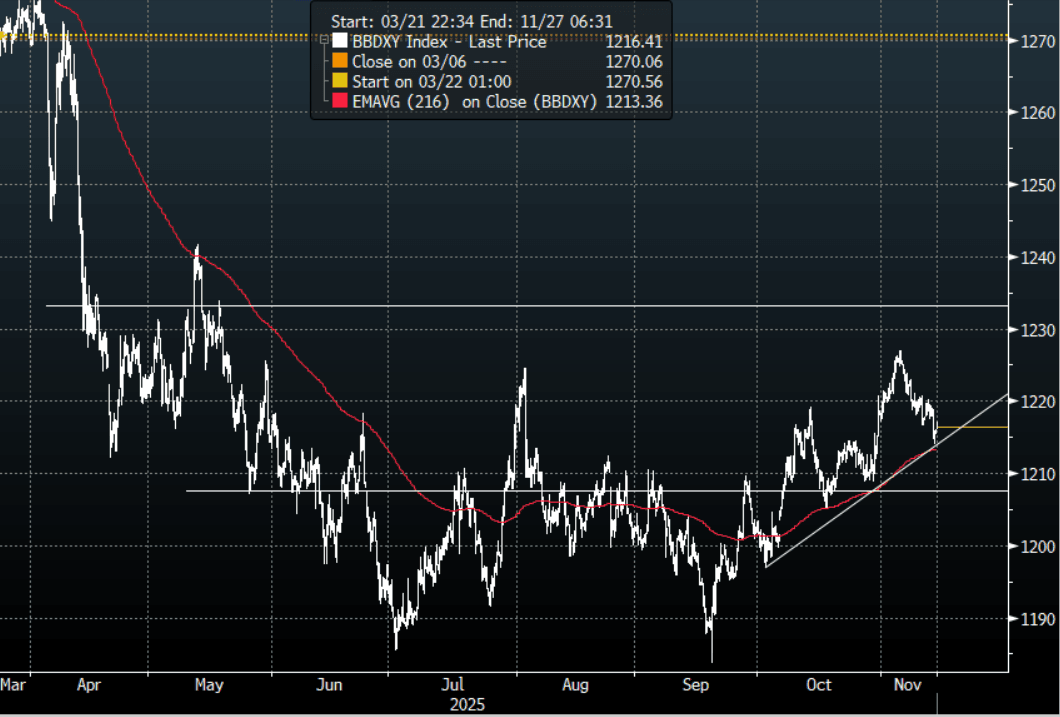

USD: BBDXY - Finds Support Toward 1213, Can It Build A Base Down Here ?

The BBDXY range overnight was 1213.92 - 1218.81, Asia is currently trading around 1216, +0.05%. The USD fell back toward the 1210-1215 support where it found some demand first up. Risk took an ugly turn last night and the USD was late to react, we have seen periods this year where the USD has not traded like a safe haven. Yet the Risk-Reward around this support area for me says this is the side I would be skewed towards. I expect we do some more work around these levels but I would be looking for signs of a base forming from which to move higher again if risk stays under pressure. Short-term the 1221-1222 area remains the pivot on the topside and we would need a move back above there to build for a retest of the 1230-35 area.

- Joseph Wang posted on X regarding the Feds changing views on cuts, "Strange so many Fed presidents are pushing back against a December cut. The bias in September was 3 cuts, and since then we have had limited official data with the shutdown itself a modest economic headwind."

