AUSSIE BONDS: Cheaper With US Tsys, Dec-34 Supply Due

ACGBs (YM -4.0 & XM -4.5) are weaker with attention on a possible US government shutdown. Nevertheless, Q3 ended on a mostly bullish note, as month- and quarter-end rebalancing added to expectations of Fed rate cuts.

- (Bloomberg) -- Australian home prices posted their strongest monthly gain in nearly two years, with an expanded government incentive for first home buyers expected to further intensify buyer demand at a time of already tight supply and declining borrowing costs.

- MNI RBA WATCH: Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Cash ACGBs are 4-6bps cheaper with the AU-US 10-year yield differential at +21bps.

- The bills strip is -4 to -5 beyond the first contract.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

- Today, the local calendar will also feature the S&P Global PMI Manufacturing (F).

- AOFM plans to sell A$1200mn of the 3.50% 21 December 2034 bond.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Back End Yields Supported, Q2 GDP/RBA Speeches In Focus This Week

Early bond future moves are modest, with 3yr futures (YM) last unchanged around 96.59, while 10yr futures (XM) are down 1bps to 95.69. This is mirroring US moves from Friday's session to some degree.

- In the Aussie government bond yield space it is a similar theme, with front end yields down a touch, while back end yields are firmer. The 3yr benchmark was last around 3.39%, while the 10yr was close to 4.28%.

- In the US on Friday, there was a ate bounce in Tsy futures on SF Fed Daly comment on LinkedIn: that "it will soon be time to recalibrate policy". Still, the 10yr yield remained above 4.20%, while front end yields finished down a touch (2yr to 3.62%). Futures have re-opened a touch softer today.

- Locally, Q2 GDP on Wednesday will be the focus of the week with inventories printing today and the net export and public demand contributions on Tuesday. Bloomberg consensus expects that growth was stronger in Q2 at 0.5% q/q after Q1’s lacklustre 0.2% q/q increase.

- RBA Governor Bullock speaks on Wednesday at 1800 AEST about “Technology and the Future of Central Banking at the RBA”. Then on Thursday Deputy Governor Hauser gives an interview to Reuters.

- In terms of broader yield moves, the 3yr is anchored fairly closely to 3.40% over recent sessions, while the 10yr is oscillating around the 4.30% region.

JPY: USD/JPY - Trading Sideways Holding Above Support

USDJPY - Struggles To Hold Gains, Testing 145.00 Support

The Friday night range was 146.77-147.41, Asia is currently trading around 147.10. USD/JPY trades sideways holding just above its recent support. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- (Bloomberg) - “Japan’s Akazawa Canceled US Trip Over Rice, Nikkei Says. Japan’s top trade negotiator Ryosei Akazawa abruptly canceled his trip to Washington on Thursday because there remains a gap between the two sides on the issue of rice, Nikkei reported."

- “Japan’s wage growth is set to strengthen, lifted by summer bonuses and spring wage agreements. A solid reading would reassure the BOJ it can continue tightening, reinforcing the case for another rate hike in October despite trade headwinds from US tariffs.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.35($310m).Upcoming Close Strikes : 146.50($1.39b Sept 3), 145.50($976m Sept 3) - BBG.

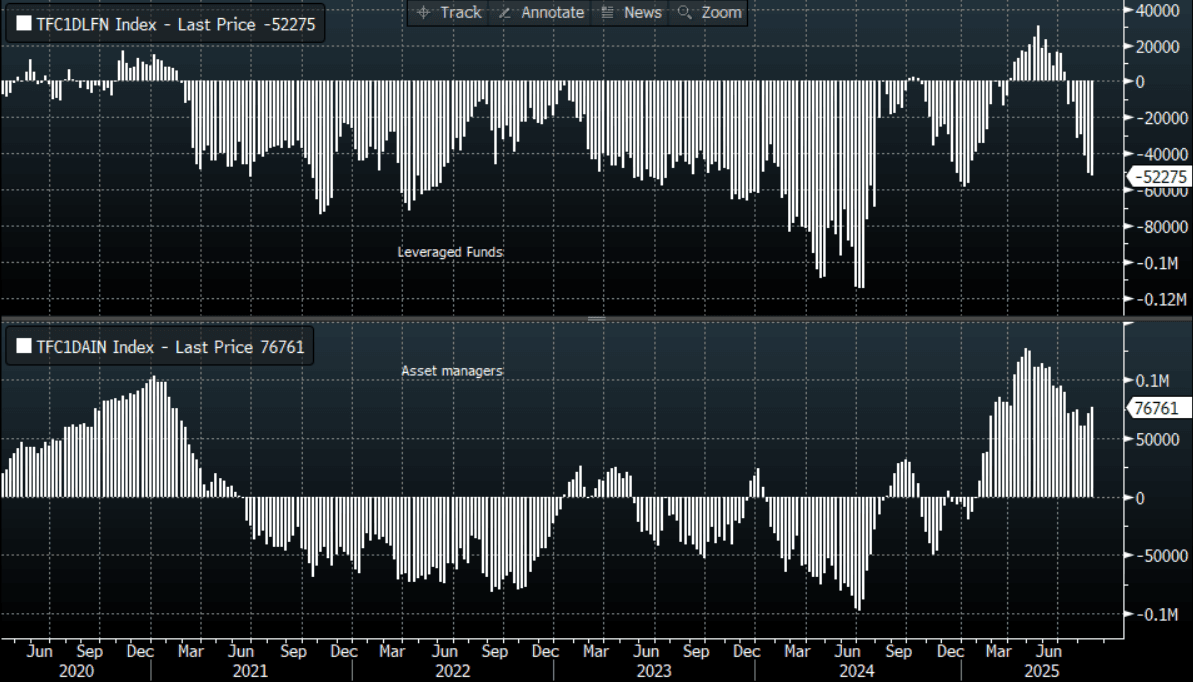

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

- Data/Event : Capital Spending, S&P PMI Mfg

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Government Issuance Today

- Bank of Korea to Sell KRW800bn 91-Day Bonds

- South Korea to Sell KRW2.7tn 2-Year Bonds

- Philippines To Sell PHP 8.5Bln 182D Bills (PH0000060030)

- Philippines To Sell PHP 8.5Bln 91D Bills (PH0000059636)

- Philippines To Sell PHP 8.0Bln 364D Bills (PH0000061012)