EU COMMUNICATIONS: COMMUNICATIONS: Ubisoft H1 Falls Short Of Consensus

UBIFP

Results short of expectations though their 2027 line is slightly higher this morning. No further insight around strategic options aside from that they are continuing to explore the sale of assets. Low numbers of consensus estimates.

- Q2 net bookings -37% YoY (~5% short of BBG consensus) as Star Wars and XDefiant continue to underperform expectations though they are working to improve SW ahead of Christmas.

- H1 operating income of EUR -252mn from EUR 43.5mn in H124 (double the consensus loss).

- H1 FCF of EUR -126.3mn from EUR 284.2mn in H124.

- Net debt of EUR 1.1bn from EUR 985mn at FY24 and EUR 880mn at H124

- FY guidance affirmed. Q3 net bookings seen at EUR 380mn vs. consensus of EUR 517mn.

- “On Assassin's Creed Shadows, so there's no risk of it being delayed from mid-February.”

- “And on the strategic options, as we said, we are reviewing the way we can improve execution and deliver recurring, sustainable, robust cash flows in the future. So there are a number of topics that are being reviewed but I won't go further in terms of comments at this stage.”

- “On the question around covenants, so yes, we mentioned that we plan to stay within the covenant boundaries because we expect substantial results in the second half as well as robust cash flow generation. “

- Q: “And then just on debt and leverage, what is the next instrument that is due to be refinanced or has to be paid, and does that sort of create any growing concern issues from yourselves over the next 12 months?” A: “We have a comfortable level of cash equivalent above EUR930 million, so that gives us a good visibility, all the more as with the cash flow generation that is coming ahead of us. The next milestone is at the end of -- very end of calendar year 2025, so December, of close to around EUR280 million.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bid On Wider Risk-Off Flow

Gilts rally from opening lows alongside the broader risk-off price action flagged previously, still no clear headline driver.

- Futures trade as high as 98.80 before easing back to 98.70.

- The bearish technical threat remains present in the contract after the recent pullback.

- Friday’s high (98.94) protects the 20-day EMA (99.40), while initial support comes in at yesterday’s low (98.30).

- Yields 1.0-2.5bp lower across the curve, flattening seen.

- BoE-dated OIS little changed to 2bp more dovish vs. levels flagged ahead of the gilt open.

- 23bp of cuts priced for Nov, 36bp of cuts priced through year-end and 117bp of cuts priced through June ’25.

- SONIA futures recover from lows, last -1.5 to +3.0.

- Final m’fing PMI and the DMO’s auction of GBP2.25bln of the short 20-year 4.75% Oct-43 gilt due today.

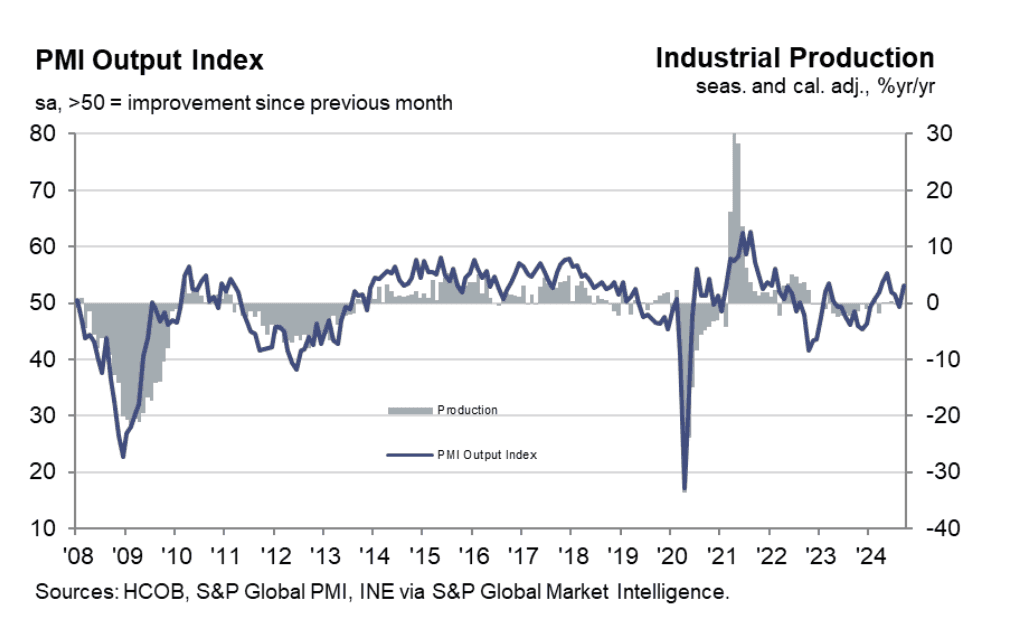

MNI: SPAIN SEP MANUFACTURING PMI 53.0 (FCAST 50.2, AUG 50.5)

- SPAIN SEP MANUFACTURING PMI 53.0 (FCAST 50.2, AUG 50.5)

SPAIN DATA: Sep Manufacturing PMI Much Stronger Than Consensus

The Spanish manufacturing PMI was much stronger than expected at 53.0 (vs 50.2 cons, 50.5 prior). This was the highest reading since May, and cements Spain’s status as the outperformer across the Eurozone this year. Alongside strong output metrics, the PMI notes that competitive forces prompted firms to lower output charges in September.

Key notes from the release:

- “The upturn in the PMI principally reflected solid increases in both output and new orders”…” Manufacturers reported that market demand and positive product campaigns had underpinned growth.”

- “This was further reflected by an increase in new export sales for the seventh successive month. Firms were suitably encouraged by the uplifts in sales and production requirements to bolster their purchasing activity during September”.

- “There was a further increase in input costs amid some reports of higher raw material prices”.

- “The net rise in input costs was however marginal and the weakest since February amid evidence that slow market demand and competition was limiting the pricing power of vendors”.

- “Competitive forces led manufacturers themselves to lower their charges for the first time since April”.