MEXICO: Banxico Governor Rodriguez Sees No Secondary Impact From Tax Hikes

* Speaking during the presentation of the Q4 Quarterly Inflation Report, Banxico Governor Rodrigue...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Hike As BOC's Next Move Is The Base Case, But Paths To A Cut Remain

The Bank of Canada is overwhelmingly expected by both markets and analysts to maintain its overnight rate at 2.25% at the January meeting (announcement on Jan 28), as we explain in our preview (link).. This would be a 2nd consecutive pause as part of what is anticipated to be a flat rate path through 2026. The biggest question is, in which direction will the next move be? The account of the deliberations at the December meeting highlighted that Governing Council debated "whether it was more likely that their next move would be to raise or lower the policy interest rate." It remains more likely than not that the next move will be a hike, with a downside shock required for cutting again.

- As the December deliberations began, it seemed at the time that there was not just a firm case for the easing cycle to already have ended, but that a hike would definitely be more appropriate as the next move. The policy rate was at the lower end of the estimated 2.25-3.25% neutral range, employment had bounced back strongly over a multi-month period, inflation remained above-target, and uncertainty over the Canada-US trade conflict appeared to have abated.

- But since then, December data suggested that underlying inflation was softening while employment gains had slowed again, and most importantly US-Canada trade relations appeared to deteriorate again. We review the latest data below but it’s largely consisted of dovish surprises of late that have removed impetus for near-term hiking.

- With rates "at about the right level", Governor Macklem noted last month that it would take "a new shock" or "an accumulation of evidence" to "materially change the outlook", and the data received since December do not rise to that standard. While the latest quarterly Monetary Policy Report (MPR) projections released at this meeting will mark-to-market a more mixed trajectory for GDP growth than seen at the last edition in October, there is unlikely to be much of a change in the inflation outlook.

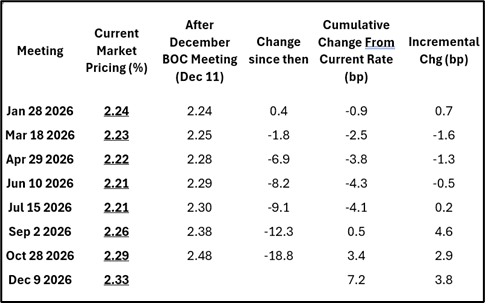

- In line with the BOC’s uncertainty, market pricing has reflected the somewhat ambiguous outlook for the next BOC move. Meeting-dated OIS continues to see the easing cycle at an end, with a moderate chance of a hike by end-2026 but more likely in 2027. See table at right for implied overnight rates.

- But compared with pricing at the conclusion of the last meeting in December, rates markets have faded near-term rate hike expectations, with a little bit of easing creeping back into the profile through mid-2026 (about 4bp of cuts through July vs 5bp of hikes having been expected). There remains a lean toward a hike by end-2026 though only very faintly, with about 8bp in net cumulative tightening by the December meeting. This shift has come with a moderation in both core CPI and employment data since the December meeting, as well as a resurgence in geopolitical risks/US-Canada trade tensions.

