GILTS: Bear Flattening Early On

Jun-28 07:54

Gilt futures look through yesterday’s low after dealing either side of late Tuesday levels around the open, before ticking away from session lows, leaving the contract just below flat on the day. Cash Gilts run little changed to 4bp cheaper, as the 2-/10-Year curve bear flattens to fresh inverted cycle extremes, with 2-Year yields registering a fresh cycle high.

- Terminal pricing on the BoE-dated OIS strip settles around the 6.30% mark in policy rate terms.

- The SONIA strip steepens, showing flat to -3.5 through the reds at typing.

- Domestic headline flow has remained focused on the housing market, which has seen steeper discounting in recent times.

- Looking ahead, BoE Governor Bailey will participate in a 4-way panel with the chiefs of the Fed, ECB & BoJ this afternoon, while BoE’s Pill is set to speak this morning.

- Elsewhere, the DMO will return to the market, looking to sell GBP2.75bln of the 15-Year 3.75% Jan-38 line.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: USDCAD Under Pressure With Equities & Oil Lifted

May-29 07:39

- USDCAD lifts 10 pips off session lows of 1.3584 (-0.2%) but broadly remains under pressure with the S&P E-mini holding the day’s gains (albeit off the post-open snap higher) and with WTI also extending Friday’s recover to chip further away at Thursday’s slide after weekend debt talk progress.

- It sees the pair move closer to the middle of technical levels, after Friday’s high of 1.3655 and then 1.3647 post-strong US data came closer to key short-term resistance at 1.3668 (Apr 28 high). As it is, there is still some leeway to support at 1.3485 (May 23 low) after sizeable gains the day after helped by a hawkish Waller.

- A normal trading day for Canada, volumes are nevertheless likely to be heavily depressed with Memorial Day observances. The docket is suitably light, with weekly Bloomberg Nanos consumer confidence and a 24-day bills auction. Data will soon heat up though with GDP on Wed one of the last key releases before the BoC on Jun 7.

EGBS: Holding A Modest Rally Since The Cash Open

May-29 07:14

- Bunds have seen two-way trade since the cash open but remain constrained to relatively narrow ranges, and easily within Friday’s range, with reduced volumes on Memorial Day observances elsewhere.

- RXM3 trades +0.19 at 133.12 (cumulative volumes just 12k) off a recent low of 133.10 and an overnight low of 133.05 after the open, but hasn’t looked to trouble support at 132.83 (Fri low). There is no sign of the contract breaking out of the current bear mode though, with resistance notably higher at the 20-day EMA of 134.52.

- In yield space, EGBs trade relatively tightly across the board, with Bunds -0.8bps and only slightly underperforming OATs and BTPs, with the BTP-Bund spread dipping just 0.3bp to 183.8bps for still the tightest since May 19.

- Little by way of German data until regional CPIs on Wed.

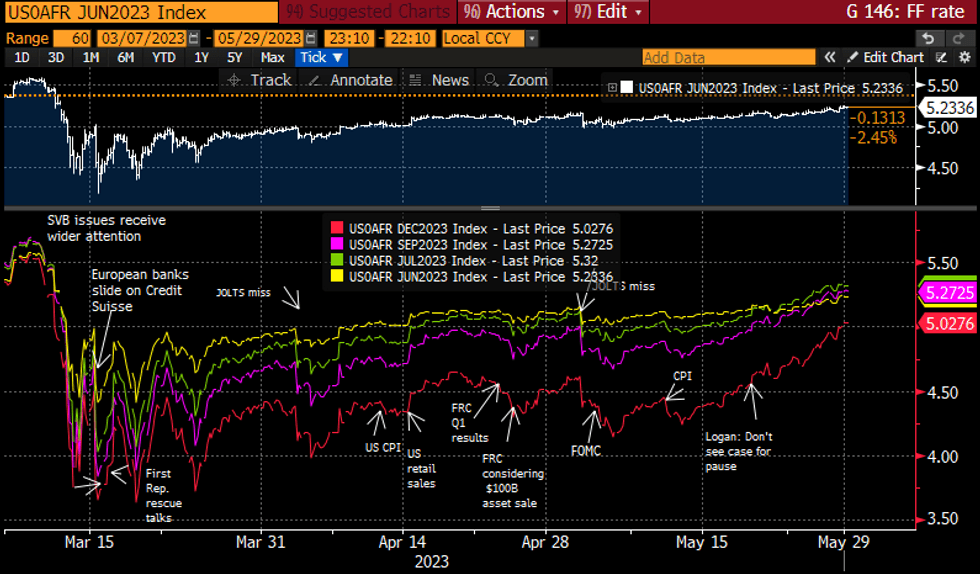

STIR: Fed Cuts Trimmed Further After Debt Talk Progress

May-29 06:34

- Fed Funds implied rates are off overnight highs but have continued to unwind cuts later in the year after weekend debt deal is set to head to Congress.

- Less than 50bp of cuts from July peak to January.

- Cumulative from 5.08% effective: +15.5bp Jun (-0.5bp from Fri), +24bp Jul (-1bp), +19bp Sep (+0.5bp), +8.5bp Nov (+2.5bp), -5bp Dec (+3bp) and -20bp Jan (+3.5bp).

- Chicago Fed’s Goolsbee (’23 voter) in an interview with CBS on Sunday echoed other Fed speakers that he doesn’t want to prejudge June’s rate move [notable releases between now and then include payrolls on Jun 2 and CPI on Jun 13].

- He did however keep to dovish leaning remarks that Fed moves takes months, years to work through the economy.

- Other comments meanwhile took aim at debt talk discussions despite weekend progress: seeing fear and uncertainty in rates over an impasse and with a last minute deal “a little dangerous”.

Source: Bloomberg

Source: Bloomberg