EM ASIA CREDIT: Contemporary Amperex: Lithium mine to restart

(CONAMP, A3/A-/A-)

"*CATL READIES TO RESTART CHINA LITHIUM MINE SOONER THAN EXPECTED" - BBG

Contemporary Amperex (CATL), the world’s largest EV battery supplier, had suspended operations at its Jianxiawo lithium mine in Jiangxi after its mining license expired in August. The markets initial reactions was focused on lack of supply, and impacts on prices, but it was always expected by us to be temporary. Neutral for spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Back Testing All-Time Highs

The ESU5 Friday night range was 6370.25 - 6425.75, Asia is currently trading around 6422. The ESU5 contract was bid for the majority of the N/Y session, closing within a whisker of all-time highs. This morning US futures have opened slightly higher, ESU5 +0.13%, NQU5 +0.07%. Price bounced strongly off its first support around 6200/6250, depending on what your view is I suspect bounces back towards 6400/50 should now find sellers initially as we enter a poor period based on seasonality. A break below 6200 is needed to potentially signal a deeper correction back to the 5900/6000 area. The price action in stocks continues to be bullish though ignoring the headwinds surrounding growth and positioning that point to a possible retracement.

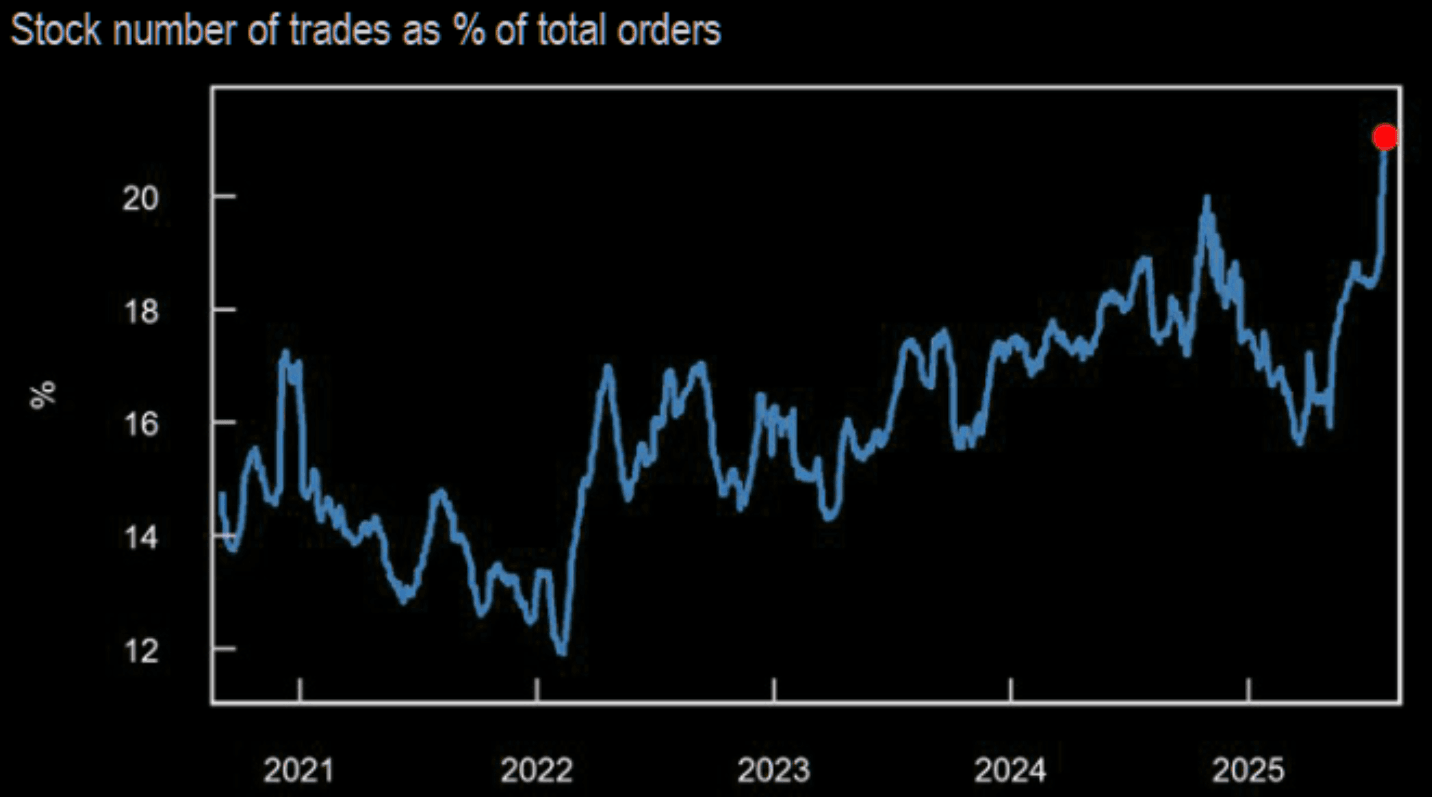

- Lance Roberts on X: “Retail options speculation is literally going to need a bigger chart soon.” See Fig.1 below.

- ISABELNET on X: “At 96.25, the NAAIM Exposure Index reflects active managers' strong bullish stance and significant exposure to the US stock market, signaling robust confidence.”

- Wei Li(CIS BlackRock) on LinkedIn - “Equity bond correlation can’t make up its mind if it is growth or inflation that should matter more. Neither can the Fed, it seems.”

- Seth Golden on X: ”Ahead of ANY rate cuts, excess real liquidity growth has turned positive this quarter for the 1st time in this bull market! When excess liquidity is positive 3-mn forward average annualized returns are 15%+"

- Bloomberg - “ Man versus machine. Computer-driven traders are at their most bullish on stocks since early 2020, while human investors remain bearish amid economic uncertainties. This rare divergence typically doesn’t last long, a Deutsche Bank strategist said.”

Fig 1: Retail Options % Of Total Orders

Source: MNI - Market News/@LanceRoberts

LNG: US-Russia Meeting Drives Prices Lower But EU Heat Increasing Demand

