +0.6%" - BBG

- "AUSTRALIA AUG. BUILDING APPROVALS FALL 6.0% M/M; EST. 2.6%, AUSTRALIA AUG. PRIVATE-SECTOR HOME APPROVALS FALL 2.6% M/M" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6417(AUD597m), 0.6600(AUD820m), 0.6800(AUD525m). Upcoming Close Strikes : 0.6600(AUD1.5b Oct 3), 0.6600(AUD1.7b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.70 - 98.08, Asia is trading around 98.00. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

Fig 1: AUD/USD spot 2HChart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Continues Trending Lower, Focus On Supply Outlook

After falling over 3.5% on Monday, oil has continued falling during Tuesday’s APAC session as the market’s attention returns to excess supply concerns. WTI is down 0.6% to $63.09/bbl after rising to $63.21 and then falling to $62.91. Brent (December) is also 0.6% lower at $66.68/bbl off the intraday trough of $66.52 which followed a high of $66.82. The USD index is flat.

- The focus has returned to supply following flows from Iraqi Kurdistan to Turkey resumed on the weekend after being halted for around two and a half years. Thus, the upcoming 5 October OPEC+ meeting is of particular interest and it is currently expected to increase November production by at least 137kbd in line with October. While the group wants to increase market share, there is little material spare capacity amongst members, except Saudi Arabia.

- An increase in inventories is a sign of excess supply. US industry-based data is released later on Tuesday.

- Later the Fed’s Jefferson, Collins, Goolsbee, Logan, ECB’s Lagarde, Elderson, Machado, Cipollone and BoE’s Mann, Lombardelli and Breeden speak. US July housing data, August JOLTS job openings, September MNI Chicago PMI and Conference Board consumer confidence as well as German August retail sales, unemployment and preliminary German/Italian September CPIs are released.

RBA BOARD ATTENTIVE TO DATA, EVOLVING RISKS

- RBA BOARD ATTENTIVE TO DATA, EVOLVING RISKS