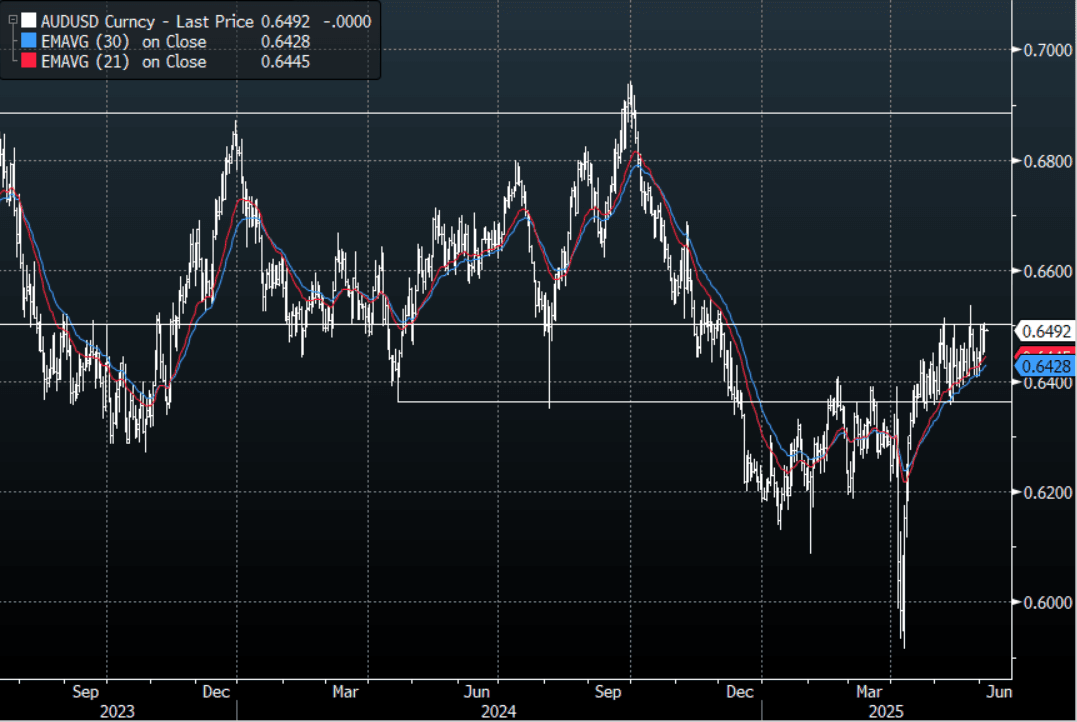

AUD: AUD/USD - Bounces Off 0.6450, Eyes Top Of Range Around 0.6550

The AUD had a range overnight of 0.6453 - 0.6505, Asia is opening around 0.6490. The AUD had a decent bounce overnight after the demand around 0.6450 proved solid. The USD could not hold onto any of its gains as US yields fell quite hard reacting to weaker data and the market pricing in more rate cuts. At the moment the USD seems to fall in most scenarios.

- (Bloomberg) -- “Australia’s weaker-than-expected 1Q GDP growth isn’t great, but it’s not a cause for alarm, writes BE’s James McIntyre. Extreme weather dented demand, giving a false impression that a baton pass from public to private demand is struggling. The economy is soft — but not as weak as the 1Q figures suggest.”

- “There’s room for further monetary support. We don’t think the RBA will necessarily regret its decision to cut the cash rate by only 25 basis points instead of 50 bps in May. It’s likely to keep easing at a gradual pace, delivering the next 25-bp cut in August.”

- The AUD moved higher overnight bouncing off the demand seen around 0.6450 as the USD came under heavy selling pressure.

- Price is back in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. Price looks set to test the top end of the range but I am not sure how far it extends until we get confirmation of a slowdown in labor from the NFP tomorrow night.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6490(AUD1.14b). Upcoming Close Strikes : 0.6300(AUD 1.47b June 6), 0.6420(AUD771m June 10)

Data/Event: Trade Balance, Household Spending

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Better Data and Supply Takes Back End Yields Higher

TYM5 reopens at 111-03, up 0-01 from closing levels in today’s Asia-Pac session.