Natural gas was lower on Friday and has started August on a weak note. European prices fell 2.3% to EUR 32.20 to be down 8.7% this month. It reached a high of EUR 33.44 before falling to EUR 32.11. Steady imports and refilling ahead of winter have helped to keep a lid on prices and with Presidents Trump and Putin due to meet in Alaska on Friday the risk premium is being reduced. With Ukraine refusing to cede territory to Russia though, a long-term peace that would allow the easing of sanctions is a very long way off.

- European prices are likely to remain sensitive to changes in supply/demand conditions as inventory building continues. France is expected to increase its gas usage given higher cooling demand and the planned reduction in nuclear power given the current heat wave, which should support gas prices. Lower wind-power generation may also drive higher gas consumption in Germany and the UK.

- US gas fell 2.3% to $2.996 after a low of $2.96 with the key $3.00 level breached again. It is now down 3.5% in August. Supply remains ample with production close to all-time highs and inventories 5.9% above the 5-year average, according to BOK Financial Securities, as the cooling season approaches its end. Thus US prices are likely to remain low for now.

- The weather is expected to be cooler around mid-August for the west and east coasts of the US but temperatures are forecast to remain above average for the eastern two-thirds of the country into the third week of August, according to Vaisala.

- Lower-48 US gas production rose 6.3% y/y, while demand fell 1.2% y/y. Flows to LNG export facilities were down 1.2% w/w. Baker Hughes US gas rig count fell one last week after rising the previous two weeks.

AUSSIE BONDS: Slightly Cheaper Ahead Of Tomorrow's RBA Decision

ACGBs (YM -1.0 & XM -2.0) are slightly weaker after US tsys finished moderately cheaper on Friday.

- The focus of the week will be on Tuesday’s RBA decision, with it widely expected to cut rates 25bp to 3.6%. There are also a number of key data releases too. Q2 wages print on Wednesday and July jobs data Thursday.

- The RBA announcement at 1430 AEST will include how the Monetary Board voted and an update of staff projections. Governor Bullock will hold her usual press conference at 1530 AEST.

- Q2 wages on Wednesday are forecast to moderate slightly rising 0.8% q/q & 3.3% y/y after Q1’s 0.9% q/q & 3.4% y/y. July labour market data print on Thursday and will be watched closely for signs of further deterioration.

- Cash ACGBs are 1-2bps cheaper with the AU-US 10-year yield differential at -2bps.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut tomorrow is given a 97% probability, with a cumulative 61bps of easing priced by year-end.

- Today, the local calendar will be empty.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.