Fig 1: BBDXY 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Taiwan Sees Outflows, While India More Positive On Rate Cut Hopes

Asia Pac net equity flows have been mixed to start the week. South Korea has seen mixed trends since onshore markets returned from the early Oct break. We are positive for the past 5 trading days, but aggregate sums remain below recent highs. The Kospi is just below record highs, while focus remains on local chip makers linked into the global tech/AI boom. Sentiment in this space remains positive, but we have had a very strong run higherin recent months. In contrast, inflows into Taiwan have clearly lost momentum, with $2.3bn in net outflows for the past 5 trading days. Price action in the Taiex has been choppy in the past week, with offshore investors potentially taking some profit after most of Sep saw quite strong inflows (+$7.3bn for the month)

- Elsewhere, inflow momentum has been stronger into Indian markets, over $1.2bn in the past 5 trading days. Inflation outcomes have given hope to easier RBI policy settings, although local equities are struggling to build on earlier Oct gains.

- In South East Asia, outflow pressures have mostly been evident, although Indonesia's 5-day sum remains positive.

- Outflows from Malaysia have been most prominent from a trend standpoint, with local equities down sharply from earlier Oct highs abvoe 1650.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 311 | 582 | 2671 |

| Taiwan (USDmn) | -411 | -2313 | 7563 |

| India (USDmn)* | 400 | 1251 | -16526 |

| Indonesia (USDmn) | -82 | 133 | -6175 |

| Thailand (USDmn) | -88 | -163 | -3028 |

| Malaysia (USDmn) | -76 | -376 | -4116 |

| Philippines (USDmn) | -6 | -10 | -703 |

| Total (USDmn) | 49 | -894 | -20314 |

| * Data Up To Oct 13 |

Source: Bloomberg Finance L.P./MNI

US TSYS: Treasury Yields Grind Lower at Open of Asia Trading Day

As cash bonds set up for another trading day, futures had guided prices marginally lower after the overnight rally in the US. As TYZ5 trades down -01+ at 113-11 bond yields are opening up marginally lower.

- The US 2-Yr is at 3.381%, close to 0.5bp lower in early trade.

- The US 5-Yr is at 3.607% having closed prior to Columbus day at 3.626%.

- The US 10-Yr is down -0.5bps to 4.028% having failed to test 4.00% prior. It had looked likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out.

- The US 30-Yr is down -0.5bps at 4.628%

- The catalyst for the overnight rally was comments from Fed Chairman Powell indicating that the outlook for inflation and employment appears to have changed little since September, keeping intact expectations for two more rate cuts this year.

- Key data in the calendar for later is Empire Manufacturing which is forecast to decline -1.8 following -8.7 in September and Real Average Hourly Earnings.

NZD: Kiwi Softer As RBNZ’s Conway Says OCR At Lower End Of “Neutral”

NZDUSD has dipped today to around 0.5709 following comments from RBNZ chief economist Conway and that he’s “confident” the output gap will close and that rates are towards the bottom end of neutral suggesting that further easing will bring policy into stimulatory territory. At this stage another cut on 26 November looks likely.

- Conway reiterated that rates are “getting toward the lower end” of the neutral range. The RBNZ estimates it to be around 2.5-3.5% and the OCR is currently at 2.5% after October’s 50bp cut. He also repeated that excess capacity should help inflation return to the 2% mid-point of the band.

- His speech was on the policy lessons learned from the pandemic period which included recent research on the effect of Large-Scale Asset Purchases (LSAPs). He stated that “while certainly not perfect, LSAPs need to remain a key part of our additional policy toolkit for targeted interventions during financial and economic crisis when the Official Cash Rate has reached its lower limit.” But additional tools are unlikely to be used anytime soon.

- Kiwi was impacted by generally weaker risk appetite on Tuesday related to US-China trade concerns as China retaliated against the US’ investigation into shipping. NZDUSD fell 0.2% to 0.5716 on Tuesday off the intraday low of 0.5683 helped by comments from US trade representative Greer that staff-level talks with China were taking place increasing hopes of a solution.

- AUDNZD is up 0.2% to 0.1365 so far today driven by the contrast between the RBNZ’s clear easing bias and the RBA’s caution and focus on upside risks in its 30 September meeting minutes. AUDNZD fell to 1.1323 on Tuesday and finished down 0.3% to 1.1349.