FED FUNDS FUTURES: BLOCKs: Jan'26 Fed Funds sales

Oct-30 14:52

- -25,000 FFF6 96.31 from 1040:17 to 1048:57ET

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Breeden due to speak on monetary policy at 16:30BST

Sep-30 14:48

- Deputy Governor Sarah Breeden rarely speaks on monetary policy but her speech scheduled for today at 16:30BST at Cardiff University is provisionally entitled “The Monetary Policy Outlook”.

- This will certainly be a key speech. She sounded slightly more dovish than Governor Bailey in our view following her testimony ahead of the TSC on 3 June but hasn’t really spoken on monetary policy since.

- Her tone is likely to be pivotal for markets, particularly if she strikes a dovish tone given current market pricing.

- We think that markets are underpricing the probability of a Q4 cut with less than 1bp priced for November and less than 5bp cumulatively priced for December.

- Note that yesterday, Deputy Governor Ramsden did not rule out voting for a cut in November but was generally considered the most dovish member to not dissent at the September MPC meeting. In order to reach the five members needed for a cut we would need the two September dissenters (Dhingra and Taylor) and then likely all of Ramsden, Breeden and Bailey. That leaves the four members who hawkishly dissented in August continuing to favour a skip.

SOFR OPTIONS: Latest Vol Sales

Sep-30 14:43

- -5,000 SFRX5 96.12/96.62 strangles, 1.75

- -3,000 SFRV5 96.31 straddles, 6.25-6.0

- -12,900 0QV5 96.93 calls 4.5 ref 96.905

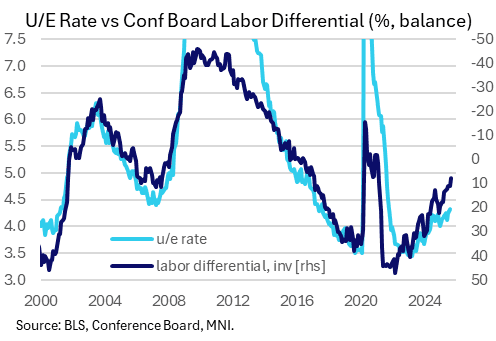

US DATA: Conference Board Labor Differential Hits Fresh Cycle Low

Sep-30 14:38

Standing out in a broadly weak Conference Board consumer confidence survey for September, the "labor differential" (jobs "plentiful" minus "hard to get") fell to 7.8 from 11.1 in August (rev from 9.7). That's the weakest since 2017 when excluding the 2020-21 pandemic period.

- While the percentage of those seeing jobs as "hard to get" was steady at 19.1%, the proportion seeing jobs as "plentiful" (26.9%) was the lowest since February 2021, but excluding the April 2020-Feb 2021 pandemic period, it was the lowest since February 2017.

- This is a closely-watched indicator for broader labor market conditions. It's historically correlated with the unemployment rate and having come down from over 22 at the end of last year, this has shown a decisive cooling which points to a continued rise in joblessness. A similar reading in 2017 was consistent with unemployment around 5.0%, vs 4.3% as of August.