UK: BOE: 5-4 Vote For 'Finely Balanced' 25bp Cut In First Ever Second Ballot

The BOE MPC voted 5-4 to cut Bank Rate to 4.00% after a second ballot.

- Four members (Greene, Lombardelli, Mann and Pill) voted to maintain Bank Rate at 4.25%, as the "disinflationary process had slowed and the risk of inflation expectations feeding through to second-round effects had risen".

- In the first vote, Alan Taylor had opted for a 50bp cut, but switched to a 25bp cut in a second ballot in order to secure a majority on Bank Rate.

- The remaining members voted for a 25bp cut. From the minutes: "There had been sufficient progress in underlying disinflation albeit, for some of these members, with a risk that this momentum could slow".

- Governor Bailey said the decision was "finely balanced". He noted rates are still on a "downward path" but "future cuts will need to be made gradually and carefully."

- There were subtle, but important changes in to the guidance. While a "gradual and careful" approach to cuts is still warranted, MPC emphasised that "the restrictiveness of monetary policy has fallen" and that "the timing and pace" of future cuts would depend on "the extent to which underlying disinflation pressures continue to ease".

- Headline inflation forecasts were raised a tenth to 2.0% Y/Y at 2/3-year horizons. The MPS said that "the upside risks around medium-term inflationary pressures have moved slightly higher since May".

- There was a small upgrade to near-term unemployment projections, with the MPS and minutes pointing to a continued "gradual loosening" of labour market conditions.

- The MPR contained a Box on QT, but no forward guidance for the September decision was provided. Staff estimate that QT has contributed to a 15-25bp rise in 10-year term premia, up from a 10-20bp estimate last year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

