US DATA: Consumer Credit Jumps To End 2025, Overall Impulse Remains Subdued

Consumer credit jumped in December, with total consumer credit owned and securitized up $24.0B ($8.0...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

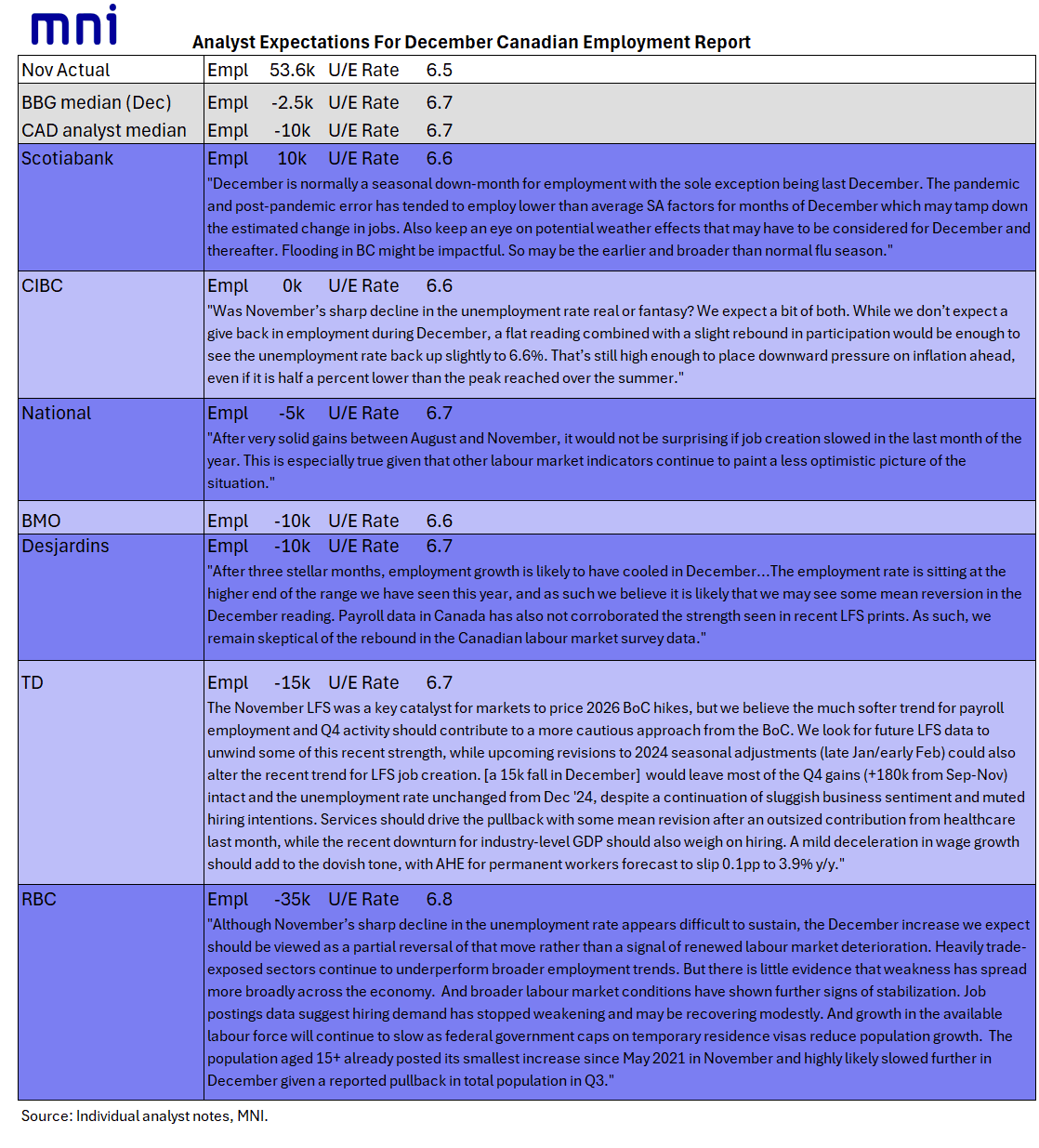

CANADA: Analysts See Mean Reversion In December LFS (2/3)

Canadian institutions see December employment in a range of -35k to +10k (+54k Nov), with unemployment seen rising to between 6.6% and 6.8% (6.5% Nov). See table in image below.

- Various factors identified as worth watching include seasonal adjustments and weather effects (including flooding in British Columbia), but overall the theme is "mean reversion" from a strong November as opposed to any particular macro driver in the pullback.

- Longer-term factors to watch in future reports include upcoming revisions to seasonal factors and demographic factors (including capped immigration).

US STOCKS: Late Equities Roundup: Dow Holds Weaker, Defense Stocks Pressed Late

- Stocks remain mixed Wednesday, the DJIA weaker in late trade after extending to a new record high on the open (49,621.43). Currently, the DJIA trades down 338.36 points (-0.68%) at 49121.09, S&P E-Mini Futures down 5 points (-0.07%) at 6983, Nasdaq up 112.8 points (0.5%) at 23660.15.

- Defense stocks reversed support, some gapping lower after Pres Trump warned defense contractors and the industry as a whole that executives should be prevented from making more than $5M annually, while the sector should be barred from allowing dividends and share buybacks.

- "All United State Defense Contractors, and the Defense Industry as a whole, BEWARE: While we make the best Military Equipment in the World (No other Country is even close!), Defense Contractors are currently issuing massive Dividends to their Shareholders and massive Stock Buybacks, at the expense and detriment of investing in Plants and Equipment. This situation will no longer be allowed or tolerated!," Trump posted on his social media platform.

