CANADA: Carney Talks Up Improving Relations In Meeting w/Chinese Premier

Canadian PM Mark Carney is meeting with Chinese Premier Li Qiang in Beijing as the Canadian leader attempts to improve ties with China amid Ottawa's ongoing trade war with the US. Reuters reports Li saying that "China is ready to work with Canada to increase mutual trust, practical cooperation, and work for more new outcomes." Carney says, "Our teams have worked hard [on] addressing trade irritants and creating platforms for new opportunities."

- On Sino-Canadian relations, Carney says, "We are bringing this relationship back toward where it should be," adding the "Relationship with China had gone through a period of uncertainty and of distance".

- Diplomatic and trade ties have been in the deep freeze for several years following an extradition row and the imposition of tariffs on Chinese EVs by the gov't of former PM Justin Trudeau, which sparked retaliatory action from China hitting Canadian agricultural products.

- Carney finds himself treading a fine line between rebuilding trade ties with China in an effort to diversify exports, while avoiding the worst of the White House's ire that could spark even higher tariff rates on Canadian sales to the US.

- Tomorrow, Carney will hold talks with Chinese President Xi Jinping. The two previously met on the sidelines of the APEC summit in South Korea in November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Of note:

GBPUSD 3.86bn at 1.3500 (a bit far, but a poor US Data could help).

EURUSD 1.61bn at 1.1750.

EURUSD 2.63bn at 1.1750 (thu).

USDJPY 3.14bn at 155.00 (thu).

AUDNZD 1.53bn at 1.1410 (thu).

EURGBP 1.27bn at 0.8800 (fri).

USDJPY 2.02bn at 155.00 (fri).

USDCAD 2.65bn at 1.3800/1.3825 (fri).

AUDUSD 2.67bn at 0.6675/0.6700 (fri).

USDZAR 2.71bn at 16.90/17.10 (fri).

- EURUSD: 1.1700 (424mln), 1.1750 (1.61bn), 1.1800 (729mln).

- GBPUSD: 1.3450 (767mln), 1.3500 (3.86bn).

- USDCAD: 1.3750 (935mln).

- AUDUSD: 0.6640 (489mln).

MNI: UK DEC FLASH MANUF PMI 51.2 (50.3 FCAST, 50.2 NOV)

- MNI: UK DEC FLASH MANUF PMI 51.2 (50.3 FCAST, 50.2 NOV)

- UK DEC FLASH SERV PMI 52.1 (51.6 FCAST, 51.3 NOV)

