CNH: CNH Outperforms USD Bounce Post Fed, Trump-Xi Meeting Soon

USD/CNH rebounded from sub 7.0900 to just above 7.1000 as the hawkish 25bps Fed cut unfolded. We track near 7.0960 in early Thursday dealings, as markets await the Trump-Xi meeting later in South Korea (11am local time, 2am BST, so in around 1 hour). Focus is on lower tariff rates (related to fentanyl), rare earths export controls, along with China purchases of US soybeans (which resumed this week), while shipping charges, along with other issues that may come up.

- CNH outperformed broader USD gains post the Fed outcome on Wednesday, as US-China trade optimism, the CNY fixing bias (and generally low beta to USD moves) all were in play. EUR/CNH touched 8.2200, but sits back above 8.2400 in early Thursday trade, the pair still eyeing a 8.2000 downside test. CNH/JPY is holding close to 21.50, just off fresh highs since Jan of this year.

- Headlines from the Trump-Xi meet are likely to be positive from a high level standpoint, but the detail will be heavily scrutinized in terms of what exactly has been agreed (particularly in terms of lowered tariff rates) and over what time frame.

- USD/CNH downside focus will rest on mid Sep lows at 7.0851. A break sub this level brings the 7.0500 into focus. On the topside, the 20-day EMA is near 7.1200, while the 50-day is close to 7.1340.

- Note tomorrow, the official PMIs print for Oct.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Bull-Flatten, BOJ SOO Shows Split

In Tokyo morning trade, JGB futures are stronger, +8 compared to settlement levels.

- MNI - Bank of Japan board members were split over whether to raise the policy rate at the September 18-19 meeting, with some calling for more data and others pushing for an increase, the summary of opinions released Tuesday showed. The disclosures gave no clear signal of an October move, with most members aside from Naoki Tamura and Hajime Takata – who dissented and proposed a hike – seeing little urgency.

- MNI - Japan’s industrial output fell 1.2% m/m in August, marking a second straight decline after July’s 1.2% drop, as stronger automobile production was offset by weakness in electrical machinery and information and communications equipment, data from the Ministry of Economy, Trade and Industry showed Tuesday.

- Industrial output is a key indicator for BOJ economists tracking the pace of Japan’s modest recovery as it reflects both external and domestic demand.

- Cash US tsys are slightly cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s bull-flattener.

- Cash JGBs have bull-flattened across benchmarks, with yields flat to 2.2bps richer. The benchmark 10-year yield is 0.6bps lower at 1.637% versus the cycle high of 1.670%.

- Swap rates are little changed.

NEW ZEALAND: Business Activity Remained Soft But Price/Cost Components Up

ANZ business confidence for September was little changed at 49.6 while the activity outlook rose to 43.4 from 38.7. Past own activity rose 4 points to +5 signalling that growth is improving from Q2’s sharp contraction but remains lacklustre. Inflation expectations rose 0.1pp to 2.7% with a net 46% expecting to increase prices over the coming 3 months (+3pp) and an increase in costs. Employment compared to a year ago improved marginally but remained negative at -10.9, in line with other data signalling that the labour market is weak. The RBNZ is expected to ease at both its October and November meetings and monthly data pointing to continued soft growth are in line with this.

USD: BBDXY - Finds Support Back Toward 1200

The BBDXY range overnight was 1200.82 - 1203.57, Asia is currently trading around 1202, -0.01%. The USD finally found some support back towards the 1200 area after being heavily sold on the looming shutdown. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some USD selling to rebalance portfolios. I thought it would be a tough ask to see any big directional moves this week until the market gets a look at the Payroll number. With this data now at risk the ADP could take on a lot more relevance this week and we could potentially have some outsized moves.

- Bloomberg - “Dollar to Take Its Cue From ADP Data as Shutdown Looms. Wednesday’s ADP report will therefore be treated with unusual seriousness. Once dismissed as unreliable and noisy, the series has proven much more accurate than previously believed following recent payrolls revisions, suggesting it could serve as a valuable substitute if payrolls fail to materialize on Friday.”

- Barchart on X: "U.S. Dollar entering its strongest 2-month period of the year historically."

- Robin Brooks on X: “Gold is up 15% since Powell's dovish speech at Jackson Hole, even as the Dollar is flat. This is very unusual and says the rise in gold isn't about Dollar debasement but debasement in fiat currencies broadly. Sign of a global debt crisis…”

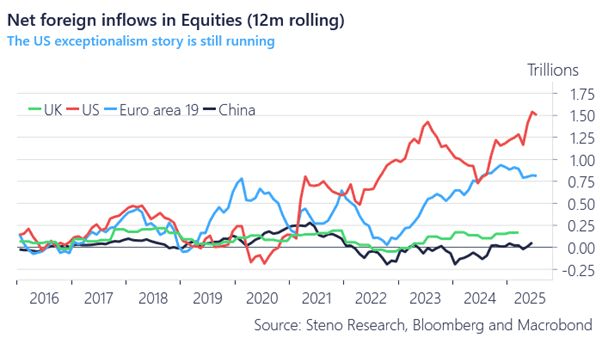

- Andreas Steno Larsen on LinkedIn - “US Exceptionalism is NOT Dead. Listening to the big banks and major financial media outlets this year, one might have assumed that the US investment case was finished. In reality, the flow of funds data tells a very different story—proving that narrative to be entirely unfounded. I cannot recall another year where the economic consensus and prevailing media narrative have been so comprehensively wrongfooted.” See Graph Below.

Fig 1: Net Foreign Inflows In Equities

Source: MNI - Market News/Macrobond/Bloomberg Finance L.P