ECB: Balanced Press Conference Helps EUR Front-end Fade Initial Reaction

ECB President Lagarde’s balanced and non-committal press conference drove a reversal in ECB implied rates. Overall, it’s notable that despite a hawkish set of projections, there is little appetite to move markets away from the current 2% terminal rate pricing.

- OIS are now back to pricing just below 3bps of hikes through the end of next year, after reaching over 5bps of hikes following the more hawkish-than-expected December macroeconomic projections.

- Lagarde stressed that policy is still in a “good place”, and that still-elevated uncertainty calls for a data-dependent and meeting-by-meeting approach.

- There was no endorsement of potential hike speculation, and an admission that “one thing that hasn’t changed is uncertainty and that’s not a comfortable position” provided a marginally dovish counter.

- Lagarde also said she wouldn’t “agonize” over neutral rate discussion, in response to Schnabel’s suggestions that increased AI investment and productivity would push up r*.

- On the risk assessment, there were no remarks around whether the growth outlook was “balanced,”, “more balanced”, or anything in between. Meanwhile, “the outlook for inflation continues to be more uncertain than usual”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (Z5) Bear Leg Extends

- RES 4: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6793.65 20-day EMA

- PRICE: 6670.75 @ 14:32 GMT Nov 18

- SUP 1: 6600.00 Round number support

- SUP 2: 6571.25 Low Oct 17

- SUP 3: 6540.25 Low Oct 10 and a key support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

S&P E-Minis maintain a softer short-term tone. The breach of support at 6655.70, the Nov 7 low cancels recent bearish signals and signals scope for an extension of the current corrective cycle. Note that price has also breached support at the 50-day EMA. An extension would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6793.65, the 20-day EMA.

GLOBAL: Reports Suggest China Diplomat Dissatisfied with Japan Meeting Outcome

- "*CHINA DIPLOMAT DISSATISFIED WITH RESULT OF JAPAN MEETING: PAPER" (BBG)

- "Chinese diplomat Liu Jinsong says he is “of course dissatisfied” with result of his meeting with Masaaki Kanai, the Japanese foreign ministry official in charge of Asia and Oceania affairs, Chinese news outlet The Paper reports."

- Earlier, the SCMP said Beijing could step up military and coastguard activities near Japan if tensions escalate further following Japanese Prime Minister Sanae Takaichi's provocative remarks on Taiwan, citing analysts.

- Indeed, Reuters wrote that Japan has warned its citizens in China to step up safety precautions and avoid crowded places, amid a deepening dispute between Asia's two largest economies over the new PM’s comments on Taiwan.

- ING have noted that the sudden escalation in Japan-China tensions has already triggered retaliatory measures from Beijing, including travel restrictions, aimed at hurting Japan’s profitable tourism business. They said that high-level diplomatic talks are already scheduled, and risks of further escalation do not seem too high.

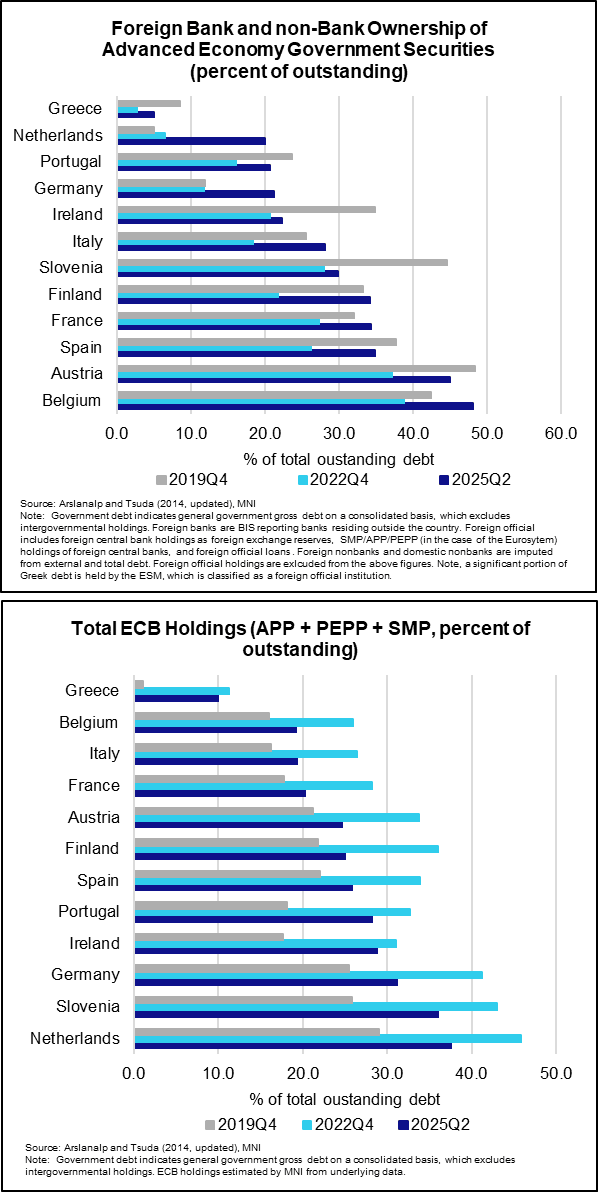

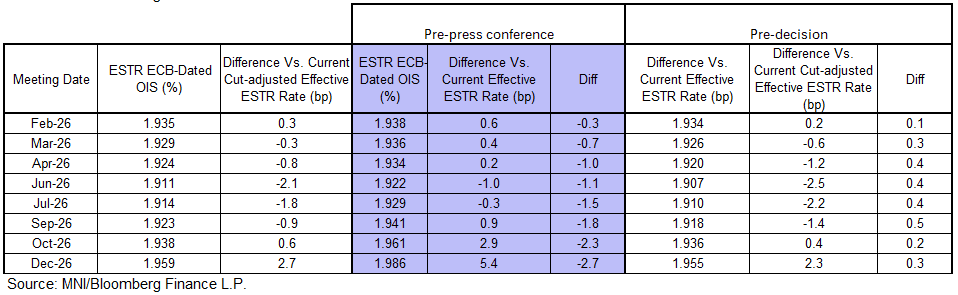

BONDS: Rise In "Foreign" EGB Exposure May Represent Intra-EZ Reallocations

In the Eurozone, the reduction in ECB exposure is largely accounted for by “foreign” agents. However, the IMF dataset does not differentiate between intra-Eurozone and extra-Eurozone agents. We suspect that a good deal of increased “foreign” exposure represents reallocations across Eurozone countries.

- Note that both the Spanish and Portugues debt agencies have highlighted increased foreign demand in recent interviews with the MNI Policy Team.

- ECB monetary policy portfolio runoff looks set to continue for the foreseeable future. In a recent speech, Executive Board member Schnabel noted that “We expect that our monetary policy bond portfolios will be run down completely, unless monetary policy considerations were to require renewed asset purchases at some point in the future.”

- Across countries as of Q2 2025, the ECB had the largest footprint in the Netherlands (37.6% of total general government debt), following by Slovenia (36.1%) and Germany (31.1%).

- Foreign bank and non-bank ownership of EGBs is most visible in Belgium (48.1% of outstanding), Austria (44.9%) and Spain (34.8%).