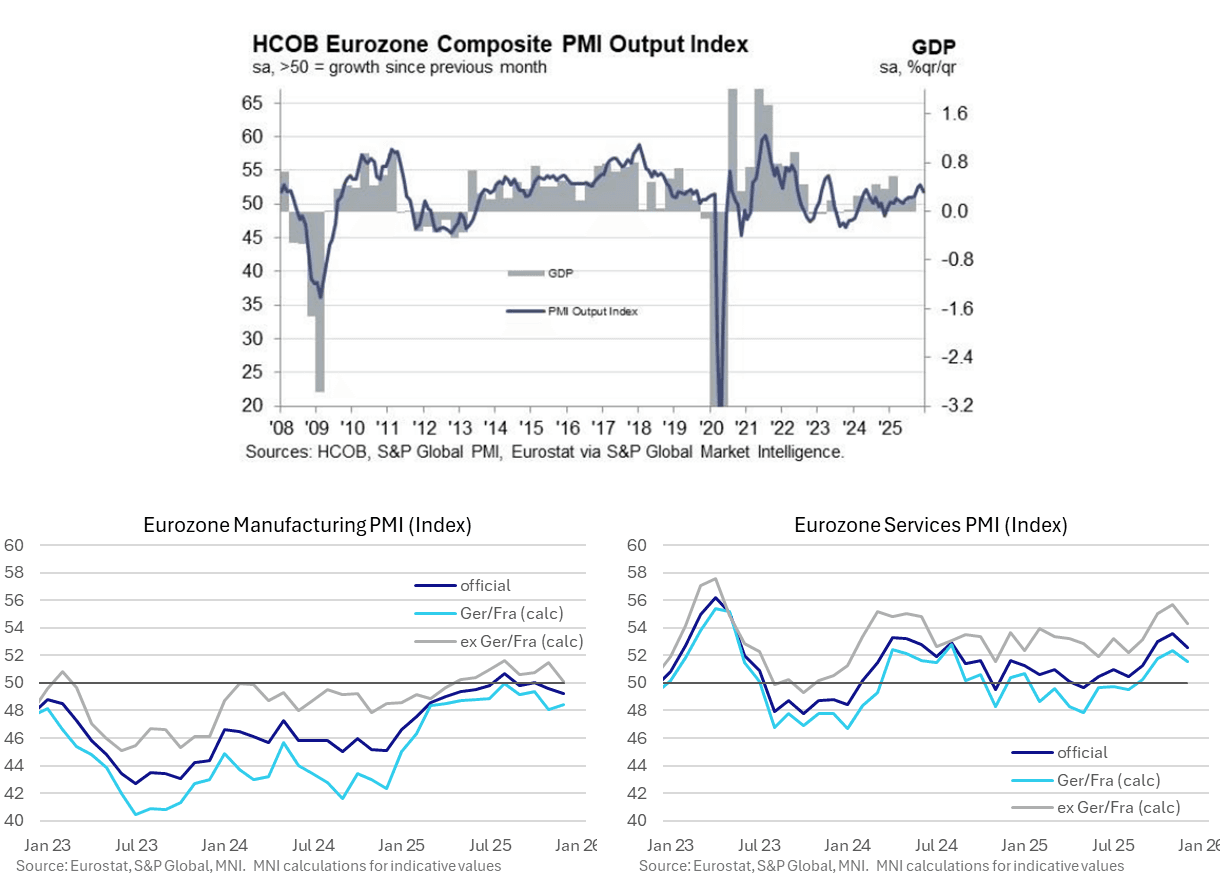

EUROZONE DATA: Dec Flash PMI: Weaker Than Expected, But Q4 Composite 3% Above Q3

The Eurozone-wide composite PMI of 51.9 was weaker-than-expected (vs 52.6 cons, 52.8 prior), but remains comfortably in expansionary territory. The Q4 average composite PMI was 3% above Q3’s average. For comparison, the Q3 average was 1% above Q2.

Manufacturing momentum continues to fade, while services’ moderation still leaves the subcomponent above the 52 handle.

- Services fell to a 3-month low of 52.6 (vs 53.3 cons, 53.6 prior). We estimate the Germany/France services PMI at 51.6 (vs 52.4 in Nov, 51.8 in Oct) and the ex-Germany/France reading at 54.3 (vs 55.7 in Nov).

- Manufacturing fell to an eight-month low of 49.2 (vs 49.9 cons, 49.6 prior). We estimate the Germany/France manufacturing PMI at 48.5 (vs 48.1 prior), and the ex-Germany/France reading at 50.1 (vs 51.5 prior) – an eight-month low.

Key notes from the Eurozone-wide release:

- “Germany saw a slower rise in output during December. The latest increase was modest and the weakest in four months. Meanwhile, output in France came close to stalling, rising only fractionally at the end of 2025. The rest of the Eurozone again posted solid growth of business activity, yet here too the pace of expansion eased from November”

- “As was the case with regards to business activity, new orders increased modestly in December, and at a softer pace than in November. …New export orders continued to fall, and the latest reduction was the sharpest since March. New business from abroad decreased more quickly in manufacturing than in services.”

- “The rise in overall workforce numbers across the euro area was registered in spite of a slight reduction in employment in Germany. Marginal job creation was seen in France and a modest uptick was seen across the rest of the Eurozone.”

- “Inflationary pressures strengthened in the final month of 2025, with both input costs and output prices increasing at sharper rates than in November. Despite this, in both cases the annual averages for the respective indices were the lowest since the COVID-19 pandemic (2020).”

- “Service providers posted a drop in confidence to the lowest since May, largely due to services optimism in Germany slumping to a near two-and-a-half year low. On the other hand, optimism among manufacturers in the Eurozone reached the highest since February 2022. At the combined level, business confidence in the euro area dipped to the lowest in seven months as the drop in services sentiment outweighed the improvement in optimism in manufacturing.”