USDCAD TECHS: Bullish Phase

May-27 20:00

* RES 4: 1.3899 High Apr 8 * RES 3: 1.3875 1.0% 10-dma envelope * RES 2: 1.3869 76.4% retracement of...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Southbound

Apr-27 20:00

- RES 4: 1.4015 High Dec 2 ‘25

- RES 3: 1.3985 76.4% retracement of the Nov 5 ‘25 - Jan 30 bear leg

- RES 2: 1.3878/3967 High Apr 13 / High Mar 31 and the bull trigger

- RES 1: 1.3749 50-day EMA

- PRICE: 1.3616 @ 17:08 BST Apr 27

- SUP 1: 1.3598 Low Apr 27

- SUP 2: 1.3526 Low Mar 9

- SUP 3: 1.3482 Low Jan 30 and key support

- SUP 4: 1.3430 2.0% 10-dma envelope

The short-term bear cycle in USDCAD remains in play and the pair traded to new lows Monday. The break through 1.3631, the Apr 21 low, confirms a resumption of the downtrend and paves the way for an extension towards 1.3526, the Mar 9 low. Initial resistance is seen at 1.3749, the 50-day EMA. A clear break of this average is required to instead signal a short-term reversal.

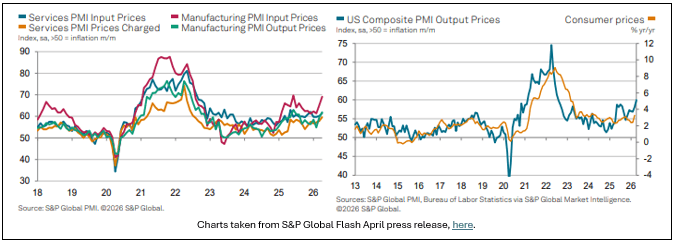

FED: Macro Since Last FOMC - Prices: PMIs Warn Upward Pressure Incoming

Apr-27 19:55

- Away from official CPI/PCE inflation, business surveys have shown a marked increase in input costs which are starting to feed through to selling prices.

- ISM manufacturing prices paid soared to 78.3 in March (+7.8pp, or +19pp over two months) for a fresh post-June 2022 high, noting a variety of input costs from steel & aluminium, tariffs on many imported goods and now increases in petroleum-based products.

- ISM services prices paid meanwhile jumped 7.7pps to 70.7 for the largest monthly increase since Aug 2012 to its highest level since Oct 2022. These were areas with clear impact from the Middle East War: the report notes "higher oil and fuel costs" impacting prices, with delivery times "unsurprisingly" longer "with shipping issues and flight disruptions due to the Middle East conflict and winter weather".

- Interestingly, the NFIB small business survey pointed to a notably weaker price outlook, with the diffusion of firms’ expectations for their own price setting falling to a joint low (in this case narrowest) since Apr 2023.

- However, the more timely flash April PMI release published Thursday noted that "Input cost inflation accelerated and supply delays worsened at a pace not seen since mid-2022, contributing to the largest monthly jump in average selling prices for goods and services since July 2022."

For more detail on March developments, see our latest Inflation Insight - “Core Relief Overshadowed By Energy” (link).

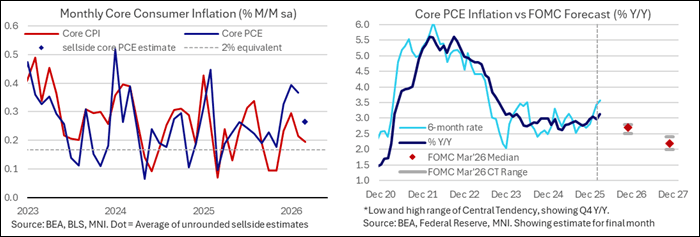

FED: Macro Since Last FOMC - Prices: Limited Initial Energy Indirect Effects

Apr-27 19:53

- Core PCE inflation continued to run at a strong pace even before the onset of the Middle East conflict. It printed 0.37% M/M in February at 0.37% M/M to continue a strong run after 0.39% M/M in Jan and 0.33% M/M in Dec, and with the Y/Y at 2.97% for a third consecutive month rounding to 3.0 or 3.1%. It had previously last rounded to 3% or above in Feb 2025 via a low of 2.6% in Apr 2025 before tariff effects started to more materially show.

- Since then, CPI and PPI headline measures have shown strong increases linked to direct energy effects, with gasoline-driven energy in CPI seeing one of its strongest monthly increases on record. Underlying details have however avoided at least some of the more hawkish outturns that could have been seen. Nevertheless, there have been strong increases in some sensitive areas, especially in tech-related areas due to shortages, and these typically carry a larger weight in PCE than CPI.

- Indeed, whilst cooling sequentially, we see analyst estimates centered around a still strong 0.26/0.27% M/M in March, albeit with a wider range than usual owing to oddities in sourcing legal services.

- The March PCE report won’t be released until the day after the FOMC decision but we suspect this mid-point isn’t a bad assumption for what Fed staff will be working from when updating policymakers. If accurate, that would see core PCE inflation at 3.1% Y/Y, and with a good chance of rounding to 3.2% Y/Y, for a continuation of no further progress towards the 2% inflation target.

- For context, whilst obviously still some time away, the median FOMC participant revised up their core PCE inflation forecast for 4Q26 up from 2.5% to 2.7% Y/Y in last month’s March SEP.

- We are core PCE focused here but it’s of course worth noting the 0.87% M/M rise in headline CPI on the back of a 11% M/M increase in energy as gasoline prices rose a historically sharp 21% M/M.