CNH: CNH Outperforming, CNY Fixing Suggests Low Beta To USD Gains

CNH outperformed broader USD gains on Thursday, with CNH up 0.17%, versus the BBDXY's 0.42% rise. USD/CNH did rebound from lows near 7.1240 on Thursday, last at 7.1380, which is back above the 20-day EMA point, but the 50-day EMA is further north at 7.1450. CNH/JPY continued to march highs, tracking towards 21.50, while EUR/CNH broke under 8.2400, before stabilizing.

- The market remains happy to play CNH outperformance against the majors. USD index gains are not so much reflective of a resilient US backdrop as the Government shutdown rolls on, but uncertainty outside of the US, particularly in Japan and France.

- With yesterday's USD/CNY fixing only marginally above end Sep levels (before China went on holiday), it suggests the yuan will maintain low beta with respect to broader USD shifts. Spot USD/CNY also couldn't sustain early gains above 7.1300 yesterday, which provided fresh impetus for USD/CNH to correct lower.

- For CNH/JPY a break above 21.50, could see late 2024 highs near 21.65 targeted. For EUR/CNH, downside focus may rest with a test of the 8.2000 region, last seen in June of this year.

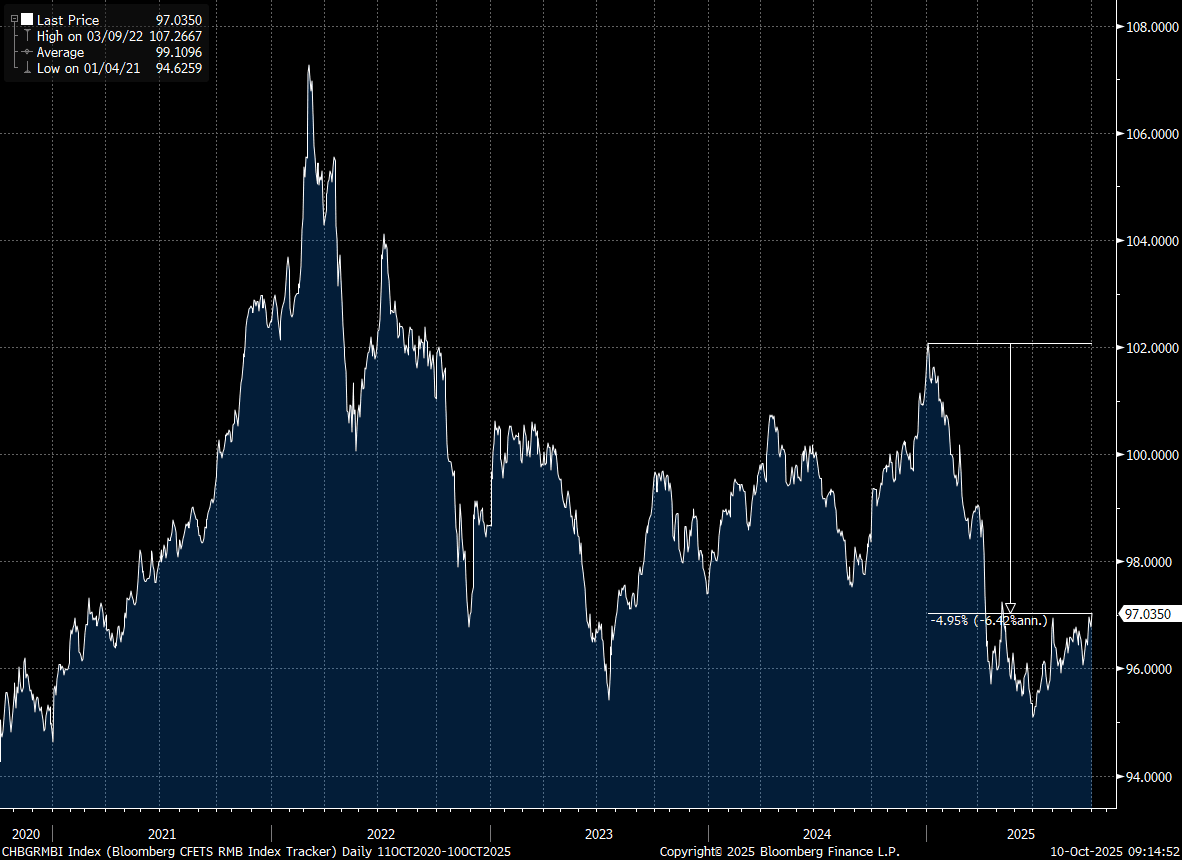

- Even with this recent round of yuan outperformance, the CNY CFETS basket tracker is still down 5% for the year (albeit up from lows), see the chart below.

- The data calendar is empty today, although we may get new loans/aggregate finance figures soon.

- Next week we have trade and inflation figures.

Fig 1: CNY CFETS Basket Tracker Up From Lows But Still Down For 2025

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Yields 2-4bps Firmer, Led By The Back End

NZGB benchmark yields are around 2-4bps firmer across the curve, led by the back end. This follows a firmer US Tsy yield backdrop from Tuesday trade. NFP revisions we weaker than forecast but we do have key inflation prints coming up.

- For the NZGB 2yr yield we are back above 2.96%, around 2bps firmer. This benchmark has struggled to hold moves north of 3.00% since the RBNZ cut rates back in August. The 10yr yield up close to 4bps, last around 4.33.%.

- This leaves the NZ 2/10s curve around 2bps steeper at +137bps.

- The NZ 2yr swap rate is relatively steady so far today, sitting around 2.75%.

