USDCAD TECHS: Corrective Pullback Still In Play

- RES 4: 1.4023 76.4% retracement of the Nov 5 - Dec 26 bear leg

- RES 3: 1.3977 High Dec 4

- RES 2: 1.3950 61.8% retracement of the Nov 5 - Dec 26 bear leg

- RES 1: 1.3855/3929 50-day EMA / High Jan 16

- PRICE: 1.3803 @ 16:09 GMT Jan 22

- SUP 1: 1.3786 Low Jan 21

- SUP 2: 1.3752 Low Jan 6

- SUP 3: 1.3701 Low Jan 2

- SUP 4: 1.3643 Low Dec 26 and the bear trigger

The latest move down in USDCAD appears corrective - for now. However, price has breached support at the 20-day EMA, at 1.3838. The clear break of this EMA highlights a stronger reversal and signals scope for a deeper retracement - towards 1.3752, the Jan 6 low. Key short-term resistance and the bull trigger has been defined at 1.3929, the Jan 16 high. A move through this hurdle is required to reinstate the recent bull theme.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

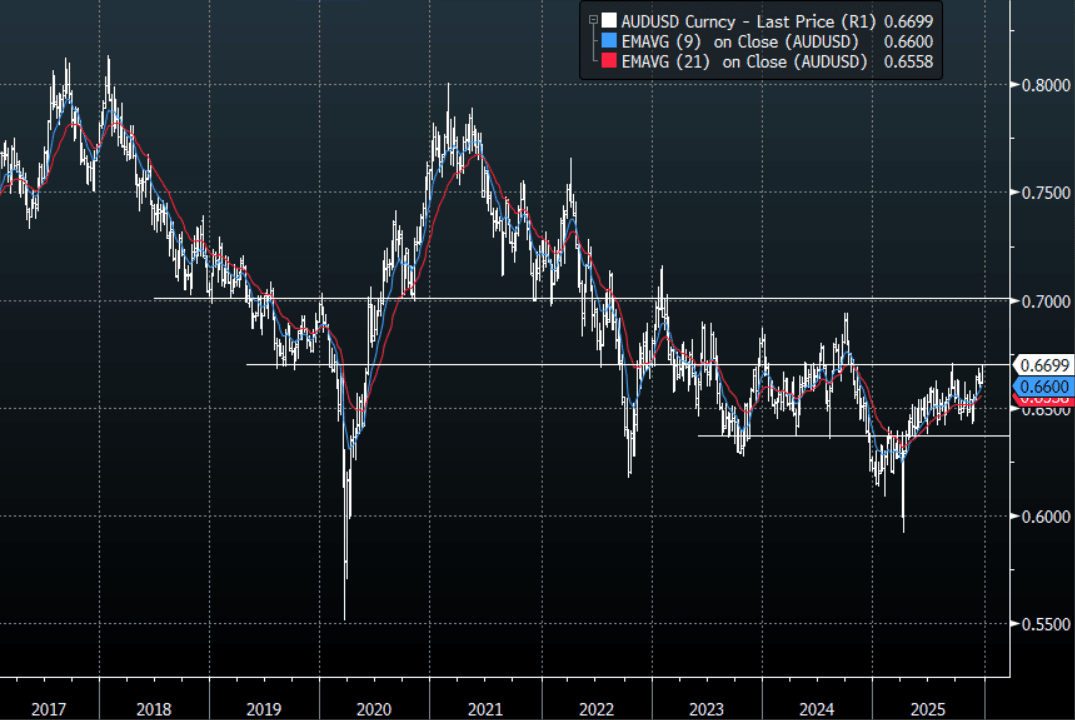

AUD: AUD/USD - Extends Higher To Test Important 0.6700 Area

The AUD/USD had a range overnight of 0.6666-0.6700, Asia is trading around {AUDUSD Curncy}. The AUD extended its move higher rising to challenge the 0.6700 area as risk has built on its recent gains and a strong GDP print added tailwinds to the Santa Rally. The AUD price action remains constructive as the pair looks to build the momentum to try and break above the 0.6700 area. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. In the Asian session, focus will be around the attempt to break back above 0.6700, the AUD does look a little stretched short-term but with risk powering ahead and liquidity not what it would normally be a move higher is possible. I would prefer to fade dips again with the first support on the day 0.6645-0.6665.

- Bloomberg - “The US economy grew at its fastest clip in two years, with a 4.3% annualized advance in the third quarter bolstered by resilient consumer and business spending, as well as calmer trade policies. The report did little to alter bets the Fed won’t be cutting rates any time soon.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6700(360m Dec29) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUDUSD TECHS: Structure Remains Bullish

- RES 4: 0.6759 High Oct 11 ‘24

- RES 3: 0.6723 High Oct 21 ‘24

- RES 2: 0.6707 High Sep 17 and a key resistance

- RES 1: 0.6700 High Dec 23

- PRICE: 0.6687 @ 15:46 GMT Dec 23

- SUP 1: 0.6593 Low Dec 18

- SUP 2: 0.6571 50-day EMA

- SUP 3: 0.6517 Low Nov 27

- SUP 4: 0.6466/21 Low Nov 26 / 21

The trend condition in AUDUSD remains bullish and a strong rally so far this week reinforces current conditions. Support at the 20-day EMA, at 0.6605, has been pierced. The 50-day average is at 0.6571. The area between the two averages represents a key short-term support zone. A continuation higher would expose 0.6707, the Sep 17 high and bull trigger. Clearance of this level would strengthen the bullish condition.

US TSYS: Strong Data Weighs on Rate Cut Pricing, Curves Twist Flatter

- Treasuries look to finish mixed, curves twist flatter (2s10s -1.733 at 63.666) with 2s-10s weaker vs. modest gains in Bonds. Futures gapped lower after stronger than expected economic data while projected rate cut pricing in-turn consolidated with the June '26 now the first FOMC date to price in a 25bp cut.

- Real GDP growth was clearly stronger than most expected in the “initial” Q3 release, with the largest upside coming from personal consumption but also with a larger than expected boost from net exports that was only partly offset by a larger than expected drag from inventories. Real GDP increased a strong 4.3% whilst PDFP was also solid at 3.0%.

- ADP employment saw an average week-on-week increase of 11.5k in the four weeks to Dec 6, a moderation after the upward revised 17.5k (initial 16.25k) in the four weeks to Nov 29.

- Durable goods orders fell more than expected in October, but as is often the case the headline reading was distorted by aircraft orders. Not only did core readings beat expectations, but priors were revised up, making for an overall solid report. In this shutdown-delayed report, headline durables orders fell 2.2% M/M (1.5% fall expected, but prior rev up 0.2pp to 0.7%), but fared better ex-transportation (up 0.2% vs the 0.3% expected, with an upward 0.1pp revision to prior to 0.7%).

- Information Technology and Communication Services sector shares continued to lead advances in the second half, chip makers buoyed after the Trump administration announced a tariff delay on China until 2027.

- Markets close early (1315ET) Wednesday for Christmas eve, re-open for electronic trade Thursday evening for Friday's order of business. Tomorrow's shortened session sees MBA Mortgage Applications (0700ET) and Weekly Jobless Claims (0830ET). Followed by US Treasury supply: US Tsy 4W & 8W bill auctions (1000ET), $44B 7Y Note (91282CPQ8) & 17W bill auctions at 1130ET.