ITALY DATA: Business Confidence Slips, Consumer Confidence Broad-Based Strength

Italy's business confidence index slipped 0.3 points to 97.4 in February, after five consecutive ris...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: BRC Shop Price Inflation Sees Broad-Based Increase in January

BRC shop price inflation rose to 1.5% Y/Y in January (vs 0.7% Dec), in data released released overnight. There were notable increases in inflation rates for both food and non-food categories. While this contrasts with the narrative that inflation has peaked, we would interpret the data with some caution.

- On a monthly basis, the shop price index grew 0.4% M/M (vs 0.0% Dec), driven primarily by food.

- We would caution against reading too much into this print, due the narrower range of goods compared to official CPI data, which could potentially amplify the effects of holiday discounts being reversed. Furthermore, the BRC Shop Price Monitor collects prices earlier in the month than the official ONS data - so particularly around November, December and January when there are sales and holidays the relationship between price movements in the BRC survey and the ONS official inflation data can be less stable.

- At most for us this release adds some upside risk to January's official CPI data (due 18th Feb), particularly for food.

- Food inflation increased again to 3.9% Y/Y (vs 3.3% Dec), extending further from December's rebound, looking to have been driven by ambient food. Month-on-month, prices rose a notable 1.1% (vs 0.3% Dec).

- Within food, ambient food inflation grew notably to 3.1% Y/Y (vs 2.5% Dec). Fresh food inflation rose again to 3.9% Y/Y (vs 3.8% Dec).

- Non-food inflation picked up to 0.3% Y/Y (vs -0.6% Dec), marking the first positive reading since early 2024. Month-on-month, prices rose 0.1% (vs -0.1% Dec).

- "Shop price inflation jumped due to high business energy costs and the hike to National Insurance continuing to feed through to prices", writes the BRC.

- "Meat, fish and fruit were particularly affected, also reflecting weak supply and stronger demand, while non-food categories, including furniture, flooring, and health and beauty, all saw inflation rise."

GILTS: UK Supply limits the upside in Futures

- Gilt saw another open outside of the Calls, opening lower but failing to break Friday's low at 90.94.

- Further break out lower in futures will highlight the 4.561% Yield level, this is the December high and highest print since Novemeber.

- Today this Yield level equates to 90.61.

- The UK £3.25bn 8yr Supply equates to 18.6k Gilt, which could limit some of the early upside in Futures.

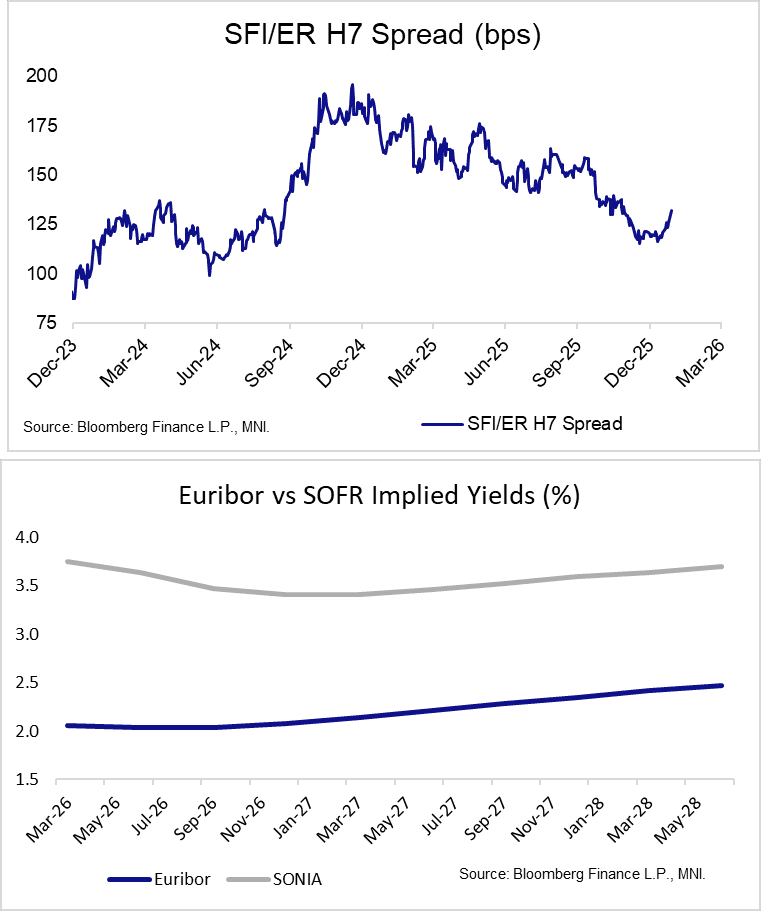

STIR: Light SONIA Underperformance vs Euribor, SFI/ER H7 At 2-month High

SONIA futures lightly underperform Euribor counterparts this morning, pushing the SONIA/Euribor H7 spread up another 2bps to 132bps, a 2-month high. In the near-term, the UK-leg will likely dictate meaningful movements in the spread. There remains more uncertainty around the pace and magnitude of the BOE’s easing cycle than the ECB. A reminder that both the BOE and ECB decisions are due next Thursday (5 February), with the BOE’s update including a full monetary policy report and forecast update.

- In OIS markets, there remain around 35bps of BOE cuts priced through December. ECB-dated OIS continue to price just over 3bps of easing through September, before the implied curve steepens to price ~1.5bps of hikes through year-end.

- The remainder of today’s UK/Eurozone calendar is light. The Spanish unemployment rate fell to 9.9% in Q3, below the 10.25% consensus and 10.45% prior.

- One area of interest in UK STIR markets this week will be the impact of the 0.125% Jan-26 Gilt redemption. See our Gilt Week Ahead for more here