ARGENTINA: BCRA Introduces New Restriction For USD Purchasers

Sep-26 16:39

- The BCRA has prohibited dollar buyers from purchasing dollar-settled bonds for 90 days, according to a publication on its website, reported by Bloomberg.

- According to the headlines on BBG, the BCRA will also require banks to obtain sworn affidavits from clients seeking to buy dollars.

- "*ARGENTINA'S BCRA ADDS NEW RESTRICTION TO BUY DOLLARS, USD BONDS" – BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Interview with Former Richmond Fed President Jeffrey Lacker

Aug-27 16:39

- MNI interviews former Richmond Fed President Jeffrey Lacker -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

PIPELINE: Corporate Bond Update: $3B Ontario 5Y SOFR Priced

Aug-27 16:26

- Date $MM Issuer (Priced *, Launch #)

- 08/27 $3B *Ontario 5Y SOFR +52

- 08/27 $2B *ESM 2030 WNG +39

- 08/27 $1.25B *Saudi Awwal 10NC5 +220

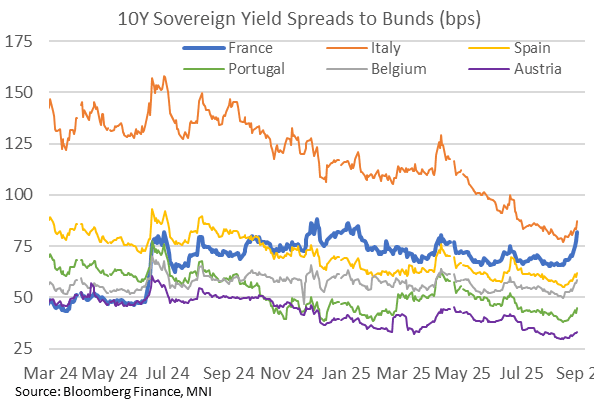

FRANCE: OAT-Bund Spread Hovering At 82bps, ING See Risks Tilted Wider

Aug-27 16:03

- OAT-Bunds spreads have been hovering around 82bps for a couple hours now after a further large widening today, +4.5bp on the day for +11bp since Monday’s Bayrou’s confidence vote call.

- It’s been a volatile session for outright yield moves, with the 10Y yield currently at 3.517% (+2.1bp) off an earlier high of 3.544% for new recent highs.

- Meanwhile, 30s have pared earlier losses which saw a fresh fourteen-year high with a 5bp increase to 4.45% (currently 4.422%, +3.2bp).

- In futures space, OATU5 trades at 121.74 (-0.18) after a short-lived pop to 121.98 on little sign of headlines, off an earlier (and new recent) low of 121.48. 3.55% yields equate to ~121.44.

- One point of interest will be ~120.66, the equivalent to a 3.631% yield from the ytd high in March which marked its highest since Nov 2011.

- ING: “We still see the balance of risk tilted to further widening [in OAT-Bund spreads]. The current 10Y spread is at a similar level to that seen in July 2024, when French President Emmanuel Macron called snap elections and OATs sold off significantly in response. However, spreads remain tighter than they were during the political turmoil following the collapse of Prime Minister Michel Barnier’s government last December. A key difference now is that parliamentary elections are allowed again, which in our view adds to the uncertainty from both a political and fiscal perspective.”

- “We do have to keep in mind that the ECB has a lot of firepower to limit excessive widening of EGB spreads, and markets are well aware of this. In theory, the ECB could resort to the Transmission Protection Instrument (TPI) if too-high interest rates on OATs negatively impact the steering of monetary policy. The conditions require a country to comply with EU fiscal rules. At the same time, however, the ECB has the ability to deviate from this requirement, an option it would likely exercise if spillover effects threaten financial stability. As such, the mere existence of this tool may be enough to prevent spreads from spiralling upwards.”

- See this morning’s MNI exclusive for more color on fiscal matters: French Austerity Plan To Largely Survive Crisis-Officials (1121BST)