- Overnight US 10-year yields had a range of 4.2869% - 4.3687%, closing near the highs.

- Treasury yields ended mostly higher overnight reacting to a strong ISM Services PMI, The move was led by the back-end with the 10yr up 0.05, steepening the yield curve.(2s10s +2.46 at 50.695).

- MNI US ISM SERVICES PRICE INDEX RISES TO HIGHEST SINCE JAN. 2023

- MNI US APRIL ISM SERVICES PMI RISES TO 51.6 FROM 50.8; EST. 50.2 bbg

- MNI US ISM APR SERVICES PRICES 65.1

- The data keeps coming in better, hence the market continues to price out rate cuts. The prices paid print will also be something the market watches with keen interest after a big jump.

- The 10-year Yield range seems to be 4.10% - 4.45%, price has moved back above the 4.30% pivot and with more supply to come this week a push back to 4.45% is possible before the buyers come in.

CNH: USD/CNH Near 7.2000, Onshore Markets Return Today, Caixin Sercices PMI Out

USD/CNH tracks near 7.2000 in early Tuesday dealings. The currency rose a modest 0.16% for Monday's session, as focused remained on broader Asian currencies gains, led by TWD. Broader USD sentiment was mostly weaker for Monday's session the BBDXY index down 0.31%, the DXY off 0.25%. Onshore China markets return today after the break since May 1 for the Labor day holiday period. Note spot USD/CNY ended the pre-holiday period at 7.2714.

- For USD/CNH technicals, intra-session lows from Monday came in at 7.1845, while selling interest came in above 7.2100 for the pair. The 200-day MA, which comes in around 7.2220 and acted as a support point in March may now act as a resistance point. On the downside, a clean break sub 7.2000 could see late Oct highs from last year near 7.1640 could be in focus.

- We did see some USD recovery in Monday US trade following the better than expected ISM services print. US yields finished higher, led by the back end of the curve, 10yr back above 4.34%.

- Still, in EM Asia the broader focus remains on USD weakness, as speculation continues around drivers of recent TWD gains (export repatriation, lifer hedging etc), with foreign currency deposits potentially shifting back into local currency elsewhere in the region.

- The other focus point is on US-China trade talks and what role a stronger yuan may play in any agreement that brings down tariff levels.

- The USD/CNY fix will be in focus today given the spot USD/CNH move, while on the data front we have the Caixin PMI services due. The market forecast is a 51.8 outcome, versus 51.9 prior.

USD: Goldman Sachs On USD Overvaluation

The global bank weighs in on USD valuations and how much the dollar might fall.

Goldman Sachs: "How overvalued is the Dollar? Investors have been asking how overvalued the Dollar is and how much further it can fall. We recently looked at this question through the lens of our two formal FX fair value models: GSDEER and GSFEER. These approach the question from separate angles but currently provide similar signals: the Dollar is around 16% overvalued on a trade-weighted basis. The FEER model links the currency to an economy’s external and internal imbalances, and we think it is the more relevant benchmark at the moment given the focus on the US current account deficit. Under the model’s assumptions, a 17% Dollar depreciation would be consistent with the US current account deficit (currently over 4%) converging to its long-run 'norm' (around 2.6% on our estimates), all else equal. In practice, external balance adjustments are often achieved with shifts in both domestic demand and exchange rates. Valuation is not a catalyst in and of itself and so exchange rates can trade far from their long-run fair value for extended periods, as has been the Dollar’s case over the past decade. However, when there is a rapid and large enough shock to macroeconomic fundamentals, currency adjustment back to fair value and/or large shifts in the fair value itself can be relatively fast. We have seen this before, for example with GBP during Brexit and with EUR during the gas supply shock. Finally, we would note that it is not unusual for currencies to overshoot once fair value is reached."