US-EU: BBG-EU Expects Exemption From US 15% Tariff Boost

Bloomberg News reports : https://www.bloomberg.com/news/articles/2026-03-04/eu-expects-to-be-exempt-...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

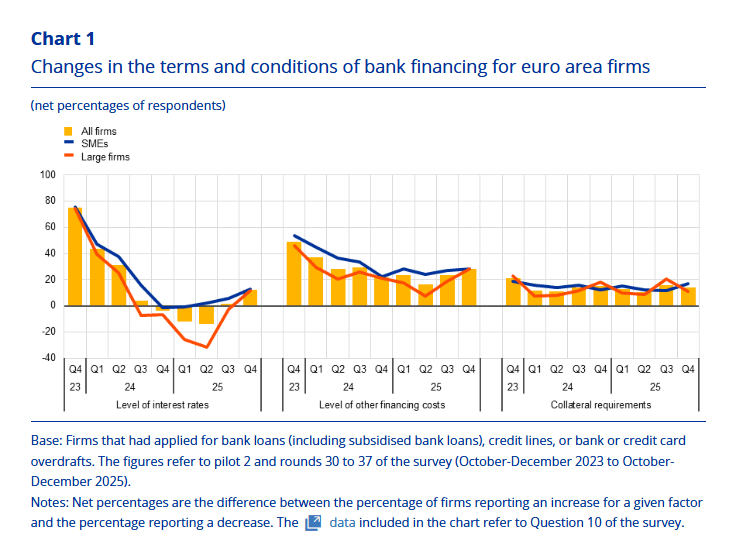

EUROZONE DATA: SAFE Indicates A Net Tightening Of Financing Conditions In Q4

The ECB’s Q4 Survey on the Access to Finance of Enterprises (SAFE) indicated a perceived net tightening of financing conditions from the perspective of Euro area firms. The results will need to be interpreted alongside tomorrow’s Bank Lending Survey, which will provide an update on lending conditions from the perspective of banks.

- These surveys help inform the ECB’s assessment of the effectiveness of policy transmission, alongside providing credit-based growth signals. See our latest review of monthly credit data here

The SAFE press release noted that “euro area firms reported a net increase in interest rates on bank loans (net 12%, compared with 2% in the previous quarter….”a net 28% of firms (up from 23% in the previous quarter) observed increases in both other financing costs (i.e. charges, fees and commissions) and collateral requirements (net 14%, compared with 16% in the third quarter of 2025)”

- “In this survey round, firms reported a modest rise in their need for bank loans (net 3%, up from 0% in the third quarter of 2025), accompanied by a small perceived decline in availability (net -2%, compared with -1% in the third quarter)”.

- “Firms continued to perceive the general economic outlook to be the main factor constraining the availability of external financing (net 20%, compared with 19% in the previous survey round) and indicated a slight improvement in banks’ willingness to lend (net 4%, up from 2%).”

Summarising non-credit focused questions from the survey:

- “Firms’ expected their selling prices to rise by 2.9% on average over the next 12 months (similar to the previous survey round), while the corresponding figure for wages was 3.1% (up from 3% in the previous round)”

- “Firms’ inflation expectations were broadly unchanged over all horizons”…“For the five-year horizon, most firms continued to indicate that risks to the inflation outlook were tilted to the upside (net 56%, up from 53% in the previous round).”

- "In this survey round, firms were asked about their use of artificial intelligence (AI). Results show that 27% of euro area firms do not use AI, 33% use it very infrequently, 31% moderately and 7% significantly"

US TSY FUTURES: BLOCK, Mar'26 10Y Sale

- -5,000 TYH6 111-25. sell through 111-26.5 post time bid at 0858:00ET, DV01 $328,000.

- the 10Y contract trades 111-24.5 last (-2).

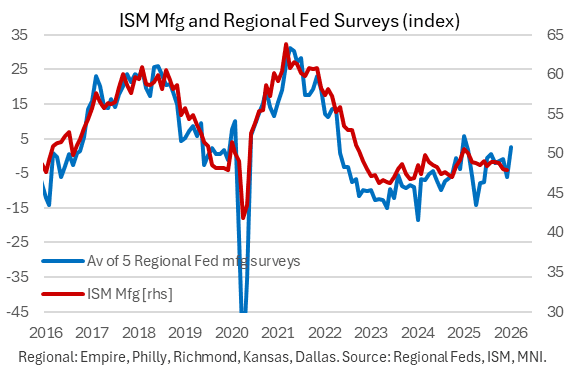

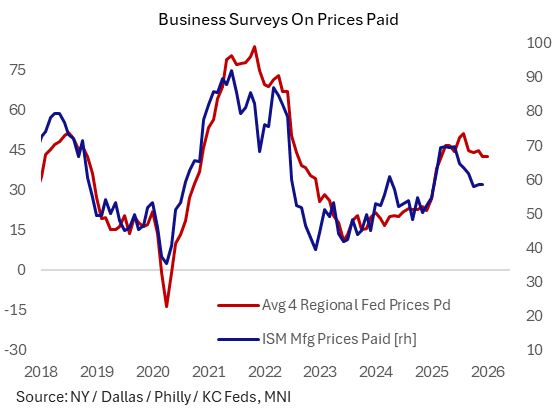

US PREVIEW: All Signs Point To Stronger ISM Manufacturing In Jan, Mixed Prices

January's ISM Manufacturing report (1000ET) is expected to reflect an improvement in activity indices from a surprisingly weak December, with inflation remaining stubbornly high. Consensus is for a move up in the headline PMI index to 48.5 from 47.9 in December, which had missed the 48.4 consensus to edge to a 14-month low. In the context of soft recent readings, a 0.6 point uptick would represent a 3-month high but the 11th consecutive sub-50 reading.

- The Employment sub-index is expected to rise to 46.0 from 44.9 prior; there's no consensus for New Orders but prior was 47.7. Both were areas of improvement in December's report (+0.9 for Employment and +0.3 for New Orders) with Production (-0.4 to 51.0) and inventories (-3.7 to 45.2) dragging, with imports down 4.3 points to 44.6 but export orders ticking up 0.6 points to 46.9.

- Various proxy indices of manufacturing activity point to an uptick: the S&P PMI flash reading was up 0.1ppp to 51.9 (expected to be revised up another tenth to 52.0 in the final at 0945ET), with the Chicago Business Barometer, produced with MNI, jumping 11.3 points to 54.0 in January for the first expansion since November 2023 driven by broad sub-index gains. Across Fed surveys, we saw marked improvements in NY, Philadelphia, and Dallas, with Richmond and Kansas City basically flat. This produced the first positive average z-score across all 5 indices since a year earlier.

- For prices paid, disinflationary progress is still expected to be limited: 58.5 in December, the sub-index is seen rising to 59.3 in January (December's report had defied consensus for a 0.2pp uptick to 58.7, staying steady instead). Regional Fed manufacturing prices were more mixed in this regard - NY and Philadelphia saw solid drops in current Prices Paid, with KC, Richmond, and Dallas ticking up to multi-month highs. The MNI Chicago PMI's Prices Paid fell 9 points to the lowest since January 2025.

- That said, S&P PMI noted "manufacturing input prices rose at the fastest pace since last September, once again widely blamed on tariffs".

- Note that this report incorporates revised seasonal factors that will impact prior data readings for key subindices.