- While GE and Boeing trades steady after the headlines, others retreated: Raytheon Technologies Corporation (RTX) -1.01%, Lockheed Martin Corporation (LMT) -2.97%, General Dynamics Corporation (GD) -2.45%, Northrop Grumman Corporation (NOC) -3.25%.

- Additional underperformers included Utilities and Materials sector shares in the first half. Weighing on the former: Vistra Corp -8.19%, NRG Energy -6.44%, Constellation Energy -4.71%, PG&E Corp -3.28% and Dominion Energy -2.68%.

- Meanwhile, CF Industries Holdings -2.88%, CRH -4.03%, LyondellBasell Industries -2.79%, Steel Dynamics -2.53% and Dow Inc -2.51% weighed on the Materials sector.

- On the positive side mix of Technology and Health Care sector shares continued to lead advances: Intel Corp +6.82%, Crowdstrike Holdings +5.62%, Palo Alto Networks +4.93%, Incyte Corp +3.77%, Regeneron Pharmaceuticals +3.62%, Eli Lilly & Co +3.13%, Synopsys Inc +3.06% and Bristol-Myers Squibb +3.00%.

- While the IT sector led overall gains, there were some significant declines noted on a handful of semiconductor makers: Skyworks Solutions -10.94%, First Solar -9.89%, Western Digital -7.64%, Seagate Technology -5.78% and Monolithic Power Systems -5.24%.

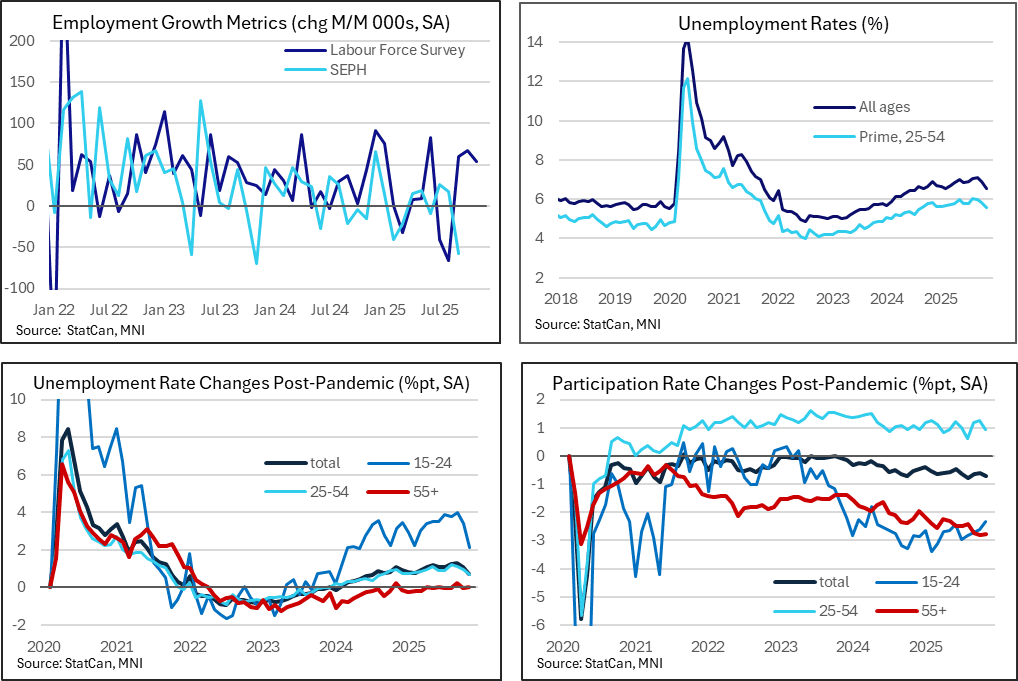

CANADA: December Expected To Partly Reverse Surprising November Job Gains (1/3)

December's Labour Force Survey (Friday Jan 9 at 0830 ET) is expected to show flat-to-negative employment growth, with an uptick in the unemployment rate. While obviously on the soft side, a result in line with consensus would need to be regarded in the context of the large misses vs consensus in previous months, and generally speaking analysts appear to be basing their December expectations on mean reversion after November's strong figures moreso than any other individual factor.

- Canadian analyst median consensus for December is for -10k employment with the unemployment rising to 6.7% from 6.5% on a rounded basis (this is a little weaker than the Bloomberg overall median of -2.5k; also 6.7% unemp).

- The November labour survey was much stronger than expected, including the biggest (ex-pandemic) drop in the unemployment rate in 20 years (to 6.54% from 6.88%), and easily beating the -2.5k employment change expected by consensus with a +53.6k reading.

- This has been part of a pattern of large misses vs consensus in recent months. The October consensus was +10k and the outcome was +67k; September had +5k expected and was +60k; August had expectations of +7.5k and ended up being -65.5k.

- There were some caveats in the November survey, including a part-time driven jobs gain of 63k vs full-time jobs falling 9k (continuing the trends from the previous month). A third consecutive overall beat in employment in December driven by the part-time category would be eyed increasingly skeptically.

- Overall though employment has risen by 181k in the most recent 3 months, after showing contraction through much of the summer. A consensus reading would still keep the 3 month sum at +120k to end the year, which along with a sub-7 unemployment rate suggesting some stabilization in recent months even if the details aren't completely aligned.

- On that front we'll be watching US-Canada trade impact fallout, both in the December report and over the next several months. One metric is the breadth of job gains, with services employment leading gains the last couple of months but goods-producing employment lagging; and indeed wholesale/transportation jobs have been among the weakest on the services side. The BoC's fear had been that weakness in the labour market would spill over from trade-related into non-trade-related sectors, which appeared to start happening in the summer but the bleeding has more recently been staunched.