- On the data front, we had July net migration at just above +2k, while the annual migration figure picked up to +13k.

- From our policy team, RBNZ Leadership Woes Present Reform Opportunity. Suzanne Snively, a former board member and chair of the independent experts panel that led the 2017-22 RBNZ Act review, said the government may revisit the balance between RBNZ independence and ministerial control, with Finance Minister Nicola Willis likely to reopen debate over.

- Onshore media reported from yesterday: "New Zealand’s main opposition Labour Party is open to having a discussion about the RBNZ’s 1-3% inflation target, the NZ Herald reports, citing finance spokesperson Barbara Edmonds." (via BBG).

- Also note, RBNZ Chief Economist Conway speaks to the Auckland Chamber of Commerce, RBNZ Manager Balance Sheet Policy Craigie will speak on the Liquidity Management Review at 1330.

GOLD: Gold Off New Record High As Waits US Price Data

Gold reached a new record high of $3674.27/oz on Tuesday but then fell and finished the day down 0.3% at $3674.27 but is still up 5.2% this month. It has started today around $3635.5. US August PPI prints Wednesday with CPI Thursday and could impact pricing for Fed easing. OIS has just over 25bp for the 17 September meeting. The stronger US dollar (BBDXY +0.2%) and higher yields pressured gold yesterday.

- Gold approached resistance at $3674.8 but the level wasn’t breached. The metal is in a clear bull cycle with the resumption of the primary uptrend. Initial support is at $3540.2, 5 September low.

- Silver fell 1.2% to $40.874 after reaching a low of $40.787 but is still 2.9% higher in September. It is currently around $40.88. It remains in a bullish trend with initial resistance at $41.671, 8 September high. The 20-day EMA is $39.552.

- Equities were higher with the S&P up 0.3% and Euro stoxx +0.1% and the S&P e-mini is currently +0.2%. Oil prices were stronger with WTI +0.8% to $62.77/bbl. Copper rose 0.4%.

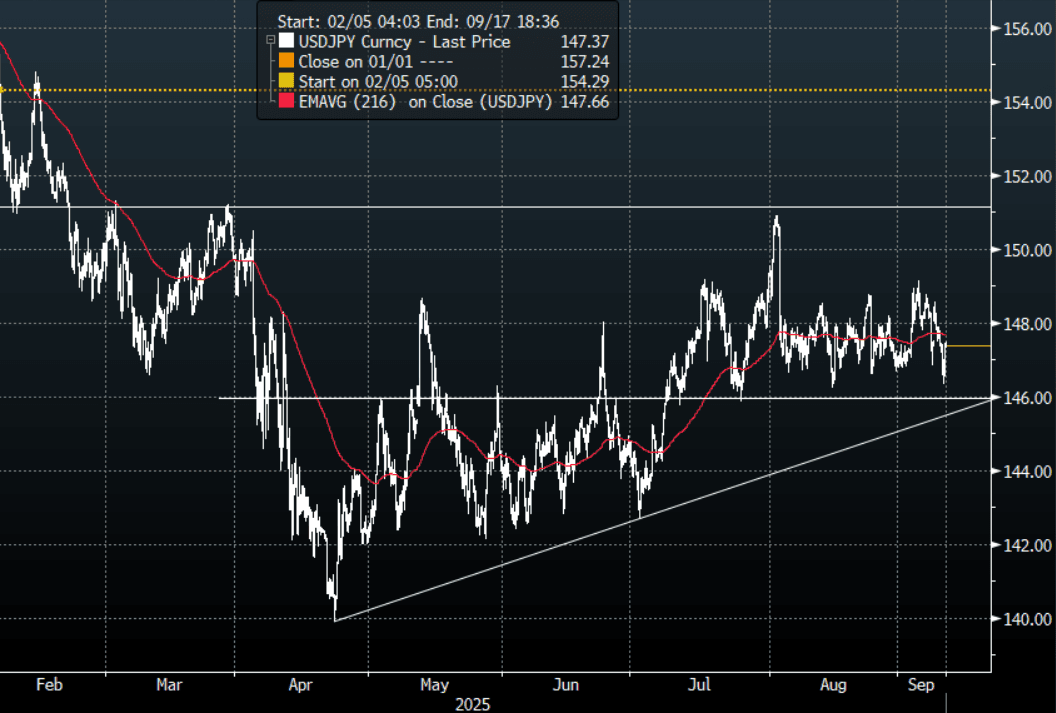

JPY: USD/JPY - Support Towards 146.00 Solid Ahead Of US Inflation Data

The overnight range was 146.31-147.47, Asia is currently trading around 147.35. USD/JPY collapsed lower giving the support towards 146.00 a proper test, but it proved to be solid once again as the market looks towards the US inflation data this week. The price then very quickly retraced back to the middle of its 146-149 range once more. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so they will be hoping the inflation data this week keeps this support intact. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- MNI US: For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior). Core PCE estimates are for 0.31% M/M vs 0.27% prior, with no analysts seeing core PCE printing above core CPI. That could change based on various PPI components that feed into PCE, but as it stands, the M/M core PCE estimate would be the highest since February.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

- “The political uncertainty from the Japanese Prime Minister’s resignation over the weekend will pile greater pressure on the bond market than the currency.” - BBG.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.50($902m).Upcoming Close Strikes : 147.40($1.38b Sept 12), 150.00($1.11b Sept 11) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +78427( Last +76761), leveraged funds though again used the dip to add a decent clip to their newly built short JPY position -66914(Last -52275). One of them is going to be wrong.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P