THB: BoT Says Acted On Baht, 1mth Implied Vols Near Recent Lows

USD/THB sits near 31.88 in latest dealings, up close to 0.30% for the session, but still short of recent highs (31.965).

- A short while ago a series of headlines crossed. The BoT noted it had acted on the baht and would continue to monitor it closely (looking to avoid excessive moves). It added that the baht was stronger than what was implied by underlying fundamentals but that it hadn't seen any unusual speculation (per RTRS). The central bank also reiterated that the baht had been discussed with the Thailand FinMin.

- The BoT also stated that there were no plans to introduce a gold tax soon. This echoes earlier comments this week from the out-going BoT Governor. It was noted consultations need to take place before such steps can be considered.

- 1 month implied vols for USD/THB continue to hold around 7%, which is near recent lows, so broader market sentiment is not expecting a sharp THB move (even if it is a renewed focus point for the new Thailand government).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Holds Losses, Fed Speakers & Minutes Later

Gold has been range trading today falling to $3311.6/oz before rising to $3319.59. It is currently 0.1% higher around $3318.8 holding onto Tuesday’s losses driven by steps taken towards a Ukraine truce. With markets hoping Fed Chair Powell will reveal his thinking for the September 17 decision on Friday, they are moving in narrow ranges. US yields are little changed and the USD index is 0.1% higher.

- Silver is down 0.5% to $37.212 off the intraday low of $37.170. A clear break of the 50-day EMA at $37.077 is needed to strengthen the short-term bearish threat. Initial resistance is at $39.655.

- Equities are also generally weaker with the Nikkei down 1.7%, Hang Seng -0.6% and S&P e-mini -0.3%. Oil prices are moderately higher with WTI +0.4% to $61.99/bbl. Copper is up slightly.

- Later the Fed’s Waller and Bostic appear and the July FOMC meeting minutes are published. UK July CPI & PPI, euro area July CPI and German July PPI print. ECB President Lagarde appears on a panel.

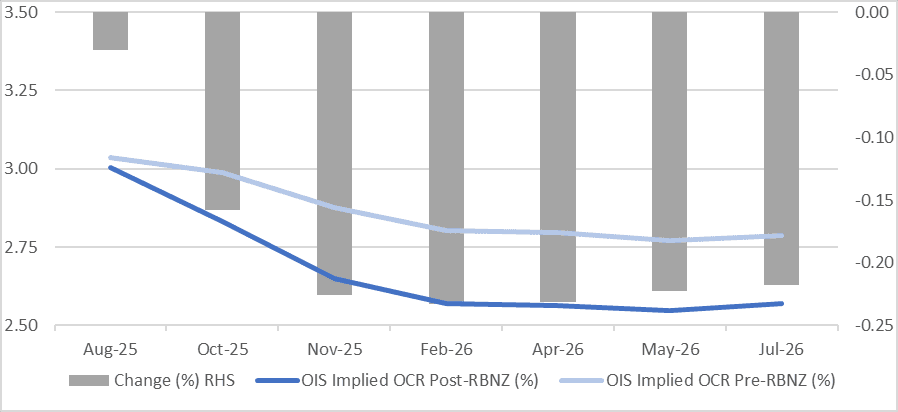

STIR: RBNZ-Dated OIS Shunt Softer After RBNZ Decision

RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August following today’s RBNZ Policy Decision.

- The market had priced 22bps of today’s 25bp cut going into the decision.

- 35bps of cumulative easing is now priced by November 2025 versus 12bps before the decision.

Figure 1: RBNZ Dated OIS Post-RBNZ vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

JGBS: Mostly Cheaper With A Steeper Curve

JGB futures are little changed, -3 compared to settlement levels.

- Japan Export Growth Negative, Lagging Other Parts Of Asia : Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -117.5bn, against a 198.5bn forecast.

- Japan Core Machine Orders Above Forecasts, Suggesting Resilient Capex : Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 0.5bp lower (7-year) to 3bps higher (40-year). The benchmark 10-year yield is 0.4bp higher at 1.606% versus the cycle high of 1.616%.

- Swap rates are flat to 1-2bps higher, with a steepening bias.

- Tomorrow, the local calendar will see Weekly International Investment Flows, S&P Global PMIs (P) and Machine Tool Orders alongside an Auction for Enhanced-Liquidity 5-15.5 YR.