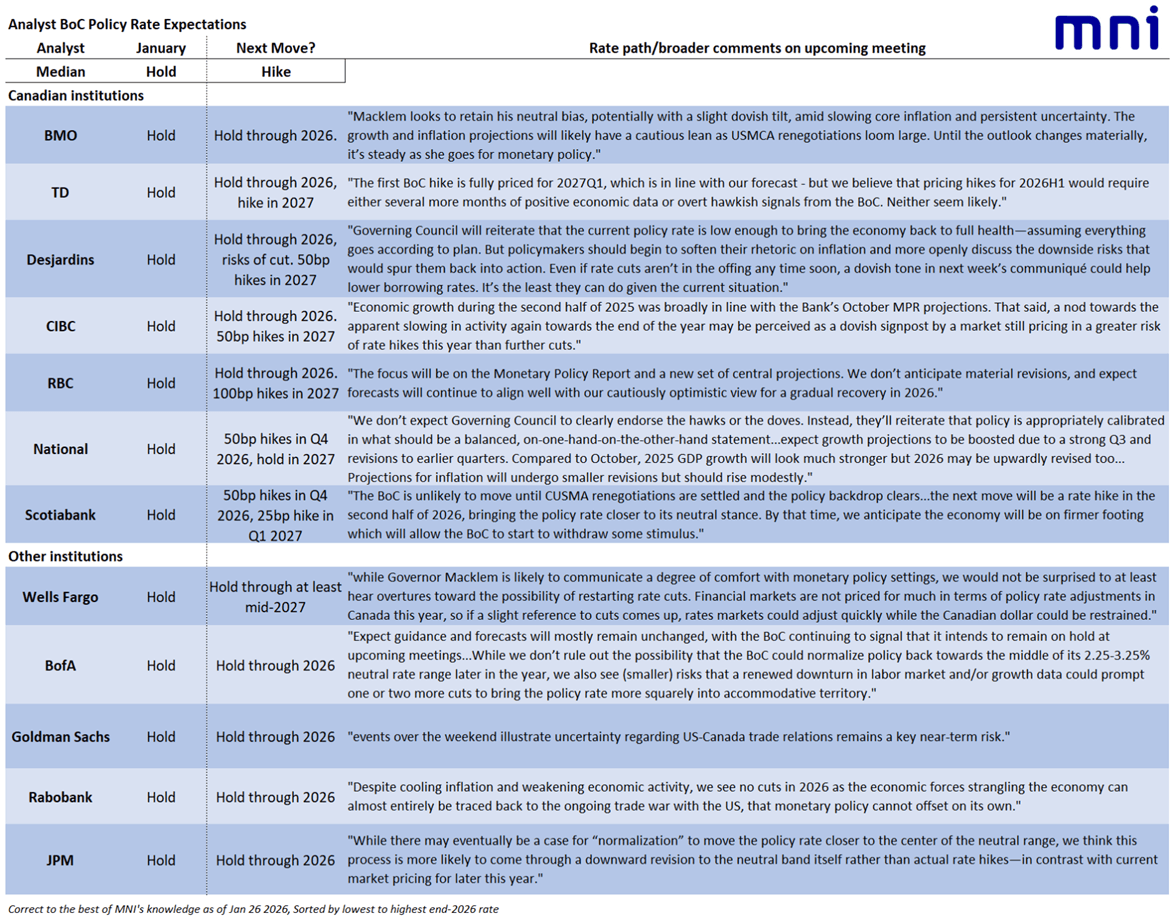

- Analysts are unanimous on a hold through at least the first half of 2026, with the vast majority seeing a hold through the full year. None see the next move being a cut as the base case. However there are a couple that have Q4 hikes as their central case and most see tightening in 2027.

- A hike before the summer would probably require a series of extraordinary upside surprises vs the soft growth and inflation expected for the coming quarters. Conversely there remain multiple potential avenues for a cut in the near-future, most prominently a renewed trade shock, potentially stemming from the upcoming US-Canada-Mexico free trade deal renegotiations due this summer. The Canadian economy was much better-insulated from the Trump administration’s tariffs than feared due to preferential free-trade tariffs for Canadian exports, and a removal of that relief could spur calls for easier monetary policy to get ahead of a deterioration in growth.

- Certainly, the BOC will probably want to wait for more clarity on this situation before initiating a hiking cycle, and such clarity is unlikely to be achieved until much later in the year. In the meantime they’ll probably want to continue conveying caution.

EURGBP TECHS: Support Remains Exposed

- RES 4: 0.8813 76.4% retracement of the Nov 14 - Jan 6 bear leg

- RES 3: 0.8797 High Dec 17

- RES 2: 0.8781 61.8% retracement of the Nov 14 - Jan 6 bear leg

- RES 1: 0.8715/46 50-day EMA / High Dec 31 & Jan 21

- PRICE: 0.8691 @ 17:55 GMT Jan 27

- SUP 1: 0.8644 Low Jan 6 and the bear trigger

- SUP 2: 0.8633 Low Sep 15

- SUP 3: 0.8620 38.2% retracement of the Dec ‘24 - Nov ‘25 bull cycle

- SUP 4: 0.8597 Low Aug 14

Last Friday’s sell-off in EURGBP signals the potential end of a corrective recovery between Jan 6 - 21. Moving average studies are in a bear-mode set-up and this continues to suggest that recent short-term have been corrective. Key support and the bear trigger lies at 0.8644, the Jan 6 low. A break of this level would confirm a resumption of the downtrend. Key short-term resistance is 0.8746, the Jan 21 high.

BOC: MNI BoC Preview-Jan 2026: Holding Is The Plan…Until It Isn’t

We've published our preview of the upcoming BOC decision - Download Full Report Here

- The Bank of Canada is overwhelmingly expected by both markets and analysts to maintain its overnight rate at 2.25% at the January meeting (announcement on Jan 28).

- This would be a 2nd consecutive pause as part of what is anticipated to be a flat rate path through 2026. The biggest question is, in which direction will the next move be?

- The account of the deliberations at the December meeting highlighted that Governing Council debated "whether it was more likely that their next move would be to raise or lower the policy interest rate."

- It remains more likely than not that the next move will be a hike, with a downside shock required for cutting again.

- The January Monetary Policy Report is likely to show an upgrade to GDP growth projections for 2025 as a whole with a potential slight upgrade to 2026 at a still-soft level. CPI forecasts also look set to be raised slightly due to higher-than-expected headline readings in the latter months of the year, but as we explain, the more important underlying metrics have been subdued.