USDCAD TECHS: Bullish Theme

Sep-10 20:00

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3925 High Aug 22 and the bull trigger

- RES 1: 1.3868 High Aug 26

- PRICE: 1.3850 @ 16:38 BST Sep 10

- SUP 1: 1.3782/27 50-day EMA / Low Aug 27 and a bear trigger

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact. The recovery from the Aug 29 low highlights a potential early reversal signal and if correct, marks the end of the corrective pullback between Aug 22 - 29. An extension higher would open the bull trigger at 1.3925, the Aug 22 high. Support lies at 1.3727, the Aug 29 low. Clearance of this level would instead reinstate a short-term bear theme and expose 1.3709 initially, a Fibonacci retracement.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Leaning Bull Flatter Ahead Of CPI

Aug-11 19:45

The Treasury curve leaned bull flatter Monday ahead of Tuesday's CPI release.

- With no key data or Fed speakers on Monday's schedule, and looming CPI being the week's most impactful release, trading was relatively subdued and focused more on geopolitical developments.

- That included anticipation of the Trump-Putin meeting later this week per the Ukraine conflict, and the China tariff truce which was due to expire Tuesday (but per CNBC has been extended by 90 days as widely expected).

- In contrast to last week's reports which drew a small but notable reaction (namely firming the USD), there was little reaction to a Bloomberg report that current FOMC members Vice Chair for Supervision Bowman, Vice Chair Jefferson, and Dallas Fed's Logan are in the running to succeed current Fed Chair Powell.

- Indeed Bowman's comments over the weekend re eyeing 3 rate cuts by year-end were largely taken in stride as she's been a vocal (and dissenting) dove in recent months.

- Implied Fed funds were unchanged through year-end, still eyeing 57bp of cuts. Tsy yields traded within Friday's ranges overall, with volumes light (725k TYU5 contracts traded through 3:45ET)

- As noted, Friday sees a busier schedule including CPI - MNI's preview is here. Consensus sees core CPI inflation at 0.3% M/M and unrounded analyst estimates broadly echo this with a median 0.32% M/M. We also hear from Fed's Barkin (non-2025 voter) and Schmid (2025 voter, hawk) after CPI, with other data including the NFIB small business survey and the Federal budget statement.

- Latest levels: The 2-Yr yield is down 0.4bps at 3.758%, 5-Yr is down 0.7bps at 3.8242%, 10-Yr is down 1.2bps at 4.2713%, and 30-Yr is down 0.9bps at 4.8403%. Sep 10-Yr futures (TY) up 1.5/32 at 111-28 (L: 111-25 / H: 112-0-)

FOREX: USD on More Solid Footing into July CPI Print

Aug-11 19:44

- The dollar finished the Monday session stronger, rising against most others in G10 in a relief rally and clear out of positioning ahead of the Tuesday US CPI print. The USD's move higher seemingly came in isolation, with the front-end of the US curve and core equity markets proving resilient to the edge higher in the greenback. Resultantly, strength in the USD Monday was likely an extended phase of position-squaring after the soft NFP print earlier this month (USD Index still 1.4% below pre-NFP levels), and ahead of tomorrow's CPI print - the next data input for the September FOMC decision.

- In addition, outside of the EUR, USD gains seemingly have less conviction: GBP/USD has reversed lower after a failed test on the 50-dma of 1.3502, and further weakness here will open 1.3398 support (23.6% retracement for the upleg off the 1.3142 low) ahead of the more notable level at 1.3310. Below here, the bounce will look to have concluded, and a further fade becomes more likely. Tomorrow's wages and unemployment numbers could prove key this week.

- The sole currency to outperform the greenback was NOK. Strength here persisted through Monday, helping EURNOK push through initial support at 11.9326 (23.6% retracement of the upleg off the late July low). The slightly stronger-than-expected July inflation report set the tone for NOK Monday: although CPI-ATE inflation was actually in line with Norges Bank's June MPR projections at 3.1% Y/Y, measures of inflation momentum suggest underlying price pressures remain a little persistent. This should push back against the need for firmer guidance towards a September cut at Thursday's Norges Bank decision.

- Near-term focus shifts to the RBA rate decision at which the bank are seen trimming rates by a further 25bps to 3.60%. The German ZEW survey then crosses ahead of the July US CPI print.

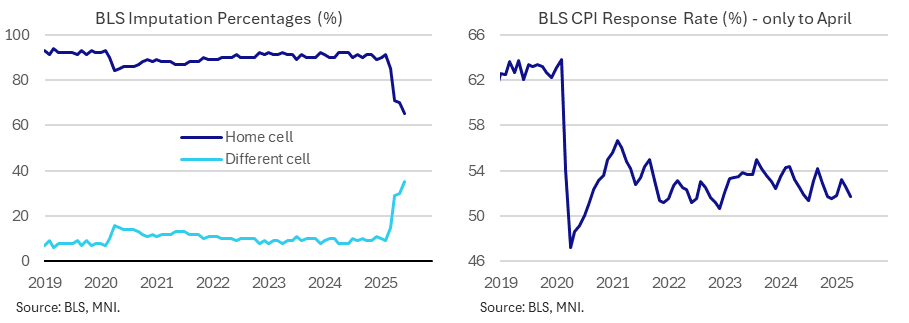

US OUTLOOK/OPINION: CPI Data Quality Concerns Even More Pronounced

Aug-11 19:36

- Questions around data quality accelerated rather than abated in last month's June CPI report and are even more pronounced heading into this week’s CPI and PPI releases after President Trump’s firing of BLS Commissioner McEntarfer after the surprisingly weak July nonfarm payrolls report on Aug 1.

- Budget cuts have seen an abrupt decline in the BLS’s ability to comprehensively collect inflation data. June saw 35% of the basket calculated from alternative sources after two months at ~30% in April/May. This compares with an average 9% through 2024 or a peak of 16% in April 2020 in the depths of the pandemic limiting survey agent activity.

- Response rates meanwhile remain low – see chart.

- One other factor to be aware of this month is a shift in source data for wireless telecoms services. Analysts we have seen reference this such as Deutsche Bank and NatWest don’t expect a significant impact but remain aware of any surprises here.

- NatWest on the matter: “The BLS will switch to alternative data source for the wireless telecommunication services component—within the overall communication services category. The wireless telecommunication services CPI component represents 1.6% of the core CPI and has roughly averaged a flat monthly reading over the last 42 months. […] We are not expecting too much of an initial change in price movements on account of this change but wouldn’t rule anything out.”