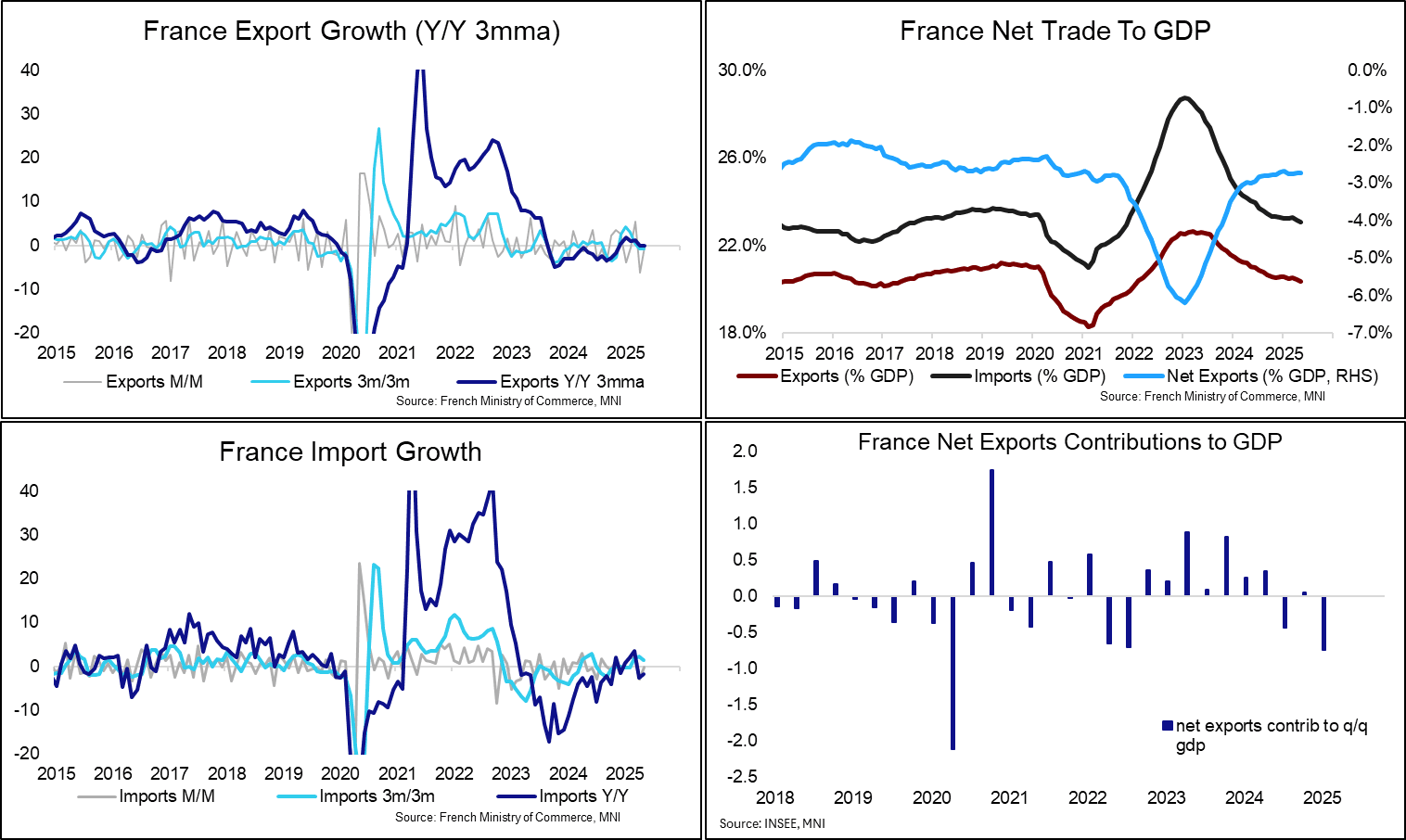

FRANCE DATA: Import and Export Trends Sluggish Post Covid (1/2)

While the French goods trade deficit to GDP is broadly back in line with pre-covid levels (~3%), the downward trend in both exports and imports is reflective of a broader sluggishness in activity. Weak demand is constraining imports, while trade uncertainty and soft partner demand is limiting export growth.

- The trade deficit was E7.8bln in May according to Ministry of Commerce data, up from E7.7bln in April. Exports (ex-military equipment) fell 0.3% M/M to E48.8bln. Export growth has been negative on an NSA sequential basis for four of the last 5 months (March was an exception with +5.3% M/M growth).

- Meanwhile, imports (ex-military equipment) fell 0.2% M/M to E56.7bln, following a 3.0% M/M fall in April. Imports were down 1.7% Y/Y in May (vs -2.6% in April, +3.4% in March), consistent with weak domestic consumption and industrial production trends seen in recent months.

- Net exports pulled Q/Q real GDP down by 0.7pp in Q1. Recent export weakness suggests a similar drag may also be seen in Q2.

