US DATA: Commodity Trajectory Continues To Dictate ISM Manuf Prices

Jul-03 16:48By: Tim Cooper

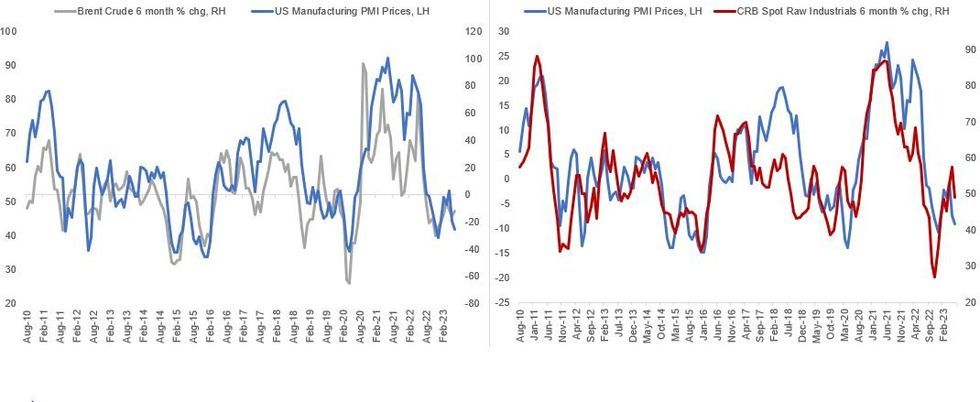

Further to our earlier note on the soft ISM Manufacturing prices paid reading: the 2nd consecutive decline in June following a nascent bounce mirrors the trajectory of changes in commodity prices as it usually does.

- After hitting a peak in mid-2022, oil and broader commodity prices saw a sharp downturn in H2 2022.

- While weakness has persisted, the rate of decline has slowed. After a modest pickup in Apr/May, commodity prices slipped back again, leaving the 6-month change in the CRB index and oil prices negative - in line with the pullback in ISM Manufacturing prices.

- If commodity prices were to stabilize, in other words, so too will ISM Manufacturing prices. In the meantime, the 7th <50 reading in 9 months leaves ISM prices paid at 14 points below the 2010s average of 56, in firmly disinflationary territory.

Source: Bloomberg, CRB, ISM, MNI

Source: Bloomberg, CRB, ISM, MNI