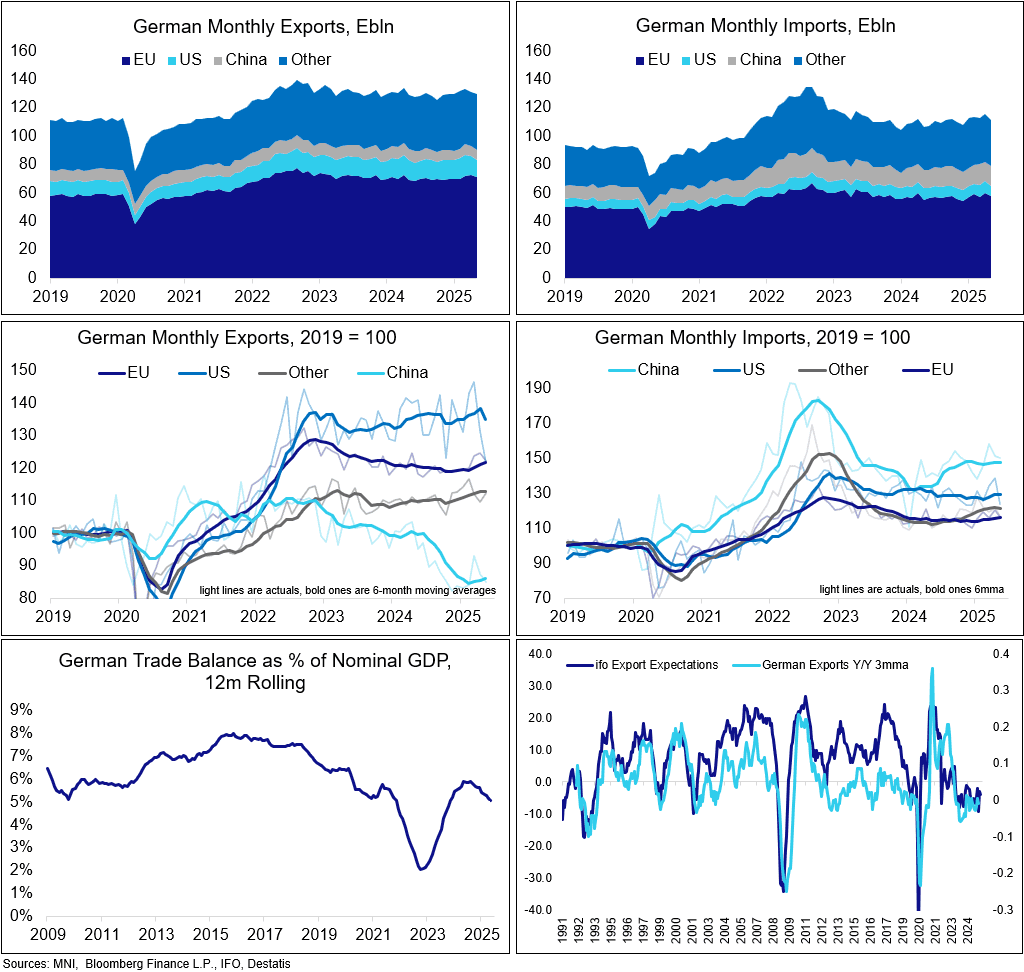

GERMAN DATA: Trade Balance Extends Real-Terms Downtrend

The German trade surplus increased in May to E18.4bln (seasonally-adjusted, vs E15.5bln cons; E15.7bln prior, revised from E14.6bln). Both exports (-1.4% M/M vs -0.5% cons; -1.7% prior, revised from -1.6%) and imports (-3.8% M/M vs -1.7% cons; 2.2% prior, revised from 3.9%) declined.

In real terms, as a % of nominal GDP on a 12-month rolling basis, the trade balance series extended its current downtrend, at 5.1% as of May, 0.9pp below levels seen around a year ago (vs 8.0% 2015 high, 2.1% 2022 low, bottom left chart).

- Across countries, an export drop to the US is consistent with the firmer tariff stance in the country. Exports to China meanwhile also dropped, sitting close to their post-pandemic lows, suggesting that an April jump might have been a one-off (mid-left chart).

- May German factory orders data showed the series holding up comparatively well from the foreign side - that could suggest some rebound in exports over the next months.

- Lower imports across the board of constituencies (mid-right chart) seen in May can be indicative of low domestic demand in the month.

- IFO export expectations fell in June, to -3.9 (-3.0 May), remaining well subdued on a historical comparison.

- "The United States has offered an agreement to the European Union that would keep a 10 percent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits", Politico quoted an EU diplomat overnight - arguably, that would be quite favourable conditions for the bloc.

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Still Present

- On the commodity front, a recent move lower in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note that the latest recovery highlights a possible false trendline break. A resumption of gains would refocus attention on $3451.3, the Jun 16 high. The bear trigger lies at $3248.7, the Jun 30 low.

- In the oil space, WTI futures maintain a softer tone following the reversal from the Jun 23 high, and recent gains appear corrective. Support to watch is the 50-day EMA, at $64.96. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.